Investment Memo and Predictions for Twilio in 2020

Investment memo and predictions for Twilio in 2020

TL;DR

- Twilio is changing the way enterprises communicate with customers, in a space with small competitors that are losing market share.

- Given its strong developer focus, and easy-to-use APIs, customers willingly pay a premium for Twilio’s all-encompassing suite of communications products.

- Growth concerns are overblown (30-31% revenue growth) as the 2020 election will spark Twilio’s awareness and potential in unprecedented one-time revenues.

- Comps should be done biannually given the impact of one-time election revenue occurrences.

- TAM is growing incredibly fast (30+%) and largely unpenetrated. Twilio will be able to penetrate TAM better than any other company given its strong brand recognition.

- Very solid fundamentals, long-term driven, great moat that is increasing.

- My predictions are: 1) Twilio will make an acquisition of a fast-growing startup in a segment of the cloud communications space where they currently do not operate; 2) The 2020 Presidential election will prove to be a major catalyst for one-time revenues of Twilio’s service, causing management to increase guidance; 3) Twilio will expand into the RCS (Rich Communications Service) space.

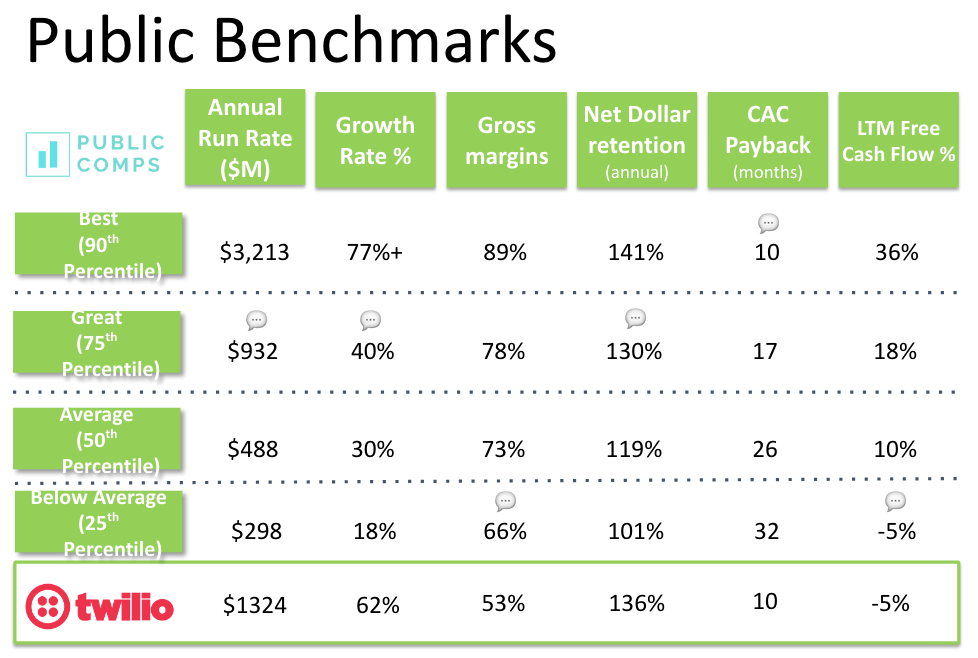

- Here’s how Twilio benchmarks on revenue, revenue growth, fcf %, NDR, payback period, etc.

Overview:

Twilio is the leading cloud communications platform that enables developers to embed channels of communication such as voice, text, chat, video and email into their applications. By providing easy to use communication APIs, Twilio enables businesses to more effectively engage with their customers. Twilio is the platform that powers the messages sent between you and your Airbnb host, the phone call between your ride-share driver, the emails you receive from Spotify, and the alerts from DoorDash.

Key Metrics

- 🔥Q4 Dollar-Based Net Expansion Rate of 124%, full year 2019: 136%.

- 🔥Q4 Revenue growth 62% (organic growth of 36%).

- 🔥Full year 2019 revenue up 75% over last year and 47% on an organic basis.

- 🔥179,000 customers (up from 64,286 a year ago, mostly due to SendGrid acquisition).

