Anaplan (PLAN) Q3 FY21 Earnings Teardown

We break down Anaplan's Q3 FY21 update.

Anaplan Earnings Summary

Historical Financials | Press Release | Earnings Transcript | Earnings Presentation

I separate this teardown into three parts: 1) company overview; 2) earnings highlights; 3) updated thesis on PLAN and outlook

Summary: Anaplan is the leading cloud-based business-planning software which provides data for decision-making purposes. PLAN is currently doing $418 ARR growing 31% YoY and 7.7% QoQ. By leveraging the public cloud, PLAN aims to expand their leading market penetration. Their partnerships include joint GTM with systems integrators, including tremendous opportunities for partner developed solution across functions and verticals, that leverage both Anaplan and public cloud vendors. The partner ecosystem is a key part of their strategy, enabling Anaplan's business to scale, both from a services and go-to-market perspective.

I. Company Overview

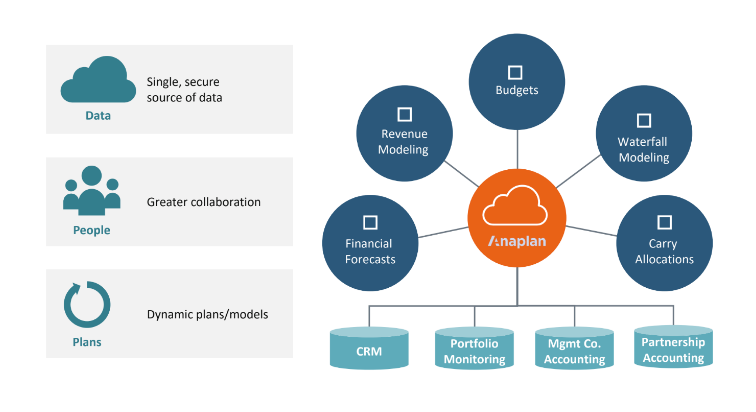

Anaplan's platform

Anaplan allows businesses to consolidate projection planning and decision-making across the whole enterprise. With the unique Hyperblock™ technology, users can model different scenarios and visualize the impact of business decisions on all departments within an organization. Anaplan is leading the future of enterprise projection and uniquely positioned given their penetration of large enterprise, extensive network and growing reputation, proprietary technology, and marketing/growth strategy that allows them to continue to dominate this space for years to come.

Why Anaplan wins:

- Versatility of landing spot within customers: many customers site starting their use of Anaplan in one of sales, finance, supply chain, etc. and then expanding use cases across their organization.

- Democratization of end-user: no technical knowledge required (familiar excel-style platform usable by everyone)

- Sophistication of use cases: supports complex financial modeling and connections to operational use cases

- Most integrations of FP&A products: offers pre-built solutions with the Anaplan App Hub

- Hyperblock technology (with in-memory calculation): ability to have thousands of users working on same model simultaneously. “The ability to update a single variable and have that change propagated through the entire model is unparalleled.”

Business model & strategy

- Subscription-based model with 3 levels (Basic, Professional, and Enterprise)

- 1,500+ customers served as of most recent quarter.

- 250+ Global 2000 companies, No customer represents 10%+ of revenue in 2019.

Go-to-Market

- Direct sales team targets large enterprises (Global 2000 companies)

- Strong network of Global and Regional Partners, targeting mid-market organizations

- Anaplan CPX annual conferences, connect existing and potential customers and reinforce brand

- Training at Anaplan Academy allows clients to efficiently migrate to Anaplan

Market Opportunity - Gartner's estimates

- The connected planning market is incredibly fragmented and undergoing heavy consolidation and digital transformation as companies move from traditional spreadsheets. It is estimated to be $21B in 2021.

- By 2024, 70% of new financial planning and analysis projects will become extended planning and analysis (xP&A) projects, extending their scope beyond the finance domain into other areas of enterprise planning and analysis.

- By 2024, 50% of new financial planning and analysis implementations, upgrades and replacements will be sourced from core financials vendors, due to superior integration and product bundling.

- By 2024, 80% of new artificial intelligence projects in the finance domain will be deployed using out-of-the-box functionality.

