Netskope Goes Public: A New Era for Cloud Security

IPO and Market Significance: Netskope went public at a $7.3B valuation, marking a rare cybersecurity IPO and signaling maturity in the SASE (Secure Access Service Edge) market.

Business Model and Platform Strength: Operates a subscription-based SaaS model integrating CASB, SWG, ZTNA, and DLP into a unified, data-centric SASE platform—offering enterprises a consolidated, cloud-native security solution.

Competitive Positioning: Competes against Zscaler, Palo Alto Networks, and Cloudflare by emphasizing deep data protection, flexibility, and a customer-centric approach, though it faces challenges in brand recognition and scale.

Financial Performance: Reached $800M+ ARR with ~30% YoY growth and strong gross margins (~70%), but remains unprofitable due to heavy R&D and sales investments aimed at accelerating growth and innovation.

Outlook and Strategic Priorities: Future success hinges on balancing growth with profitability, expanding internationally, cross-selling across its platform, and achieving sufficient scale to become the top alternative to Zscaler in the SASE market.

Netskope made headlines in September 2025 by going public at a $7.3 billion valuation, making it the second cybersecurity company to brave the IPO markets in the past year alongside Rubrik. Founded in 2012, the company grew into a leading position/role in Secure Access Service Edge (SASE). The company combines networking and security into a unified cloud-native platform. Unlike its peers, often ending up acquired by large incumbents, Netskope took the road less traveled and opted for independence and the scrutiny of public markets.

In this Article, we break down Netskope across several factors including:

- Growth in the cybersecurity space

- Business model and primary product offerings

- How they compete in the ever-changing cybersecurity landscape

- Financial growth and SaaS metrics

- Outlook for the coming years

Growth in the Cybersecurity Space

Netskope has spent over a decade building credibility in one of the fastest-evolving areas of cybersecurity. The company capitalized early on the shift to cloud-based applications, remote work, and the increasing need for real-time visibility. This visibility expanded into user activity across SaaS, IaaS, and web environments.

SASE became their anchor to success and grew alongside the changing SASE market. As enterprises moved beyond traditional perimeter security, Netskope’s platform delivered secure and seamless access from anywhere. This offering significantly accelerated revenue growth during and after the COVID-driven remote work surge. Over the years, Netskope is consistently featured as a leader in Gartner’s Magic Quadrant for SSE (Security Service Edge), helping it cement a reputation for innovation and execution.

Netskope is backed by Lightspeed Venture Partners which currently owns 19.3% of the business. Lightspeed is a top tier venture firm that adds credibility for continued revenue growth and market share gains as a public market company.

Business Model and Product Offerings

Netskope runs a subscription-based SaaS model, primarily targeting mid-market and enterprise customers that are modernizing their security architecture. This model ensures predictable recurring revenue while giving enterprises the flexibility to scale usage as their networks and security needs evolve. What sets Netskope apart is the breadth and integration of its platform. Instead of focusing on single point solutions, Netskope delivers a suite of products that converge into its Secure Access Service Edge (SASE) framework that delivers seamless management from an integrated platform no matter where the user is. Here is a closer look at its major offerings:

Secure Access Service Edge (SASE):

At the core of Netskope’s strategy is its SASE platform, which unifies networking and security into a single cloud-delivered service. Rather than forcing enterprises to stitch together multiple vendors, SASE allows secure, optimized access to cloud applications, private apps, and the open internet. Netskope’s global private cloud, the Netskope NewEdge network, underpins this offering by ensuring low-latency performance worldwide. This architecture differentiates Netskope as competitors often rely more heavily on public infrastructure rather than a private cloud.

Cloud Access Security Broker (CASB):

Netskope started as a CASB provider which remains a critical strength. CASB gives organizations visibility into SaaS applications, including everything from sanctioned tools like Microsoft 365 to shadow IT usage. Beyond visibility, Netskope offers granular controls, such as blocking high-threat file uploads, monitoring data sharing, and enforcing compliance with regulations. This deep heritage in CASB gives Netskope a data-centric advantage to best help customers, as enterprises grapple with sensitive information spread across cloud apps.

Secure Web Gateway (SWG):

The SWG component provides protection against internet-borne threats including malware, phishing, and malicious websites. Netskope delivers this as a cloud-native service, unlike traditional on-premise SWGs, which means users are always protected regardless of location. Like most of Netskopes tool’s, SWG is tightly integrated with other offerings such as Netskope’s CASB and DLP. This integration allows policies to be enforced consistently across web traffic and SaaS applications, something legacy vendors often struggle to deliver.