- 🔥Highest Revenue Run Rate per Employee ($500K) among top 10 public SaaS companies.

Business Model

- 👀Usage-based fees pricing model: Revenue grows as customers increase their usage of a product, extend their usage of a product to new applications or adopt a new product.

- 👀Sales model also includes free trials, volume discounts, and committed service discounts.

- 👀Flex (Cloud-based contact center), SendGrid (Email Marketing), Twilio for Salesforce (automated SMS) monthly fees; other services usage-based.

- 👀179,000 Active Customer Accounts as of Q4 2019.

Selling and Marketing

Goal: “drive awareness and adoption of our platform, accelerate customer acquisition and generate revenue from customers”.

- Twilio uses a go-to-market model, primarily focused on serving the needs of developers and cultivating a large global developer community through events and conferences such as SIGNAL.

- Offers low-friction trial experience for developers after introduction to the platform, hooks with easy-to-configure APIs, extensive self-service documentation and customer support team.

- As customers' use of products grows larger, some enter into negotiated contracts with terms that dictate pricing, and typically include some level of minimum revenue commitments.

- Once customers reach a certain spending level, Twilio supports them with account managers or customer success advocates to ensure their satisfaction and expand their usage of products.

- To increase enterprise awareness, Twilio Engage roadshow discusses expansion and Twilio Enterprise Plan advertises the competitive differentiation benefits of using Twilio.

- Provides referrals to tech and consulting partners if a company lacks available developers.

Business Performance & Financials

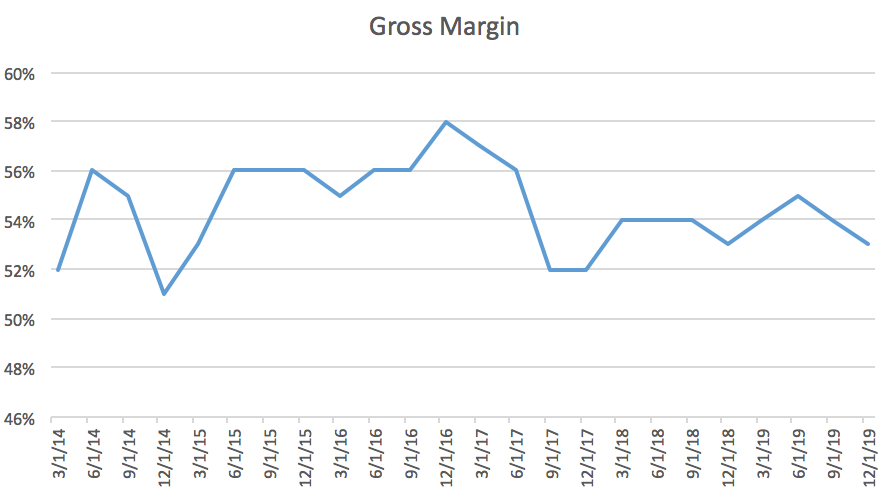

- Gross Margin Expansion

Among high growth SaaS, Twilio is heavily criticized for its low gross margins, a result of having to pay telecom fees on automated text/calls. As Twilio offers more products/services such as SendGrid and Flex with software-like margins, its total gross margins will expand as they become less dependent on SMS/call.