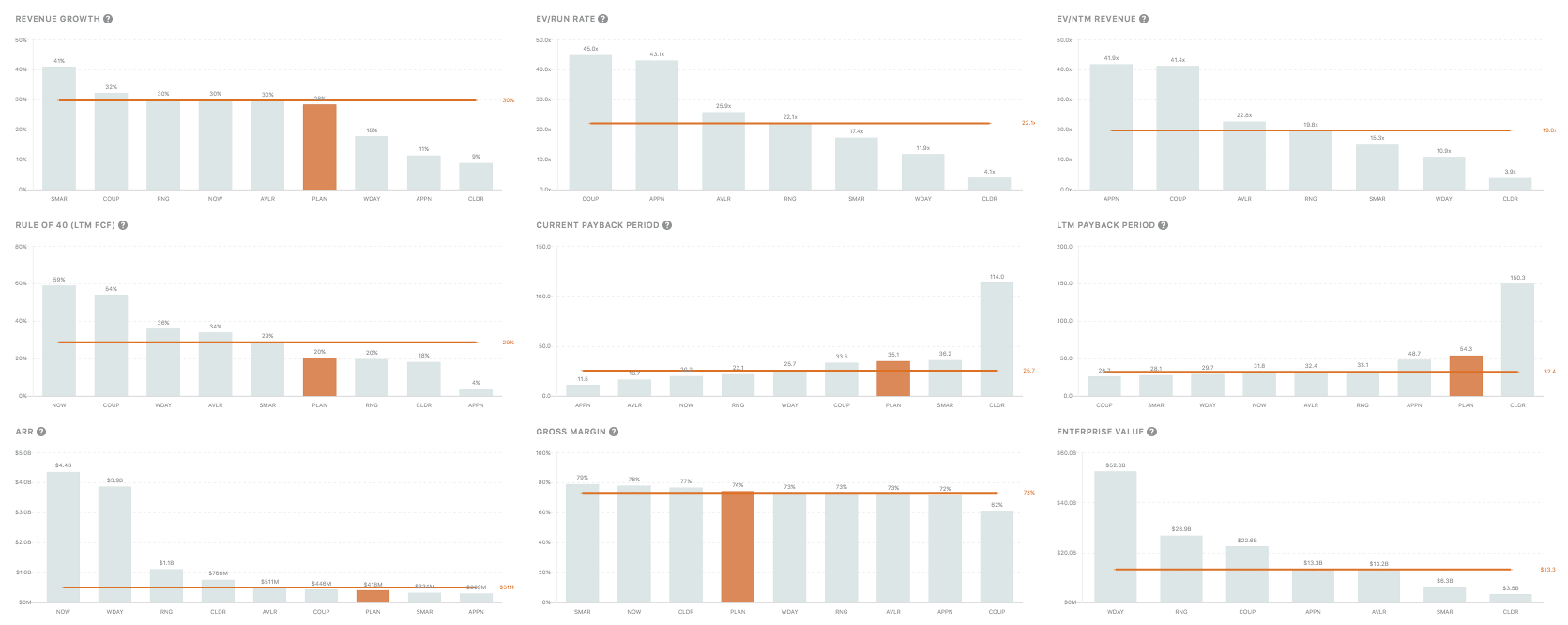

Competitive Landscape

How Anaplan stacks up vs. other large enterprise software vendors

II. Earnings Highlights & Takeaways:

Product:

- Anaplan and Google Cloud announced a new go-to-market partnership to offer the Anaplan platform on Google Cloud.

- Anaplan introduced new intelligence capabilities for predictive forecasting and scenario planning using PlanIQ with Amazon Forecast.

- Anaplan announced a multi-year deal to support Shell with digital transformation.

- Anaplan Ranked Among Fastest Growing Companies on Deloitte’s 2020 Technology Fast 500 list.

- Anaplan was recognized as a Leader in Gartner’s 2020 Magic Quadrant for Financial Planning & Analysis Solutions.

- Anaplan was recognized as the 2020 Gartner Peer Insights Customers’ Choice for Sales Performance Management.

Financials:

- Total revenue for the third quarter was $115M, +28% y/y. Subscription revenues grew +31% and comprised 91% of total revenue. Service revenues were $10 million, roughly flat from the third quarter last year.