Zero Trust Network Access (ZTNA)

ZTNA is Netskope’s modern replacement for the VPN. Instead of giving users broad access to a corporate network, ZTNA enforces identity-based, least-privileged access to specific apps and resources. This not only strengthens security but also improves the user experience by providing seamless, secure connectivity from anywhere. As hybrid work continues to grow, ZTNA becomes a centerpiece of enterprise security strategies. Netskope is successfully competing head-to-head with the largest players in the domain including Zscaler and Palo Alto Networks. While Netskope is a high-growth company, gaining incremental enterprise customers to further grow ZTNA market share will be difficult against entrenched competitors such as Zscaler and PANW.

Data Loss Prevention (DLP)

Data protection is a meaningful differentiator for Netskope. Its DLP capabilities extend across SaaS, web, and private applications, helping organizations prevent sensitive data, whether it is intellectual property or financial records, from being leaked or exfiltrated. Netskope employs advanced classification techniques, including machine learning-based pattern recognition, to monitor and control data movement in real time. This feature resonates strongly with regulated industries like healthcare, finance, and government.

By bundling these offerings into a single, cloud-native platform, Netskope positions itself as more than just another cybersecurity vendor. Its strategy is to be the consolidation play for enterprises tired of juggling multiple point products and vendors. Customers don’t just get layered defenses, but they get a unified control plane for cloud, web, and private applications. This is both Netskope’s competitive advantage and its growth engine in a market increasingly demanding efficiency and simplification.

Competitive Landscape

Netskope operates in one of the most competitive areas of cybersecurity, where networking and security converge. Its primary competition comes from both born-in-the-cloud companies and large, diversified incumbents. Giants like Zscaler, Palo Alto Networks (Prisma Access), and Cloudflare dominate the conversation, while traditional players such as Cisco and Fortinet continue to leverage their existing installed bases to push cloud-delivered security.

Zscaler: Perhaps Netskope’s most direct competitor, Zscaler pioneered the cloud-native secure web gateway and is often the first company mentioned in enterprise SASE/SSE discussions. Zscaler’s strength lies in its massive scale, larger customer base, greater global footprint, and deeper brand recognition as a public company since 2018. However, Zscaler’s heritage is more network security-focused, whereas Netskope’s background in CASB and DLP gives it a data-centric differentiation. Netskope positions itself as stronger in visibility and compliance, areas where enterprises handling sensitive data (finance, healthcare, government) may find it more compelling.

Palo Alto Networks (Prisma Access): Palo Alto brings the weight of an established cybersecurity giant with the credibility of tens of billions in market cap. Prisma Access is part of Palo Alto’s broader strategy to evolve from a hardware-centric firewall business to a cloud-based security platform. The advantage here is enterprise trust and brand reputation—Palo Alto can leverage long-standing customer relationships and cross-sell Prisma alongside its massive suite of products. The downside is that Prisma, while broad, is sometimes seen as less agile and more complex than pure-play solutions like Netskope. Netskope tries to exploit this by emphasizing flexibility and simplicity in deployment.

Cloudflare: Cloudflare has emerged as a formidable challenger by extending its global content delivery and networking infrastructure into security. Its Cloudflare One platform bundles Zero Trust, SWG, and SASE-like features at highly competitive pricing. Cloudflare’s edge is scale and performance, its global network rivals the largest CDNs, ensuring extremely low latency. For cost-sensitive customers, this makes Cloudflare attractive. Netskope differentiates by highlighting depth over breadth, particularly in advanced data protection where Cloudflare lags behind.

Cisco and Fortinet: While not pure SASE leaders, traditional networking vendors like Cisco (Umbrella, Duo, ThousandEyes) and Fortinet are significant competitors due to their installed base. These companies can bundle security into existing hardware and networking deals, making them tough to displace in accounts already loyal to their ecosystems. Netskope’s challenge is proving that its cloud-native architecture and integrated platform deliver more value than bolt-on offerings.

Netskope’s Differentiation: Despite facing well-capitalized and widely recognized rivals, Netskope has carved out distinct advantages:

- Depth of Data Protection: Its CASB and DLP foundation gives Netskope unmatched visibility into SaaS and data usage. Competitors often approach security from the “outside-in” (network-focused), while Netskope works from the “inside-out” (data-focused), a differentiation that resonates in compliance-heavy sectors.