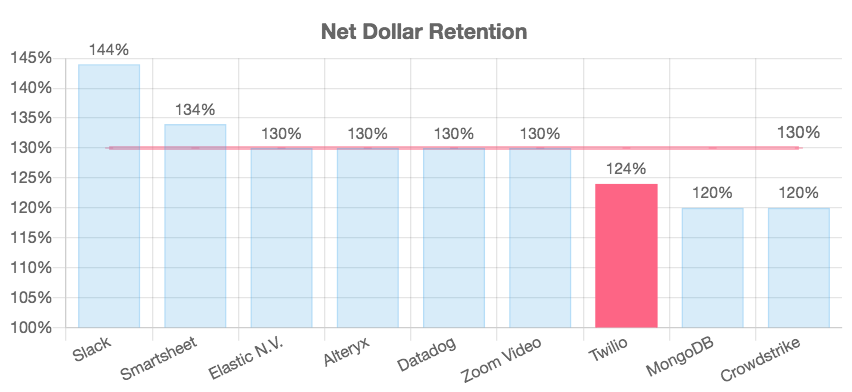

2. Net Dollar Retention

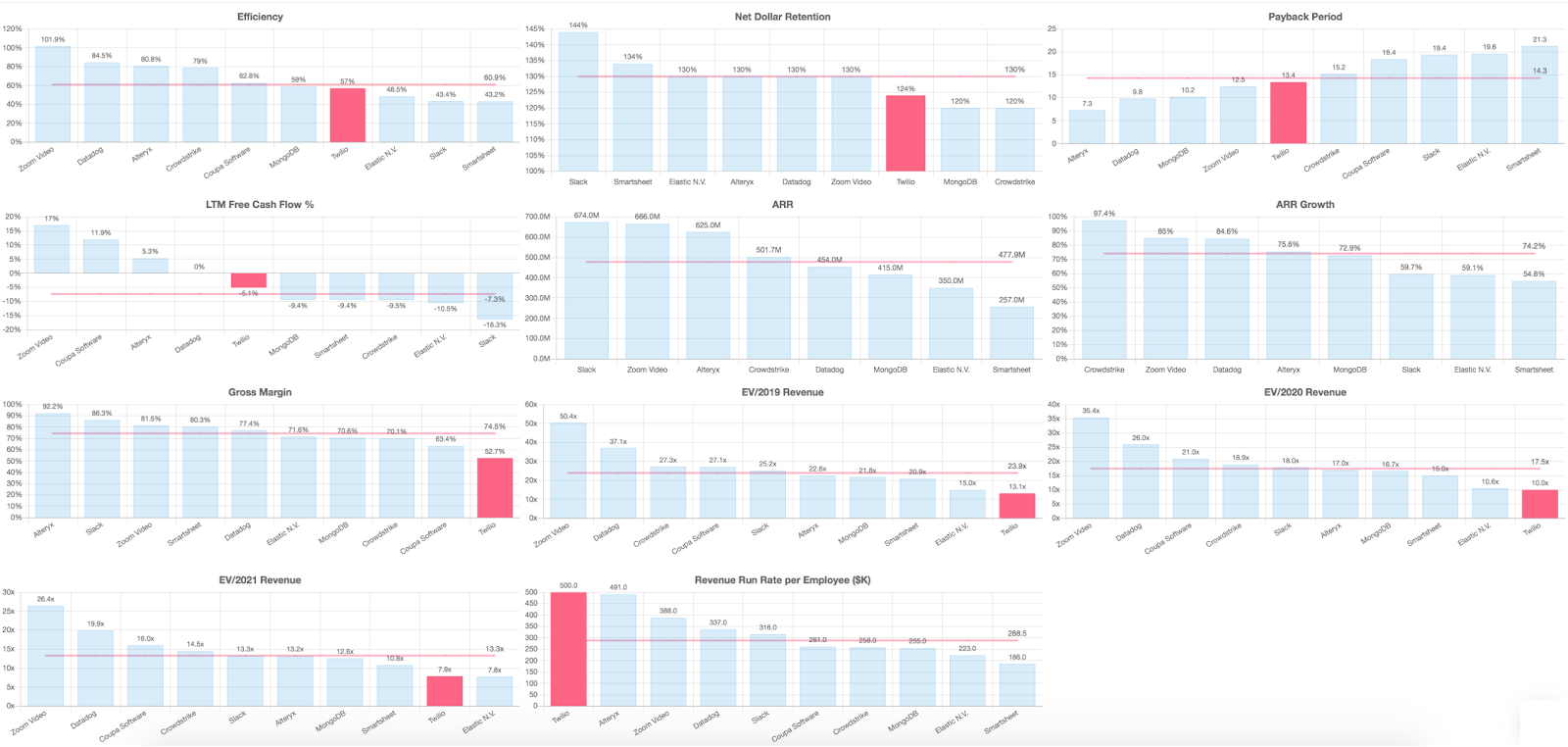

Twilio’s 136% net dollar retention in 2019 (124% in Q4) is still among the top tier public SaaS. Since they charge on a usage or per-use-basis, this demonstrates businesses’ increasing reliance on Twilio’s software to connect to their customers. Additionally, because Twilio continues to release new products such as Twilio Flex, allowing Twilio to upsell existing customers with new offerings.

