Twilio Q4'23 - Pre-Earnings Refresh

We share context on $TWLO and where its today, how to think about the departure of Jeff Lawson, and updates on the key business metrics ahead of Q4'23 earnings.

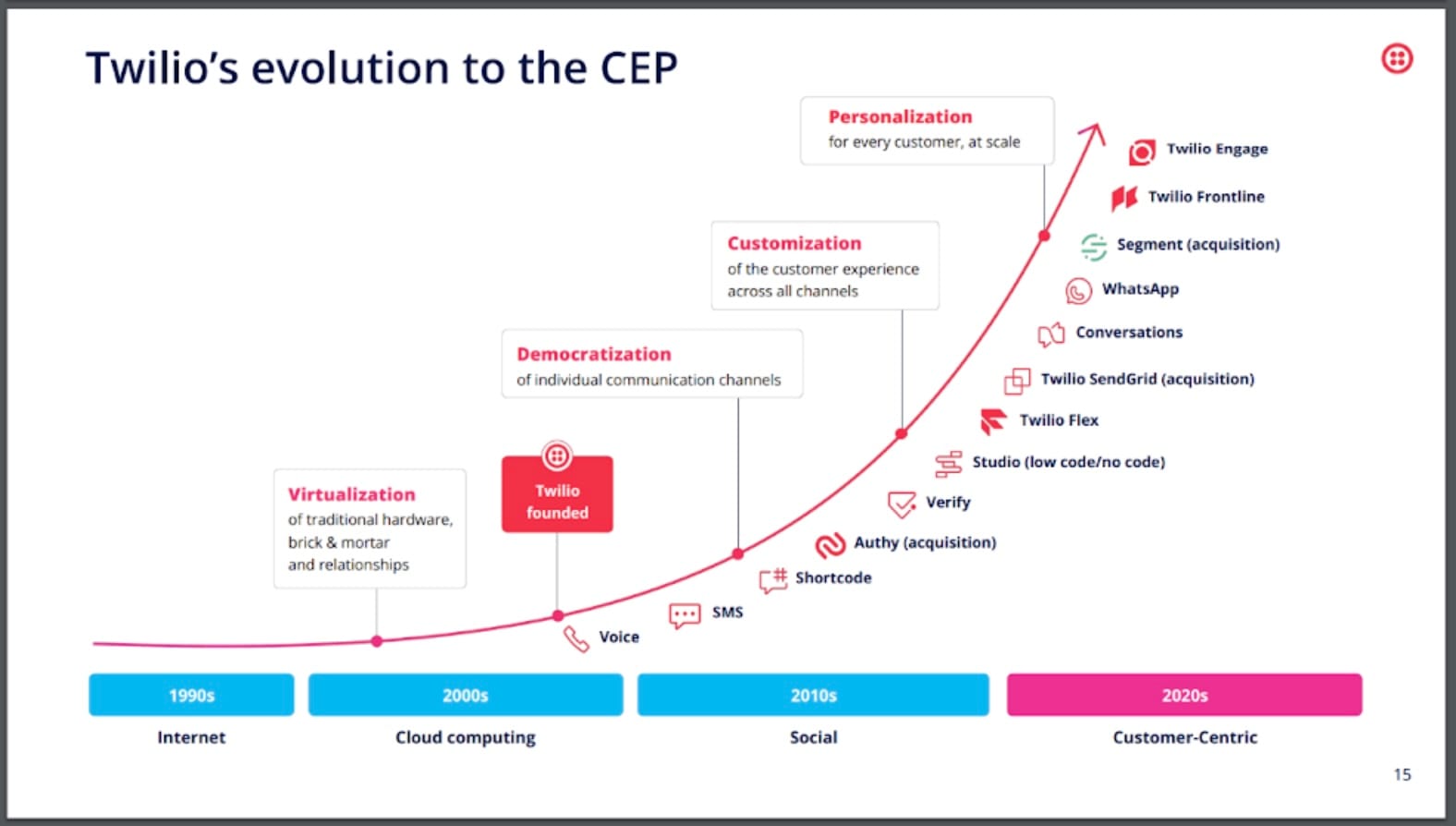

Company Overview

Twilio is a Communications Platform as a service (CPaaS) business that allows enterprises to embed communication channels (voice, text, email, etc.) into their applications. Twilio’s platform can be separated into 2 key product lines (restructured in Feb 2023), Communications and Data & Applications (formerly known as “Software”). Twilio is considered one of the industry leaders in cloud communications due to its suite of comprehensive communication tools: text, phone/voice, email, video, etc.