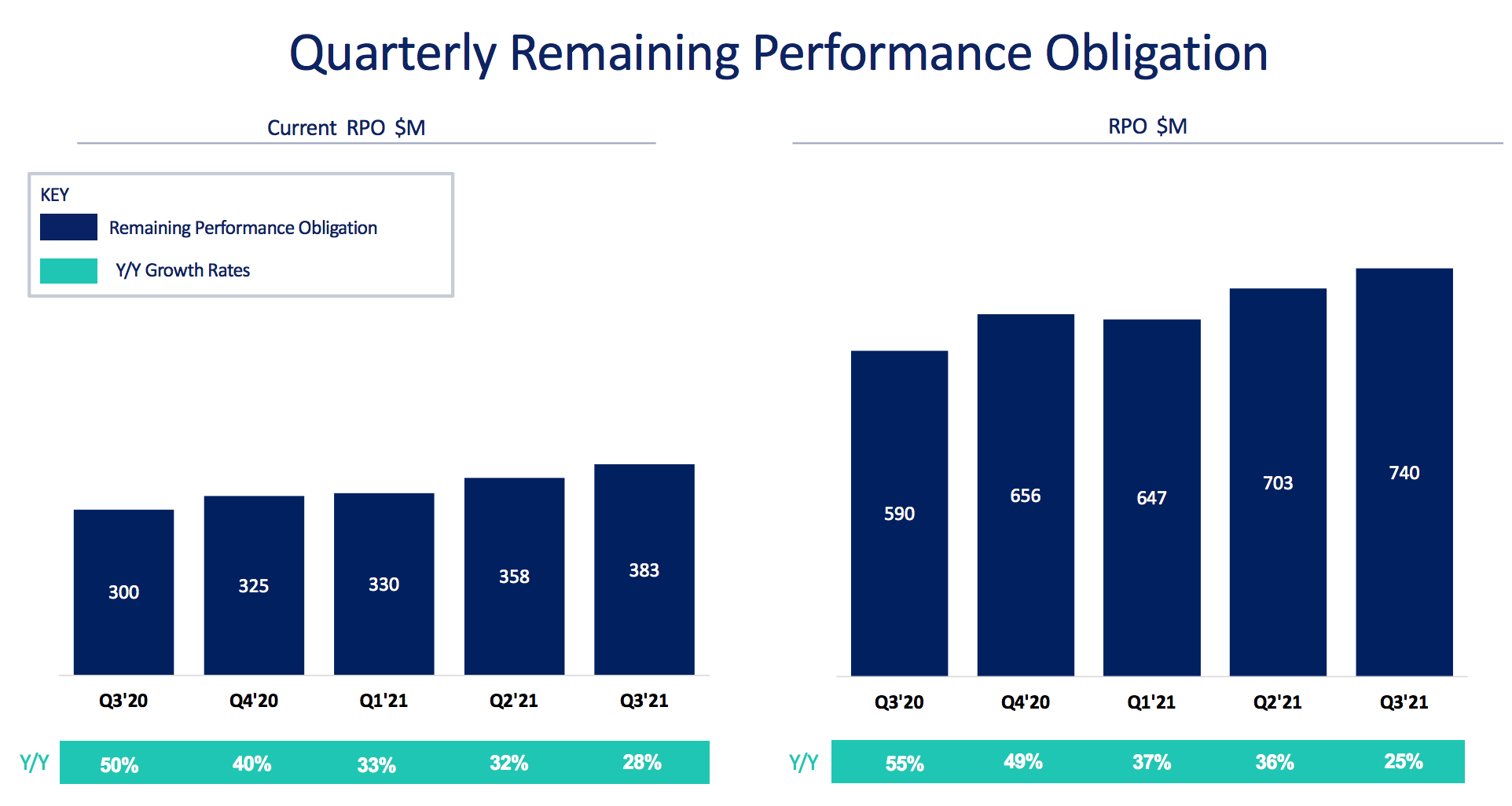

- Q3 Billings were $145 million, +27% y/y and represents a sequential improvement compared to last quarter’s y/y growth rate of 22%. RPO exiting the third quarter was $740 million, up 25% over last year. The current portion of RPO that is expected to be recognized as revenue over the next 12 months, is $383 million, up 28% year-over-year.

- We remain focused on driving higher volume in expand deals. However NRR does continue to reflect a lower volume of expand deals as compared to this time last year, primarily due to the impact of COVID-19 on the timing and velocity of deals. There was no change in churn this quarter, and our overall customer retention rate is in line with historical levels.

- Operating margins were negative 5%. An improvement of approximately 5 percentage points compared to negative 10% in the same period last year. Net loss per share in the third quarter was $0.05, based on 141 million weighted average shares. Free cash flow for the third quarter was negative $9 million.

- good working capital management, and we experienced minimal deal exception requests for extended payment terms and split billings.

Q4FY21 Guide: we anticipate revenue in the range of $118.5 million to $119.5 million. Within this, we expect services revenues to be in the range of $9.5 million to $10.5 million. In order to provide more visibility during this time of uncertainty, we’ll provide a baseline for our fourth quarter billings, which we expect to be in the range of $152 million to $153 million. This implies a year-over-year growth rate in the range of 20% to 21%.

On churn: there were no large elevated amount of churn this quarter. We continue to see churn in the single-digit. Overall customer retention rate is in line, which is very positive.

On partners: strong contribution from partners in Q3, where over two-thirds of our top 20 deals have partner influence. The Anaplan value proposition is resonating with our partners. We are at the forefront of many digital transformation discussions and partners are amplifying the Anaplan value to their customers, into other pervasive digital transformation platforms, like Salesforce, Adobe, ServiceNow, Workday and SAP. As far as the buildup of investments that partners have been making in their Anaplan consultants. We saw a continued increase in net investment this quarter again, by another couple of hundred, and we even had one customer, one partner, I should say, actually mentioned to us even within the last few weeks, that they’re pretty much at kind of a — I guess you can say a sold out capacity. Meaning that they have to do even more hiring, because the current consultants that they have are now either engaged in projects or about to be engaged in projects.

On competitive landscape: Anaplan was showcased as a leader for the fourth consecutive year in the Gartner Magic Quadrant for Cloud Financial Planning and Analysis Solutions. Anaplan has moved up from a major player to a leader in IDCs 2020 vendor assessment for cloud enterprise performance management software. IDC Highlights Anaplan as a cloud EPM vendor, that approaches this space with the idea that planning incumbency is more than just the finance function, and labeled Anaplan as one of the larger pure play EPM vendors on the market.

On the need for Anaplan in this environment: Management noted that despite the uncertainty in this current business environment, customer wins this quarter underscore the value of Anaplan’s unique ability, to solve for enterprise grade operational planning. A common theme across customer conversations was the need for significantly more insight into the performance of their business. Customers now have greater access to data, and are looking for ways to identify the dynamic levers that will impact and influence their business outcomes.

