Elastic Q1 FY2021 Analysis

Elastic Q1 Fy2021 Earnings Analysis from a developer's perspective

Summary

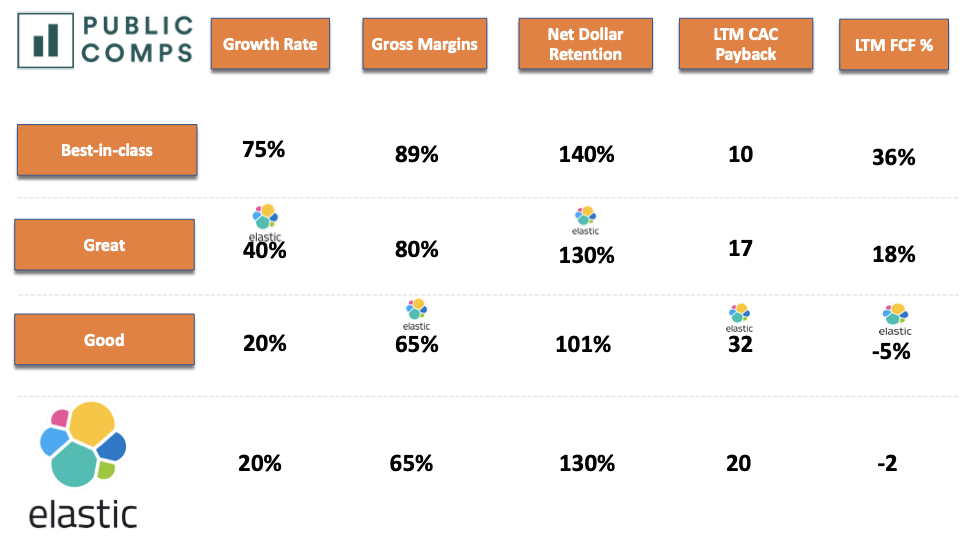

- Revenue grew 44% to 128.9 million while SaaS revenue grew 86%

- Net Dollar Retention is consistently strong at > 130%

- Gross Margins improved to 73%

- Despite margin improvement, CAC Payback periods are being driven up

Elastic is one of the most recognizable names in the software. I have been following this company for years both as an engineer & software infrastructure investor. I wanted to quickly cover what the business is, its Q1 Earnings compared to other top businesses, and how it will trend in the future.

Product

Elastic's core software is ElasticSearch. ElasticSearch is an open source search and analytics engine for data. Elastic also develops auxiliary software that integrates with ElasticSearch: Logstash & Kibana. Logstash ingests & transforms data before it is indexed in ElasticSearch. Kibana allows users to build dashboards & visualize the data. Together they are known as the ELK stack.

The use cases for this software spans across many mission critical parts of a business:

- Enterprise search: Build an enterprise engine for internal documents, customer support, and product search.

- Observability/APM: Detect which servers & applications are slow or failing, and why.

- Security: Detect security threats using the ELK stack as a SIEM while providing an endpoint security solution as well.

These use cases allow Elastic to pull from various IT budgets within an organization.

The Open Source Model

A core part of the Elastic product suite is that it's open source (recently "open core"), meaning that anyone can see the source code for free. While they give out part of their IP for free, it is an integral part of how they grow.

Open source software allows engineers that are not employed by Elastic to contribute back to the software, and create auxiliary products that develop an ecosystem around it. It effectively gives Elastic free labor & a powerful distribution engine for their product.

Elastic has two main sources of revenue: Self-Hosted & SaaS. The self-hosted part of the business allows customers to pay a subscription to host ELK on their own infrastructure. Elastic can host their stack on the cloud for their customers for their SaaS offering & charges them based on the infrastructure size. This means as their customers grow in terms of data, so does Elastic's revenue.

Customers & Competition

Customers include Fortune 500s (Facebook, Salesforce) & high-growth software companies (Shopify, Twilio) across the various use-cases. Companies use the ELK stack for one part of the business often use it for others. This is leads to a strong land-and-expand engine within these large organizations. Combined with trend of increasing data logged by these companies, and increased spend on cybersecurity, the customers will contribute more revenue year over year.

The horizontal utility & open source nature of Elastic invites a large number of competitors across its use cases. While their open source model provides great distribution, it allows AWS to cannibalize their market. AWS is the hosting infrastructure themselves so they can charge a cheaper rate. More specialized software companies for all verticals are growing quickly, both in the private & public markets.

Q1 2021 Earnings

Highlights

- Grew 44% revenue year over year at 128.9M

- SaaS grew 86%, subscription (Self-hosted + SaaS) grew 52%

- 130%+ Net Dollar Retention

- Free Cash Flow of 21.6m (17%), LTM Free Cash Flow of -2%

- LTM GM adjusted payback of 20 months

Revenue

Revenue continues to grow quickly at 43%. It was growing at 53% in the previous quarter, so there are some signs of deceleration. Their revenue run rate is at 515M, while their subscription run rate is at 485M, putting them in the middle of the pack in terms of scale versus High-Growth SaaS.