- Flexibility and Customer-Centric Design: Netskope avoids rigid deployment models. Whether customers need a full SASE platform or just CASB/SWG, Netskope offers modularity that allows gradual adoption. This approach is attractive to enterprises in transition.

Even with these strengths, Netskope faces hurdles:

- Scale: Competitors like Zscaler and Palo Alto operate at a larger revenue base and customer footprint. Netskope must continue to expand rapidly to close the gap and capitalize on the platformization trend.

- Brand Recognition: Many CISOs default to Palo Alto or Zscaler when evaluating SASE. Netskope’s IPO helps grow recognition, but building mindshare at the executive level remains critical.

- Profitability Pressure: Competing in this market requires heavy R&D and sales investment. Balancing growth with a path to profitability will determine whether Netskope can sustain its momentum as a public company.

Financial Success

At IPO, Netskope’s valuation of $7.3 billion reflected both optimism and scrutiny. The company crossed $800M+ in ARR, growing at ~30% year-over-year leading up to the listing. With strong gross margins in the 70% range, we predict these margins to continue to expand in the coming years. However, like many SaaS cybersecurity companies, Netskope was still operating at a net loss, driven by heavy R&D and sales investments. This does not discourage our bullish belief as in order to compete with PANW and Zscaler, Netskope must invest heavily in their product offerings and keep up with market trends. Their upsell strategies are also helping them grow as they have a 118% net dollar retention with over 85% of ARR coming from $100K+ customers.

The key question for public investors is whether Netskope can balance continued growth with a path toward profitability—something its closest peer Zscaler has started to demonstrate in recent years.

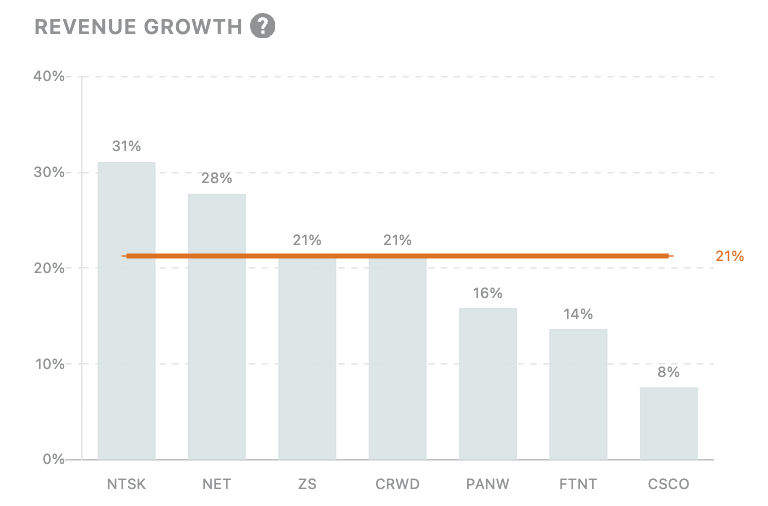

Compared to its competitors, Netskope demonstrates the strongest revenue growth, underscoring its robust market momentum. This trajectory is encouraging, and I expect the company to sustain its elevated growth rate over the coming year.