III. Updated Thesis

1. PLAN is still early on the S-curve, but on the right side of change

- Anaplan delivers immediate, quantifiable ROI to customers:

Companies can benefit as much as 537% ROI over three years by deploying the Anaplan platform--"Total Economic Impact (TEI)" study by Forrester Consulting

- Anaplan competes in a market with few established players, and aims to create a product that disrupts legacy incumbents in the ERP space: software is attractive to a diverse set of large enterprises: Enterprise customers prefer a single, consolidated platform, translating to high value and efficiency. Anaplan's product separates itself from legacy vendors by being cloud-based, offering in-memory calculation, and its focus on consolidating data across different departments in an enterprise.

Anaplan competes favorably:

- Customers choose Anaplan as the only solution that can support a range of different use cases. across territory and quota, sales forecasting, incentive comp and much more, all on a single platform, in essence, delivering a connected sales business outcome.

- Anaplan is an FP&A tool every large enterprise could use. Customers have cited that [the organization] will get to a certain size and have to have a system like Anaplan. The previous alternative was doing this in Excel, but it would be unbelievably painful to do it that way once you get to their size.

This gives them a very definable market to compete in, and I like the fact that they reference how they have more than 250 of the Global 2000.

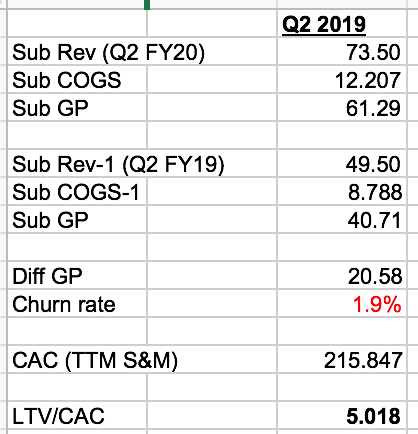

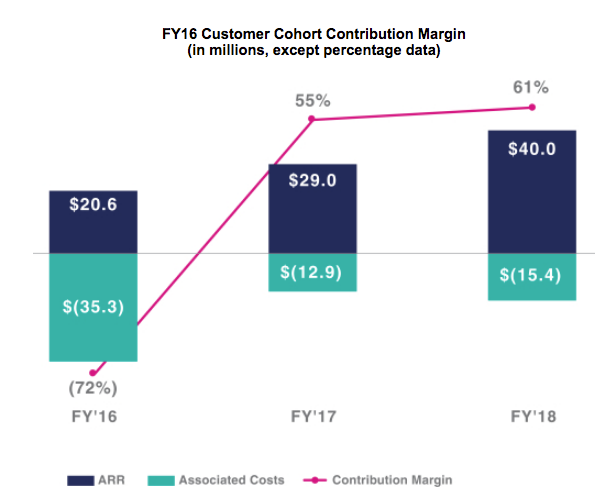

- This results in a product with very little churn (~1.9%):

One of the biggest reason's Anaplan's product is sticky is because it literally removes and automates a role that was historically done by a person within the organization by consolidating all of the planning work into a single platform.

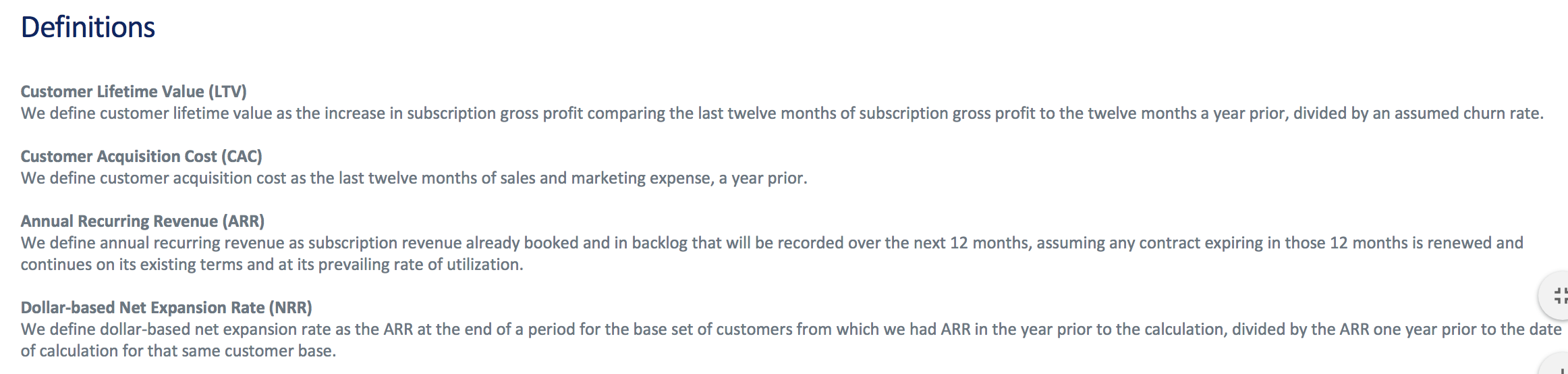

Anaplan defines the following terms in their earnings presentation deck:

In Q2FY20, we got a glimpse at what their historical churn rate is when management mentioned:

Given their definition of LTV and CAC, we can calculate an implied churn rate as follows:

As management stated in their most recent call that churn numbers are returning to historical levels, we can assume that current churn is in-line and ~2%.

