Slack IPO & S-1 Teardown

Slack (WORK) is going public. We benchmark Slack against the other fastest growing Public SaaS companies using our data platform from publiccomps.com.

Slack (WORK) is going public this Thursday, June 20th via a direct listing. We benchmark Slack against the other fastest growing Public SaaS companies using our data platform from publiccomps.com.

💬Description: Slack provides software that allows users to communicate, collaborate and get work done. Company claims it replaces the use case of email inside organizations and turns conversations happening in individual email inboxes to team-based channels to provide transparency and a better record of conversations, data and documents. Slack bills itself as a new layer of the business technology stack that brings together people, applications, and data into one application.

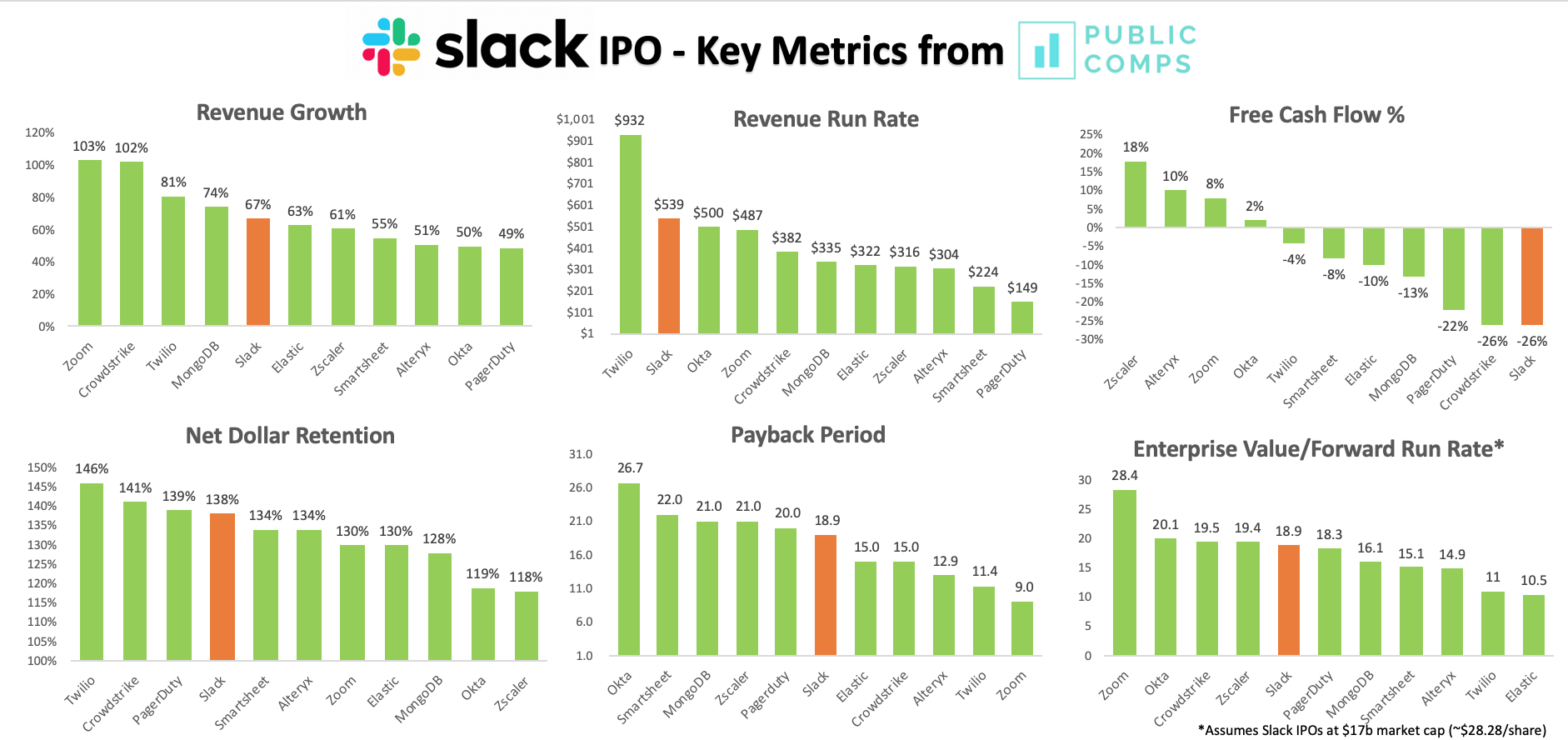

🔥 Revenue Growth: Slack is growing 67% YoY which puts it in the top decile of Public SaaS companies. We benchmark against the Public SaaS top quartile software growth companies like Crowdstrike, Zoom, Twilio, MongoDB, Elastic, Zscaler, Smartsheet, Alteryx, Okta, Pagerduty.

👍Revenue Scale: Not only is Slack in the top decile of growth, Slack is also the 2nd largest public software company in our benchmark cohort at $539m ARR. It's impressive Slack continues to grow at its current scale.

📈Best-in-class Net Dollar Retention: Slack's 138% net dollar retention, as of April 30, 2019, is best-in-class and is a reflection of the number of paid seats increasing within an organization due to word of mouth because of love for product, built in distribution for communication platforms, and sales + customer success team.

⏳Acquiring customers via self-service + sales model: Payback period is ~19 months which isn't best-in-class but still good. Slack's GTM benefits from Slack investing in its free subscription product that users can easily get started on to realize the value of Slack. Additionally, Slack has a sales team + customer success to drive adoption, converting free > paid and upsell particularly in larger accounts — this also drives a strong net dollar retention.

💸Negative Free Cash Flow % Margin: At -25% Free Cash Flow margins, Slack has the lowest FCF % among our top quartile SaaS companies. What I found interesting was that Slack had -$97m FCF in CY2018 (year before it went public) and Dropbox, which has a similar self-service business model, had +$305m FCF in CY2017 (year before it went public). This may be a function of Slack still growing 67% YoY at $539m ARR and investing heavily in S&M to continue to grow whereas Dropbox was only growing at 28% YoY at $1.2b ARR when it went public.

💰 Valuation Expectation: Slack is apparently pricing at ~$28/share or $17b market cap - $841 of cash ~$16.2b of enterprise value. That'll price Slack at around ~19x EV/Forward ARR which is up there with the other high growth SaaS companies. Crowdstrike seems to be the best comp given they're both negative FCF % but its worth noting that Crowdstrike is growing 35%+ faster.