Communications (~78% revenue)

- Customizable API’s that can be used to build contextual communications applications in the following channels: text, phone/voice, email, and online messaging. Core Offerings include:

- Programmable Messaging: API to send/receive SMS,MMS, etc

- Programmable Voice: API to allow developers receive calls via browser/app/phone

- Email (SendGrid): API to solve email delivery challenges

- Account Security: Twilio verify, uses two-factor authentication

Data & Applications (~12% revenue)

- Building off its communications segment, the data & applications solutions allow companies to create personalized experiences and campaigns using real-time customer data.

- Twilio Segment: The Customer data platform; collects first-party data across various channels (websites, mobile apps, digital ads, etc), uses the data to profile customers, then drive personalization

- Twilio Engage: Builds on Twilio Segment to help marketers create personalized campaigns

- Twilio Flex: Virtual contact center so companies can have a wide range of customer engagement channels

- Marketing Campaigns: Meant to help marketers specifically build email campaigns

Competitors

Broader Context

Before diving into earnings and financials, I think it’s worth discussing some broader contextual trends that help us understand why $TWLO is trading below pre-pandemic prices and how it’s valued today.

Let’s go back to 2020, at the onset of the COVID pandemic. While the COVID-19 pandemic initially brought down the markets as a whole, there were 3 macro trends that fueled rapid stock appreciation for tech stocks (ie, software, fintech, internet, etc): massive monetary stimulus, zero interest rate policy (ZIRP), and bullish expectations on B2B SaaS and e-commerce as a result of lockdowns and remote work. Naturally, at this point in time, Twilio was considered the darling of the software space and traded at a premium multiple, which Twilio would use to make a string of acquisitions to fuel growth.

However, at some point, the party has to stop; as inflation began spiking in late ‘21 and early ‘22 as a result of massive stimulus and the Ukraine war affecting commodity prices and supply chains, the Fed pivoted and 10x’ed the federal funds target rate in less than a year. We went from “risk-on” to “risk-off”, from “growth at all costs” to “profitability”, and as a result, $TWLO’s business model (like most software businesses) was scrutinized and valuation tumbled as growth slowed.

Lastly, as it pertains to management, it’s definitely worth mentioning how investors’ perspective of Jeff Lawson, former CEO, changed throughout this period. Lawson was once considered one of the best software CEOs and visionaries, but June 2023 was a milestone that many investors marked for Twilio as Lawson’s super voting rights expired, and many correctly speculated there would be a potential activist campaign and/or private transaction take.

Management Update

Unable to rejuvenate growth and reverse a stagnated stock price, Jeff Lawson announced his resignation on January 8th, 2024 after pressure from (Legion Partners and Anson Funds) to divest the entire company (or at minimum, the software segment) and prioritize profitability. The broader sentiment was that while Lawson did well to grow the company as a startup and develop strong products, he struggled with prioritizing profitability and sustaining growth in recent years, which seems to be key reasons for his ousting. Different times call for different strategies - some people are more fitted for growth at all cost vs. profitable growth.

$TWLO was up ~7% the day of the announcement, but I suspect this was not the pop or catalyst that the activist investors clearly are looking for. Khozema Shipchandler, former President of Twilio Communications, is replacing Lawson as CEO, and it’ll be interesting to see where he takes the company and how he responds to the current issues facing the company.