2. PLAN is primed for ACV expansion which will likely result in them guiding for cRPO re-acceleration in FY22

- Current RPO (cRPO) is the best metric to measure the underlying growth of PLAN's business. cRPO is the RPO that will be recognized within 12 months. Its a better metric to look at than RPO because it adjusts for duration of contracts. While RPO benefits from multi-year subscriptions, cRPO will only count 1 year in the "current" portion. cRPO is a better metric than billings because billings has timing issues for when they invoice.

Anaplan's Q1FY22 faces a really easy comp against Q1FY21, during which they only added 5M of net new cRPO.

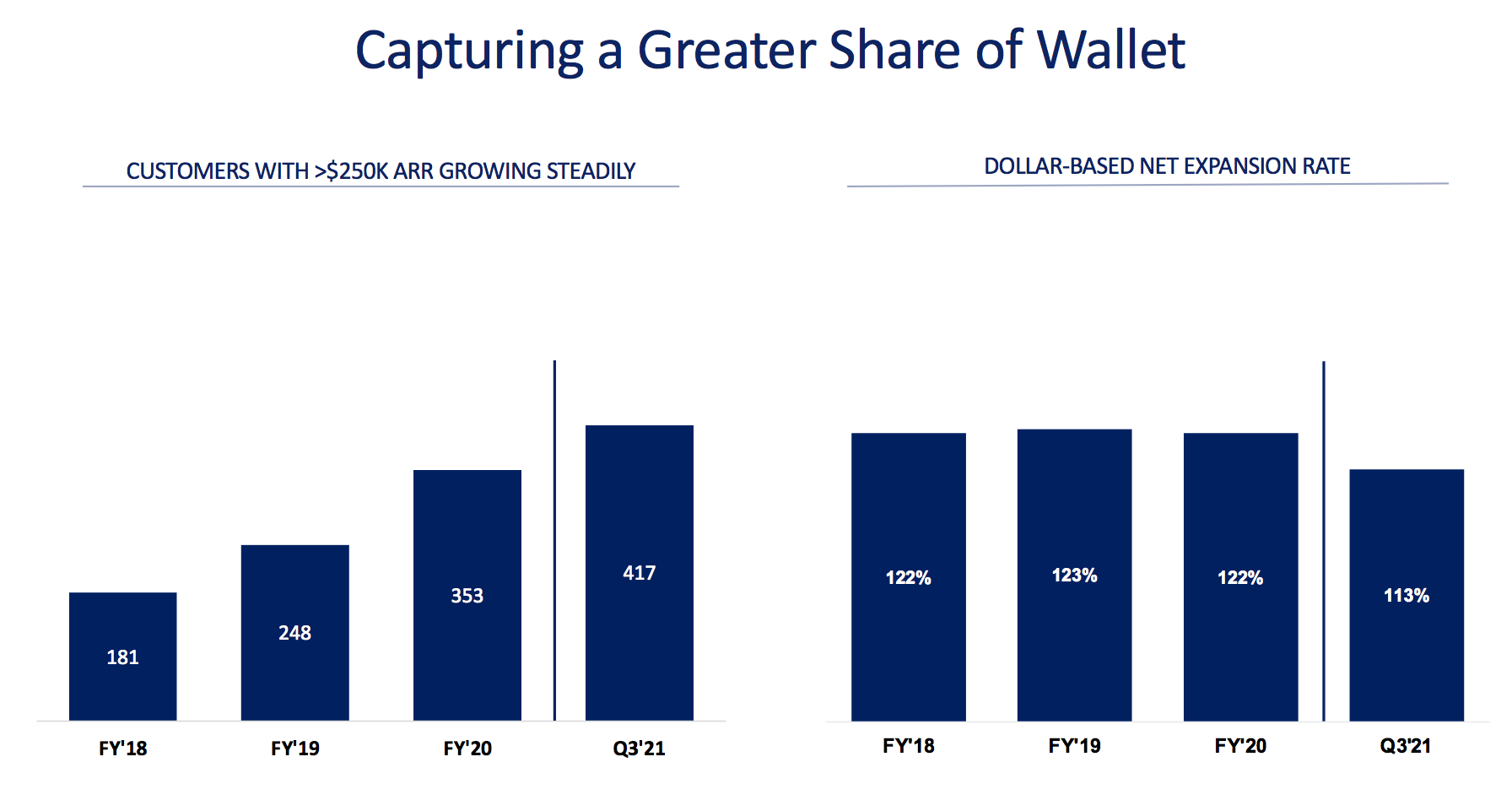

- Although churn returned to historical levels, customers still aren't landing and expanding at pre-pandemic levels yet. This is evident in DBNE falling from being in the 120s for the past 12 quarters to 117% in Q1, 116% in Q2, and now 113% in Q3.

- However, as we've seen that customers aren't churning, I believe the guide for FY22 will be optimistic as Anaplan will see pent-up demand for their product from customers who haven't expanded during FY21, as COVID-19 highlighted a number of scenario planning use cases.