That’s highlighted by 40% of their customers paying for more than one product (as of 2019) up from 10% a year prior.

Twilio (Q4 2019 NDR) vs. Top 10 SaaS on Net Dollar Retention Rate.

Other Interesting Business Metrics

- Twilio’s average revenue per user (ARPU) is currently over $6,000 (179,000 Active Customer Accounts, projected revenue $1.116B FY19) but is looking to bring in more enterprises to the business which it estimates will be moving from the 6-figure range to the 7 and 8-figure range.

- Revenue in election year 2020 will likely resemble 2018, in the way that 2019 resembles 2017 -- due to one-time increased political campaign traffic.

- Democratic National Committee handles high call and donation volumes during elections.

- Using Twilio resulted in a 10x cost decrease to the DNC.

Market Opportunity

- The biggest area of improvement in Twilio’s business are its below-average gross margins. Twilio’s SMS service offers the lowest margins because of telecom fees. Higher gross margins of Twilio Flex and SendGrid will increase free cash flow, resulting in higher multiple.

Application services: all the new components with 80-plus percent margins (such as Flex and Conversations) are growing the fastest, which will push gross margins up.

Integration of SendGrid will contribute to continued expansion of gross margins.

Twilio expects long-term gross margins of 65% (currently 55%) as it gains leverage with telecom providers and provides higher margin products like the Engagement Cloud.

2. Strong reputability and de facto leader in cloud communications; defensible moat (“a moat around the castle, and a knight in the castle who is trying to widen the moat around the castle” - Buffett)

Twilio is considered the industry leader in cloud communications, and its all-encompassing product services that span SMS, email, call, video, Flex, etc. will win in this space because customers will continue to want to communicate with their customers through various/all mediums.

3. International Revenue growth is extremely strong, growing at 100+% YoY and will likely continue to outperform as Twilio will likely reap the benefits of aggressive S&M expenditure

4. Twilio Flex allows Twilio to expand into new Unified Communications as a Service (UCaas) market w/ relatively unique position; Twilio Flex expected to be multi-hundred million dollar business in the next several years; largely replacing legacy and on-prem contact centers

“Customer engagement”: customizable interactions with consumers, is an increasing macro trend.

Flex taking longer to catch on due to enterprise cycles (12 months instead of tech’s six-month cycle), but the results should be seen towards the back end of 2020, into 2021.

Enterprise customers are adapting Flex.

5. Large TAM, that is largely unpenetrated, in core business as well as new sectors provides for resilient growth

$34B TAM today, only ~3% penetrated.

Core business is still pretty underpenetrated, ~10% of Global 2000 in voice/messaging.

Growth potential: more Global 2000 representation, Flex, new space in marketing.

Cloud Communications is still a relatively young idea.

Twilio’s position at the center of integrating communications tools into consumer-facing apps will drive 50% organic sales growth in 2019.

The move to cloud and enterprises adopting digital communications technology is still in the early stages: over the last few years we’ve seen restaurants interact with customers to alert them that their table is ready, hotels interacting with customers to ask about their stay, etc.

The best communication SaaS companies use Twilio: Attentive, which just raised $70m from Sequoia now works with over 750 leading businesses such as Coach, Urban Outfitters, CB2, PacSun, Lulus, Party City, and Jack in the Box—growing its client list 347% in just one year.

6. Dollar-based net expansion rate remains strong and reflects continued revenue growth

DBNE still remains among best in-class (Twilio’s Net Dollar Retention Rate is #8 among top 10 SaaS).

Twilio is conscious of not being able to maintain net expansion rate, and is conservatively predicting mid-to-high teens in January because of tough comparison of lapping SendGrid.