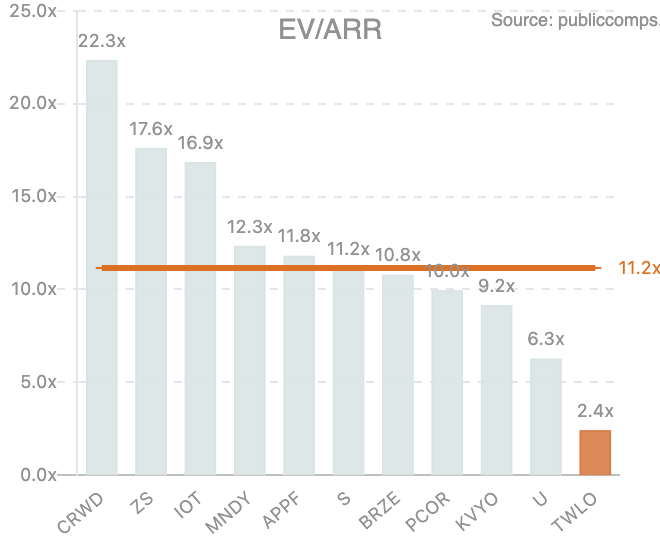

Financials and Valuation

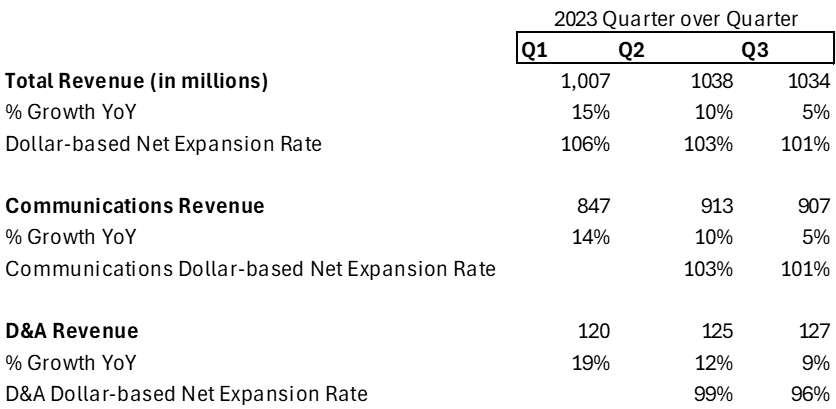

Quarterly Earnings

Revenue Trends

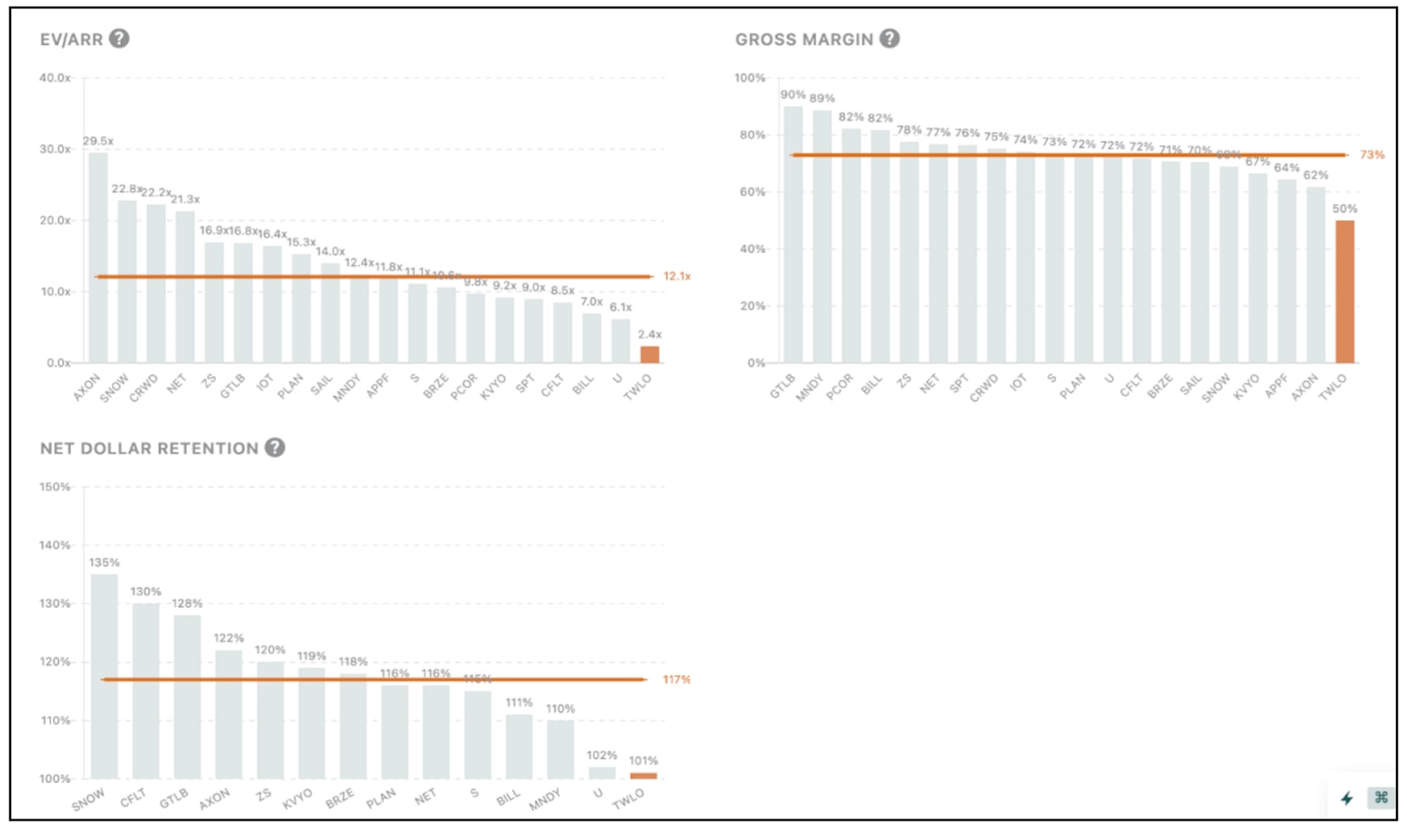

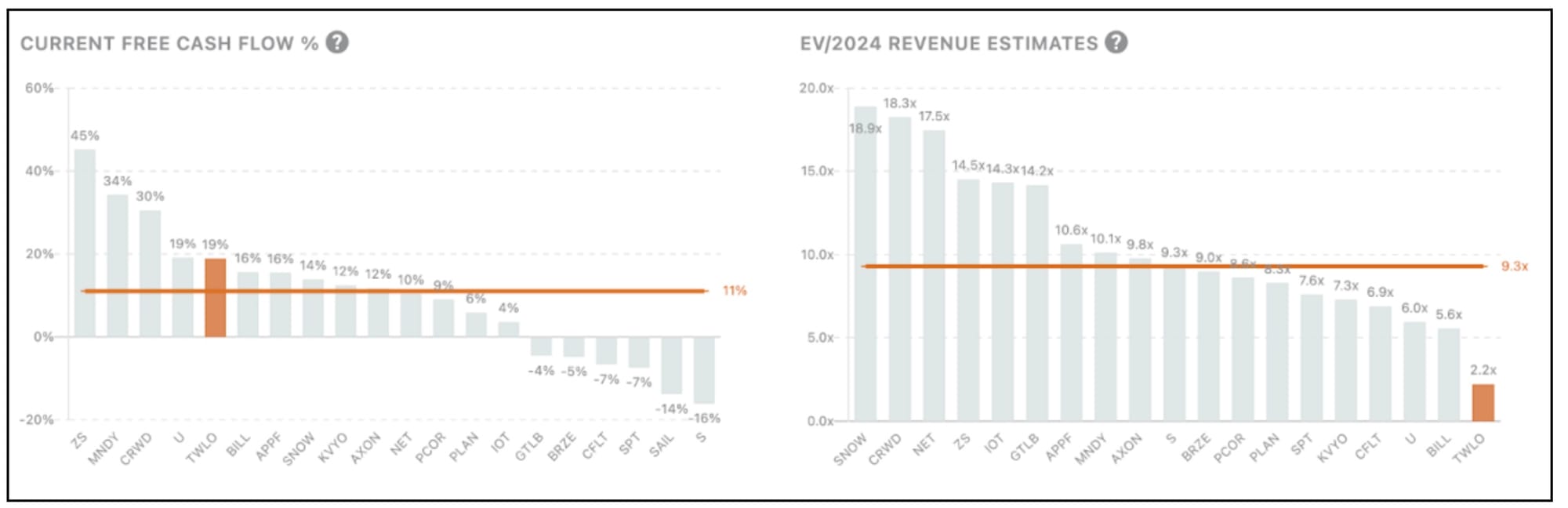