- Management noted that the largest customers expanded contracts, but this wasn't the case for most. "If I look at the top 10 deals and the average size of those deals, we saw an increase this quarter, which was positive. And the top 10 and also the top 25 customer ARRs, also increased this quarter. So we’ve seen kind of an increase from that perspective." - Frank Calderoni, Q3 FY21 earnings call.

- Management noted that they’re getting back to their historical mix of 60-40 (60% existing growth, 40% new growth).

- Q1FY22 faces a very easy comp: net new billings and RPO in Q1FY21 was -$30M and -$9M, respectively.

3. FP&A market is Anaplan's opportunity to lose, and this gives investors high confidence that they will achieve attractive long-term margins that are currently under-appreciated.

- Anaplan competes favorably in every category/metric relevant to FP&A: Anaplan wins on product, breadth of integrations, and customer satisfaction. Its a product that delivers very high ROI and could be argued that its under-monetized because they will have significant leverage once customers consolidate their planning needs.

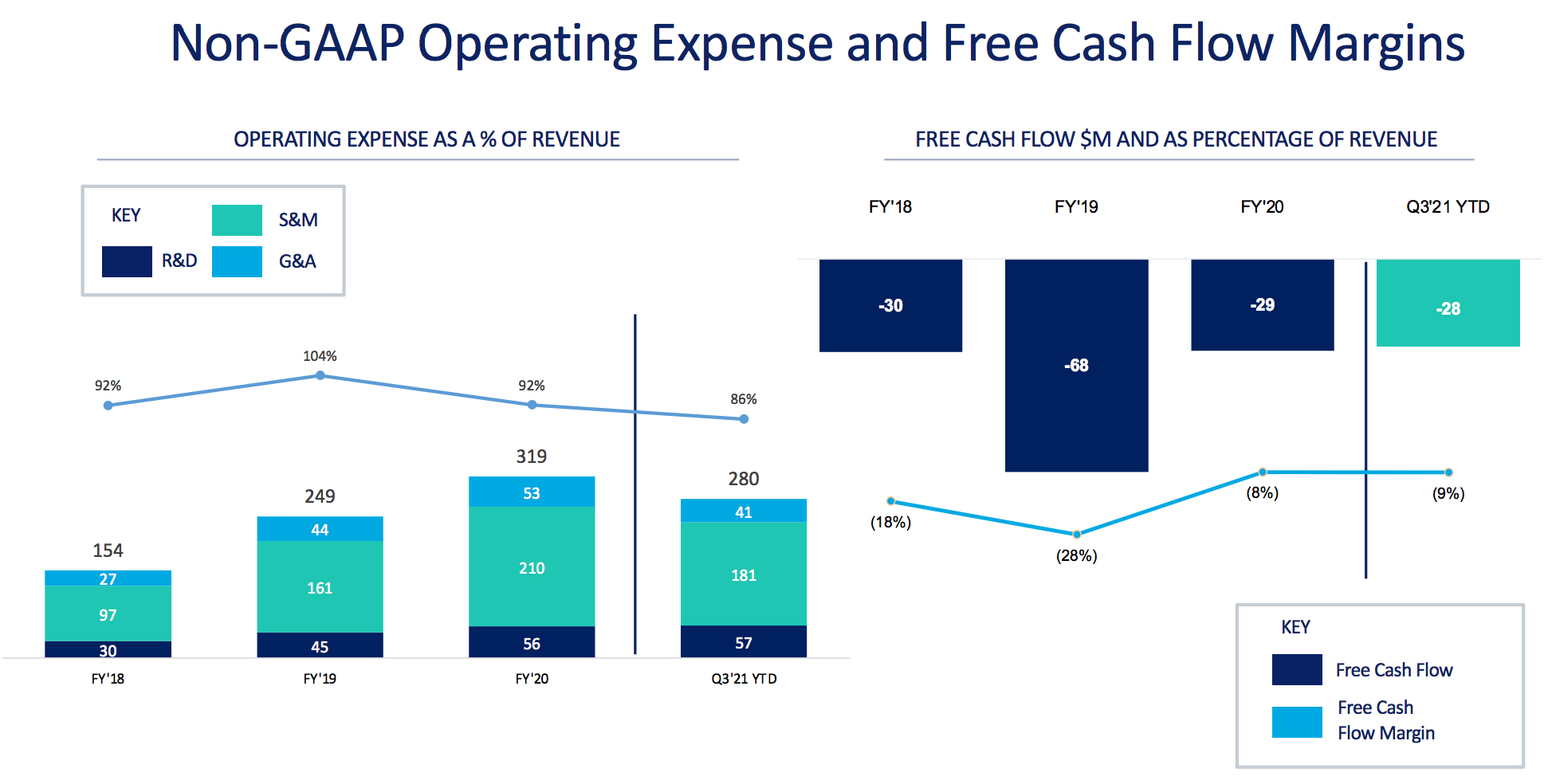

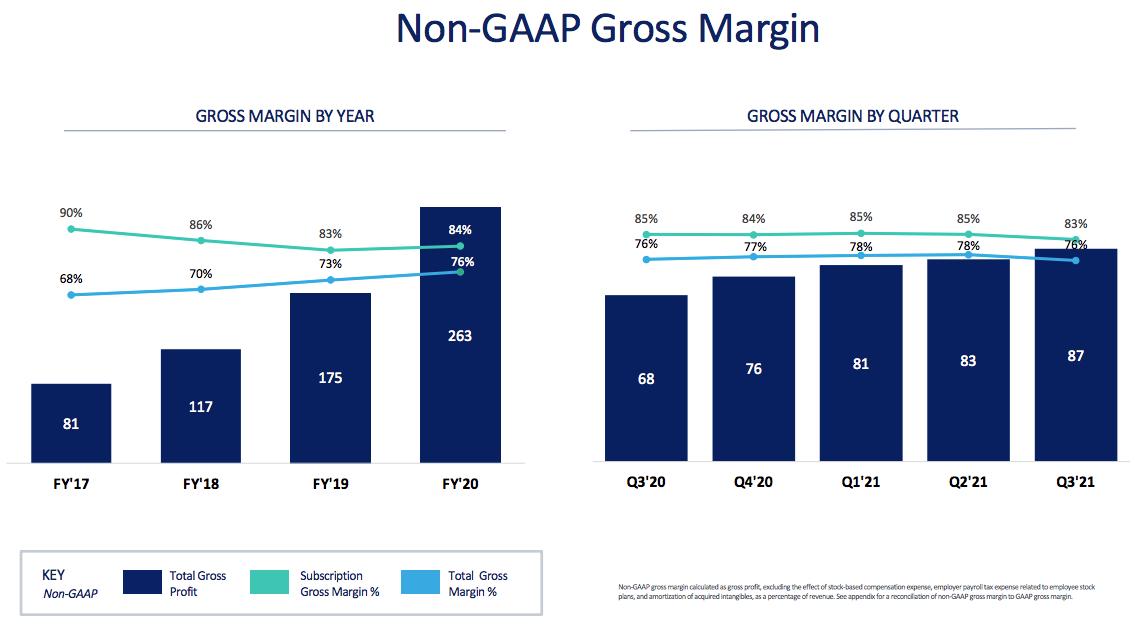

- Gross margins expand as service revenues (which operate at single digit GMs) represent a smaller proportion of total revenues. Contribution margins will likely continue to expand and are not reflected in present financials:

- S&M is a massive expense (64% of revs) at the present, but likely to converge to attractive levels as Anaplan's partner program continues to do the heavy lifting. On a positive note, LTM payback period improved slightly from 58 to 54 months (still high, even for selling $100k+ contracts to large enterprises) from the most recent quarter.

- Despite only growing cRPO at 28% y/y, bulls love the story, product, and competitive positioning, whereas bears point to the lack of improving margins and slowed growth. Anaplan recognizes the need to consolidate and digitize the massive FP&A market, but their dominant positioning gives me a lot of confidence they can win this market and continue to CAGR at ~30% for many years.

Risks:

- Execution issues - hiring and firing of Mark Anderson (now CEO of Alteryx) was equally disruptive.

- Management quality - employees have cited several management mishaps over the past couple quarters resulting in deals being pushed out of the quarter, and a general lack of sales execution. CEO Calderoni has been noted for being a micro-manager.