The important breakouts of their top line revenue are subscription & SaaS, which grew at 52% and 86% respectively. As the business evolves, more of the revenue makeup will trend towards subscription/SaaS, which is inherently higher quality revenue (stickier). While top-line revenue growth is strong, and when looking at SaaS/subscription it looks evens stronger.

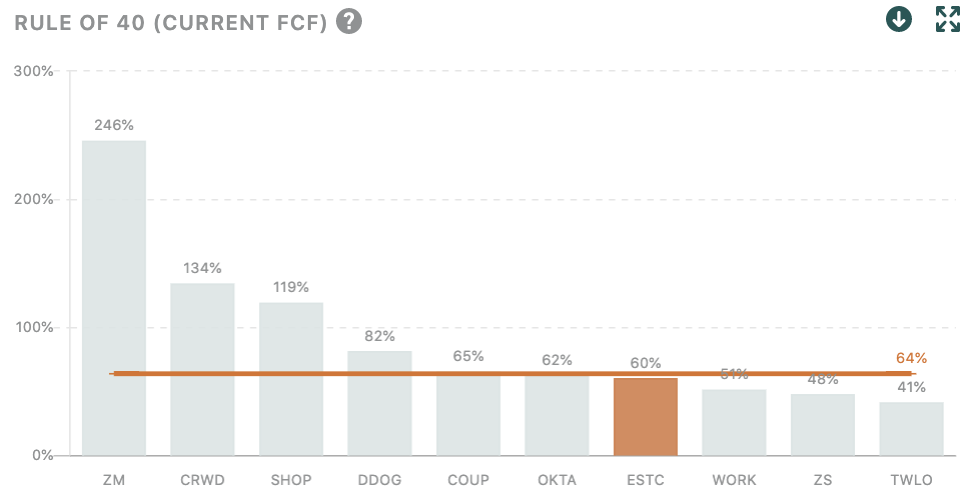

Efficiency

The company grew efficiently this quarter. FCF % + Revenue growth is 60%, passing the Rule of 40.

Net Dollar Retention

Their NDR remains high at > 130% driven by the nature of their pricing & and horizontal use cases for their product. Their revenue grows along with their customers, and having many growth customers can really drive their revenue expansion. Their ability to land with an observability product, then possibly expand that to a SIEM + Endpoint security can keep their net dollar retention high for years to come.

Gross Margins

Gross margins have been increasing as well, trending upward for the last few quarters.

Sales Efficiency & Payback Period

While their LTM payback period is solid, I expect this number to trend higher/worse in the years to come. Even though the margins are improving, customer/revenue acquisition is becoming more expensive. The reason is the swath of specialized competitors mentioned before. Elastic will have to increase their sales and marketing spend while spreading their efforts across multiple verticals to continue acquiring these customers.