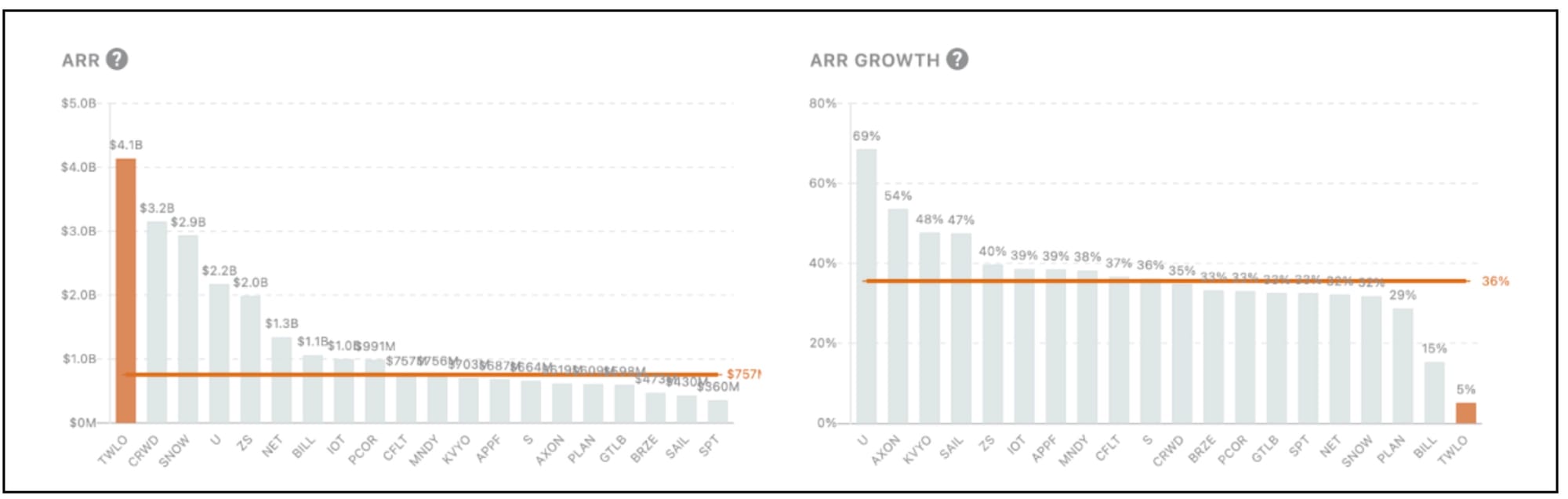

Key Metrics

Takeaways

3 key takeaways from the financials.

- First, revenue growth rates have clearly come down. Where Twilio had extremely high growth rates (>60%) during the pandemic and the ZIRP (zero interest rate policy) era, growth rates have steadily come down and appear to be hovering around 10%. With recent rounds of layoffs and change in leadership, I find it hard to see a situation where Twilio regains growth momentum.