Competitors

Developers and enterprises alike love Twilio because of its easy-to-use UI/UX, and willingly pay their higher fees. Twilio’s pay-per-use business model allows them to capture increased revenue on the growth of their customers, and they’ve already penetrated many of the large unicorns like Uber and Airbnb and have successfully been hunting for other smaller companies such as Attentive to continue growth. Businesses will continue to want to communicate with their customers over various mediums: text, call, email, etc. and Twilio’s all-encompassing suite of products is the only service in the cloud communications space. No competitor competes across all product offerings.

Valuation

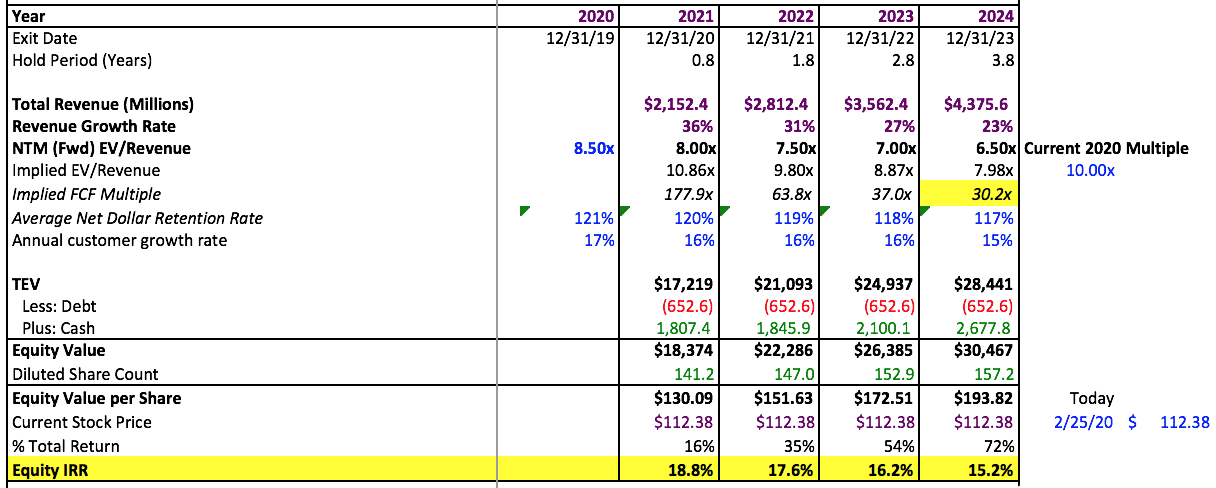

Since Twilio is still a growth SaaS company, it’ll likely get valued on a Next-Twelve-Month ARR multiple until it reaches maturity. Here, we attempt to match implied EV/Revenue multiples with a reasonable implied FCF multiple at maturity (2024). Given the multiple is currently depressed due to the coronavirus, and although management conservatively states revenues will grow 30-31% in 2020, we model revenues in 2020 using an average customer growth rate of 4.1% (qoq), with an average revenue per new customer of 1.9K, and net retention rate to remain around 120-124%. Using a forward revenue of NTM revenues, we believe Twilio is primed to grow at above 15.2% IRR over the next four years. We believe that at maturity, a 30x FCF multiple and an implied EV/Revenue multiple of 8x is reasonable, given 21.5% FCF margins.

My predictions for Twilio in 2020:

- Twilio will make an acquisition of a fast-growing startup in a segment of the cloud communications space where they currently do not operate

Twilio is currently holding an abnormal amount of cash and cash equivalents after issuing a 550M convertible bond in Q2 2019, despite previously having a healthy cash position.