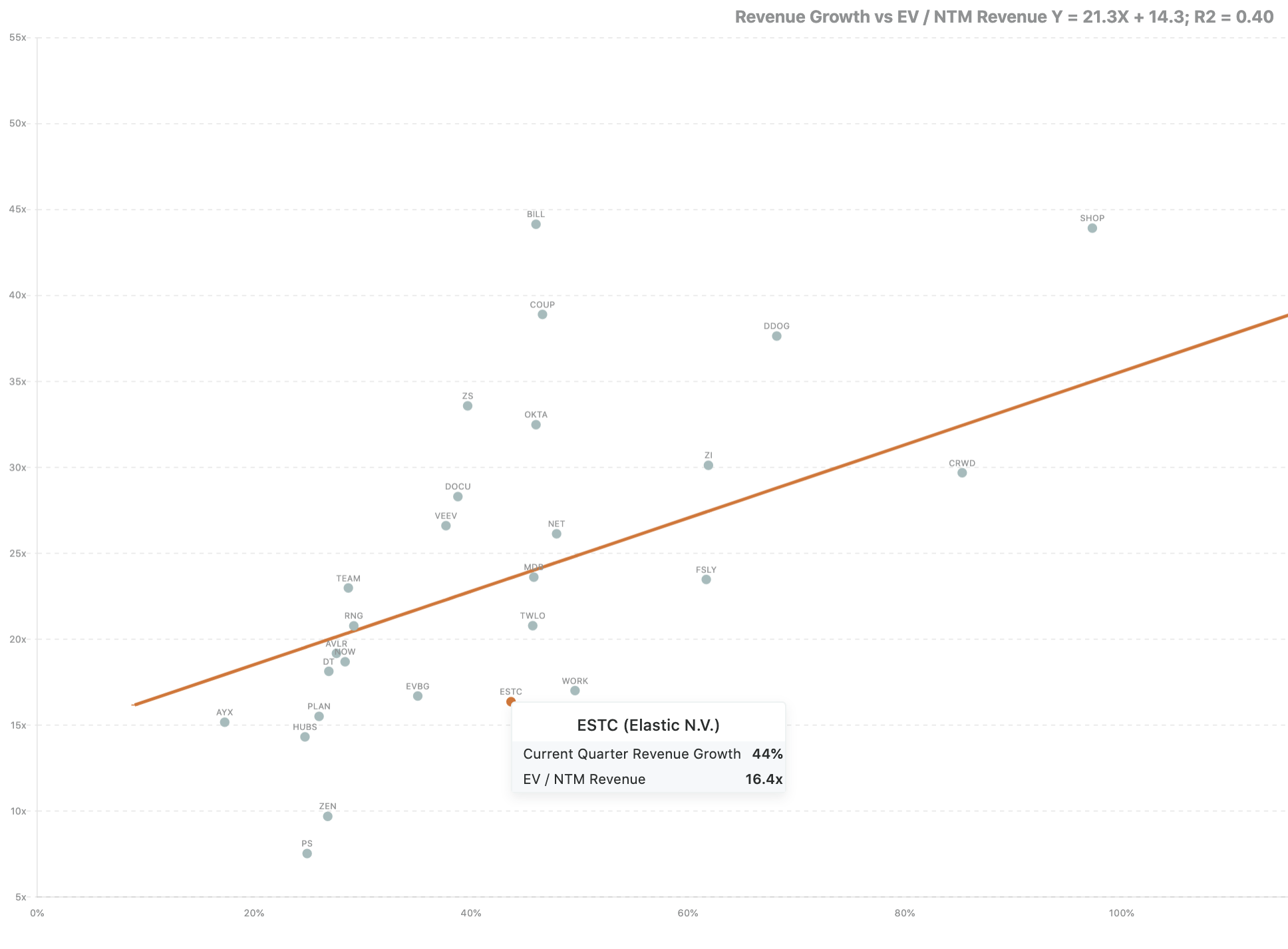

Valuation

Elastic is only trading at 16.4x EV / NTM revenue, which is cheap relative to other companies with a similar growth rate.

Predictions

CAC Paybacks Trending Upward

Competition from specialized competitors for each vertical will drive up payback periods as Elastic will have to pay more to acquire the same amount of revenue as in the past. This is especially important when thinking about valuation, as payback is one of the highest correlating features to revenue multiples.

More SaaS Revenue & consistent Net Dollar Retention

As organizations become more comfortable moving from on-premise to the cloud, the SaaS portion of the revenue will grow significantly faster than the other revenue streams.

Net Dollar Retention looks to remain strong for the foreseeable future as well, and will be a key driver to overall revenue growth for years to come. Their land-and-expand model works well with their horizontal set of products, and the SaaS offering revenues grow with their customers.

Changes to it's Open Source License

A threat to Elastic's market is AWS hosting their products at a discount. If Elastic were to change its licensing to prevent AWS from eating its revenue, it would allow them to capture more revenue from ELK stack users. They have made small steps from changing some of their software to "open core", but can get more aggressive like Mongo in the future.

Maybe the reason they aren't keen on stopping AWS is the evolution of the cloud computing landscape. Microsoft Azure & Google Cloud are growing quickly, and companies on the competitive cloud platforms might not want to add AWS to their stack. Instead they would spin up Elastic's cloud offering.

Big developments in their Cybersecurity suite

I expect that the vertical/product segment that will grow the most in the near future is their cybersecurity suite. One of the biggest COVID/WFH effects is an increase in cybersecurity spend to protect company networks from attacks originating from home networks.

Elastic developed more security products to address this increased spend, and will probably add more features in the coming months to up sell & capture this new budget.

Conclusion

Elastic is growing quickly, especially with their SaaS offering. They are equipped to capture some of the trends in APM, Observability, and Cybersecurity while being one of the biggest names in product search. My biggest concern is decreasing sales efficiency for driven by specialized competitors. All in all, Elastic is a solid business that will continue grow in the verticals it operates in.

Howard Chen, Public Comps Team

howard@publiccomps.com

Like this analysis? Subscribe to the newsletter here where we send out investment memos, market maps and analysis on the broader SaaS market.

Disclaimer: The author owns stock directly in AYX, CRWD, TEAM, TWLO, AMZN, FB, DDOG, ESTC, and ZM. Public Comps (SaaSy Metrics LLC) provides financial and industry information and analysis regarding public software companies as part of our weekly dashboard, our blog, and emails. Such information is for general informational purposes only and should not be construed as investment advice or other professional advice.