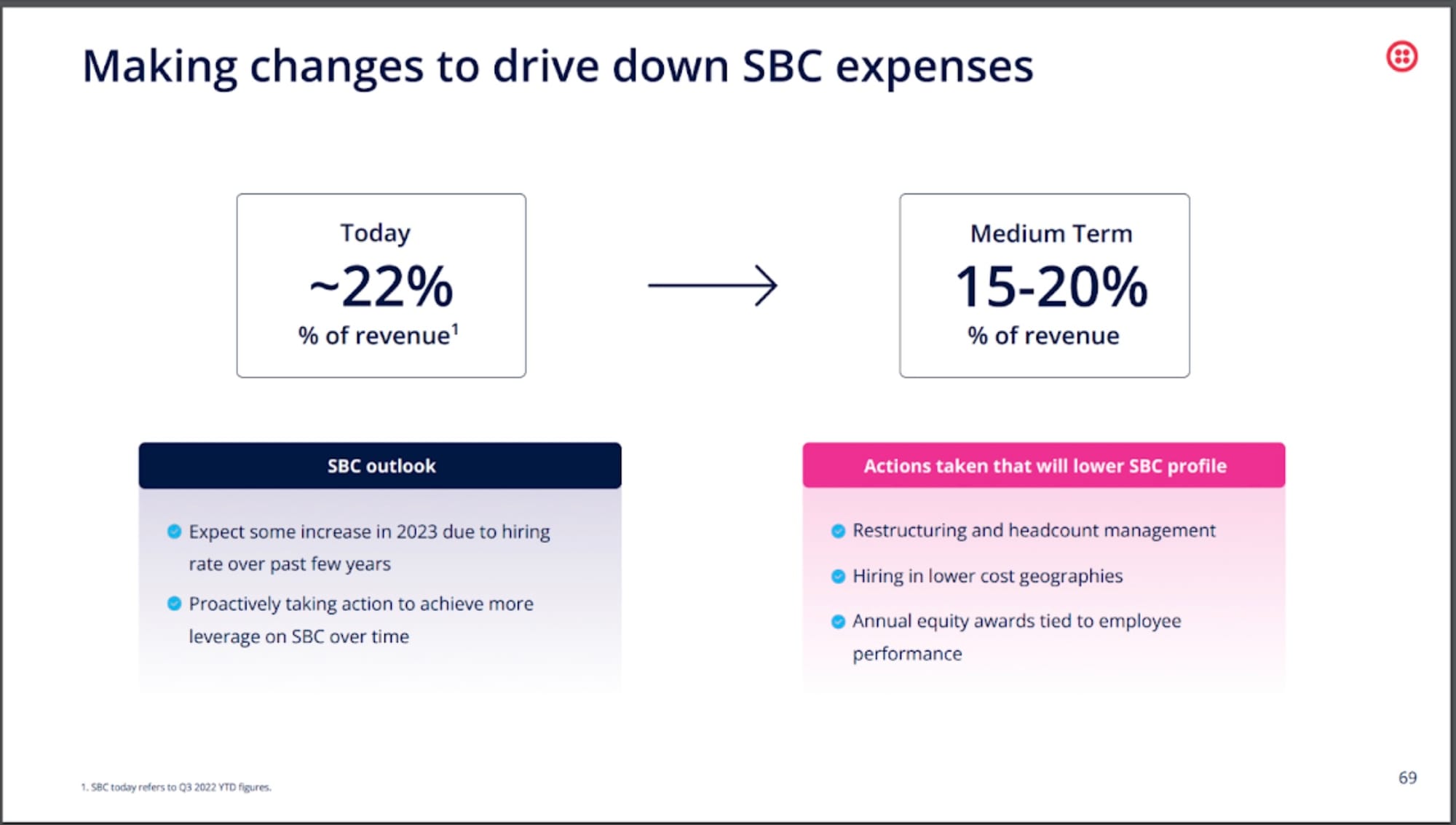

- Second, Twilio has consistently had a margin problem. Its gross margin has historically hovered around 50%, the lowest gross margin among our “Top 10 SaaS’ benchmark. This is often attributed to paying expensive telecom fees to network service providers, as well as the “messaging” segment having a lower gross margin compared to the more truly “software” segments. On top of all this, Twilio’s stock-based compensation is notoriously high, sitting at ~20% of revenue, hurting a gross margin that’s already below the industry average.