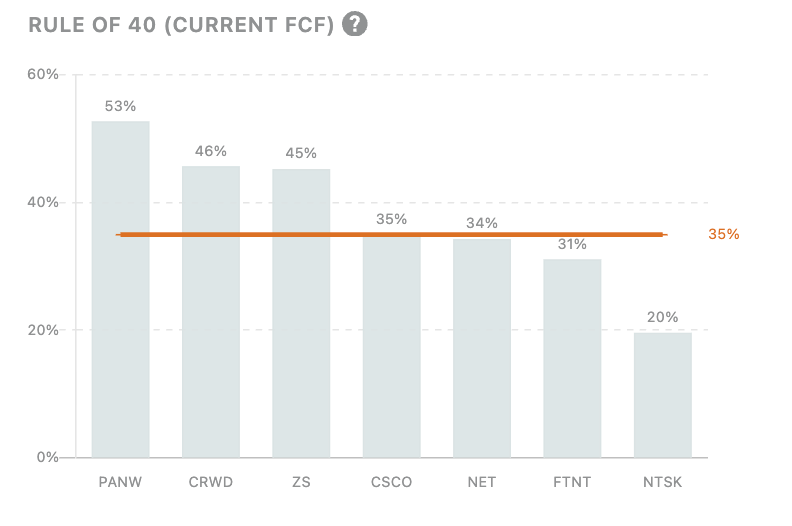

While Netskope’s revenue growth remains strong, its Rule of 40 performance is below expectations. The company’s heavy investment in R&D could raise concerns that it is trying to catch up with competitors. However, I view this spending differently — Netskope’s substantial R&D investment likely reflects a strategic effort to strengthen its platform and position itself for accelerated market share gains in the coming months and years.

Outlook: Where Netskope Goes from Here

In the Near-Term Netkope will undergo Public Market Scrutiny and need to navigate the discipline of quarterly earnings. Pre-IPO, growth-stage cybersecurity companies have the freedom to focus on topline expansion at the expense of profitability. But the public markets demand both growth and operational discipline. Investors will want to see whether Netskope can sustain 25–30% annual growth while simultaneously improving operating leverage and reducing the gap between revenue growth and net losses. This will be extremely important and difficult in the first 12 months of operation, but as Netskope gains momentum we believe they will be able to maintain their growth.

This balancing act is tricky. Cybersecurity remains a land-grab market, and the temptation will be to spend aggressively on R&D and sales to defend share against competitors like Zscaler and Palo Alto. But if Netskope overspends, Wall Street could penalize the stock, compressing its valuation. In the near term, the company’s credibility will rest on demonstrating that it can execute consistently, land larger enterprise deals, and expand internationally without runaway costs.

Over the next three to five years, Netskope’s growth engine will depend on a combination of:

- Expanding Internationally: The NewEdge network already gives Netskope global reach, but continued investment in local data centers and channel partnerships will be critical for adoption in Europe, APAC, and Latin America.

- Cross-Selling Across the Platform: Many customers initially buy Netskope for CASB or SWG. The company has significant upsell potential by layering in ZTNA, DLP, and full SASE functionality. Increasing wallet share within existing customers will be as important as landing new logos. PANW, one of the most successful cybersecurity companies, relies heavily on cross-selling and up-selling, and in order to reach their realm of success, Netskope must continue to grow its current 118% NRR.

- Enterprise Consolidation: Large organizations are actively consolidating vendors to reduce complexity and costs. Netskope’s integrated platform is well positioned to be on the “shortlist” when enterprises rationalize their security stack, but need to maintain their top of the line offerings that integrate across the platform.

Looking further ahead, Netskope could emerge as a true platform consolidator in the SASE market. As enterprises demand fewer, stronger vendors, Netskope’s data-centric approach gives it a unique position relative to network-first rivals. If the company can achieve sufficient scale, it could become the go-to alternative to Zscaler in pure-play SASE, much like CrowdStrike became the go-to in endpoint security alongside Palo Alto. That said, Netskope’s mid-market size remains a concern. Without achieving sufficient operational scale and profitability, it risks being overshadowed by larger, better-capitalized competitors that can outspend them on go-to-market initiatives and customer acquisition.

That said, competition is relentless. Palo Alto Networks continues to invest billions into cloud security and can bundle Prisma with its firewalls. Cloudflare is rapidly evolving from CDN to security platform and could undercut Netskope on cost and scale. Zscaler, with its first-mover advantage and public track record, will continue to set the benchmark Netskope must measure itself against.

Beyond Netskope itself, this IPO is symbolic. Cybersecurity startups in recent years have overwhelmingly exited through acquisitions rather than public listings. Netskope’s decision to go public, and how it performs, will be a bellwether for the sector. A strong performance could re-open the IPO window for other late-stage cybersecurity firms. A weak one could reinforce the narrative that only the largest incumbents or platform companies can survive independently.

Netskope’s IPO is more than just a company milestone, but a signal of maturity for the SASE market and highlights the expanding exit opportunities for cybersecurity companies. Netskope’s next test will be proving that it can sustain growth, balance profitability, and compete at scale. If it succeeds, it won’t just be a win for the company, but could reshape how cybersecurity companies think about their long-term exit strategies. Shifting from the historic acquisition exit to the IPO path would cause a major change within the cybersecurity space and I am excited to follow their independent growth in the coming years.