Next avenue would be acquiring a developer-focused startup on a branch of cloud communications they do not currently compete in (Authy, Two-factor authentication in 2014; SendGrid, emails in 2019)

2. The 2020 Presidential election will prove to be a major catalyst for one-time revenues of Twilio’s service causing management to increase guidance

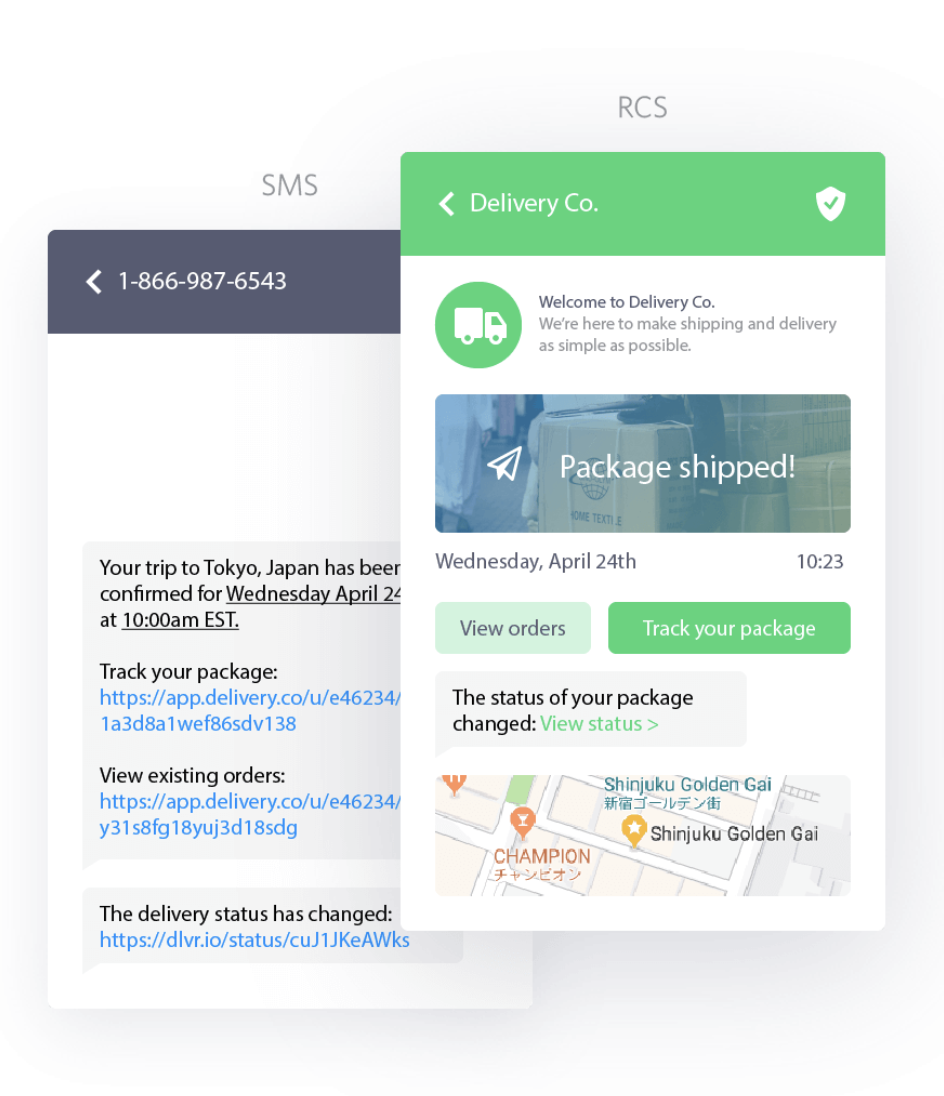

3. Twilio will expand into the RCS (Rich Communications Service) space:

Twilio has introduced support for RCS (same API, drag-and-drop features) to capitalize on an innovative mode of business-consumer communication.

RCS has existed since 2007, similar to iMessage or Whatsapp; it allows for a richer texting experience, with efficient group chats, embedded hd images, read receipts, etc.

Oct. 2019 Google took over efforts to integrate RCS fully in the US using CCMI with the backing of all four major network providers (ATT, Verizon, Sprint, T-Mobile). Despite RCS’s existence and its failure to reach the critical threshold for widespread adoption, Google will be the one to get this done.

Disclaimer: The author owns stock directly in TWLO. Public Comps (SaaSy Metrics LLC) provides financial and industry information and analysis regarding public software companies as part of our weekly dashboard, our blog, and emails. Such information is for general informational purposes only and should not be construed as investment advice or other professional advice.