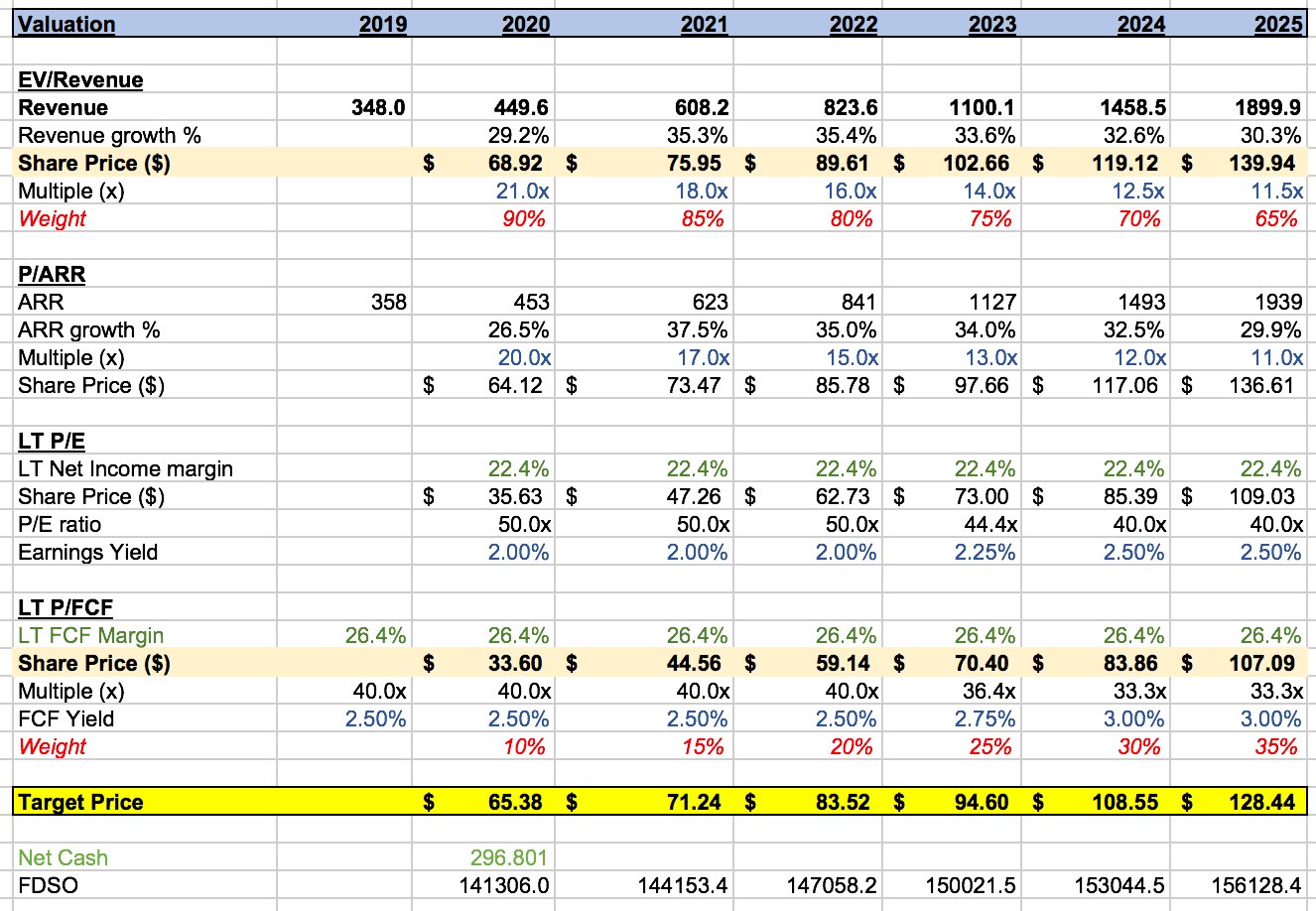

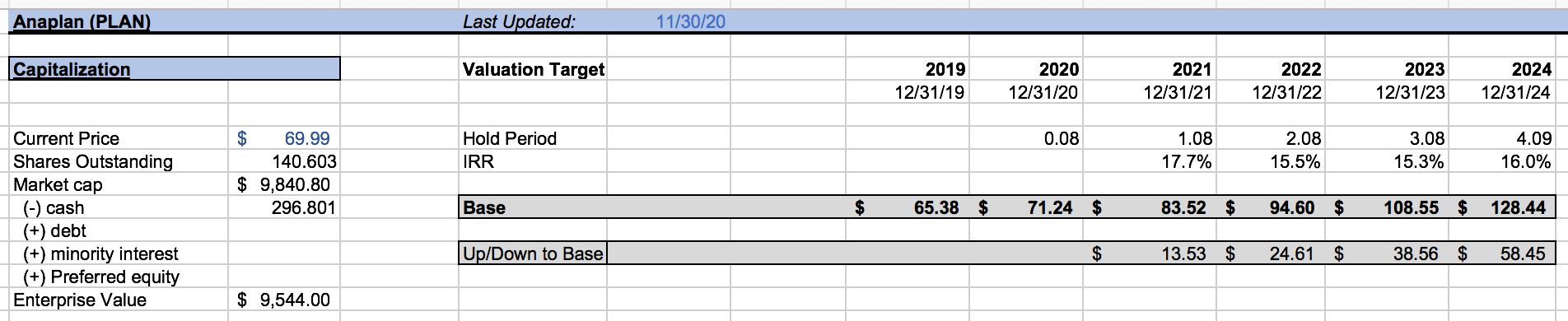

Valuation

Conservatively, I estimate long term gross margin to be 85% (current subscription margin is ~82-84%). In the long term, one-time service revenues represent a significantly lower chunk of total revenue and subscription margins converge to slightly higher levels as the bulk of customers expand their ACVs.

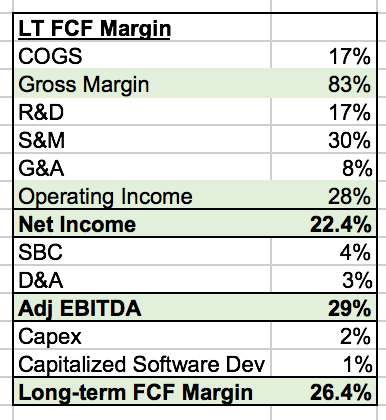

Estimate of long-term FCF margins:

Summary

Anaplan faces little competition in a rapidly growing marketspace, and it's all-encompassing suite, user-friendly interface, and high customer satisfaction will allow it to dominate this space. Because of their little competition, I believe they have a strong likelihood of achieving SaaS-like long-term margins of ~30% FCF margins. They have a great competitive positioning and a strong product that is being held back by the execution of the management team. At currently levels, I believe Anaplan is slightly overvalued and don't find the expected IRR compelling. Current RPO is the best metric of the growth of Anaplan's business and at 28% in Q3, I would expect a lower valuation multiple than what it currently trades at. The potential for Anaplan is enormous, as it could likely represent a mission-critical service for all large enterprises and delivers immediate ROI, especially in this environment. With the right execution, growth could likely inflect to much higher levels – for this reason, I still believe Anaplan to be an interesting company to watch, but remains a tier 2 SaaS company.