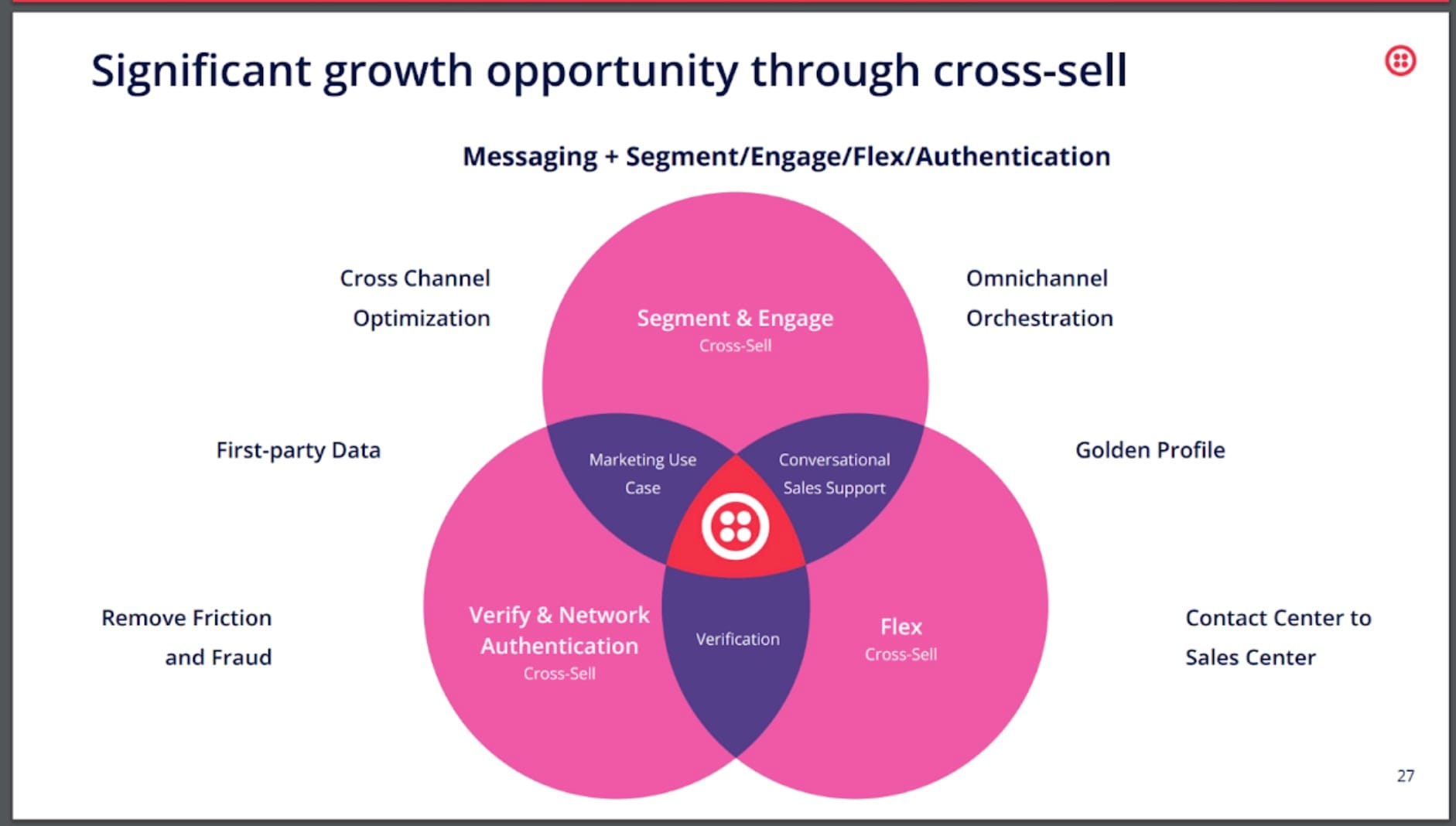

- Third, Twilio’s dollar net-based expansion rate is down near 100% and the lowest among “Top 10 SaaS”, an indication that Twilio is struggling to cross-sell among its existing customer base. While Twilio sees its Data & Applications portion of the business with the most opportunity to cross-sell, the fact that that portion of the business is both smaller and has seen less growth helps explain the low expansion rate.

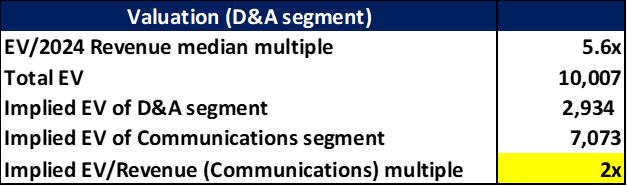

Valuation

As it relates to valuation, the markets view $TWLO as two businesses; one software and one tech-enabled services (communications). If we assume it’s feasible to separate the two segments (which will be discussed below), the markets are valuing the communications at 2x revenue and 10x gross profit (assuming a 20% margin). While the implied multiples are below multiples traditionally prescribed to software companies, it seems like a fair valuation for a business that’s low growth and low margin, begging the question if the communications segment can be valued as a “true” software company.

That being said, it's a fair debate on whether or not we can separate the two business segments. From my perspective, Twilio started its business with communication APIs, and as the business grew overtime, Twilio saw an opportunity to help enterprises develop the data platforms and customer engagement (think marketing campaigns, customized campaigns, etc.) off of their existing customer channels. I think there are strong synergies and cross-selling opportunities between the two, and for the same reasons I find it hard to believe that a buyer would only buy the “data and applications” portion of the business, I think it may not be the best idea to value the two businesses separately.

Outlook for 2024

Going into 2024, especially with Q4 ‘23 earnings and the annual report release on February 14, here are two key themes we’re paying close attention to.

First, we expect a strong focus on profitability. Absent high growth, Twilio’s best play is to maintain discipline and cut costs. Since 2022, we’ve seen 3 rounds of layoffs, shrinking headcount by ~26%. As per their 2022 Investor Day presentation, Twilio focused on reducing opex by restructuring the business, layoffs, and shifting to “remote-first”, and we’ll see how much it paid off come February.

Second, and more interestingly, we’re looking to see how Twilio will respond to pressure from activist investors to divest. Legion Partners and Anson Funds are pushing for a buyout, or at least divesting the Data & Applications (formerly software) portion of the business, which clearly played a role in Lawson’s ousting. From our perspective, It’s hard to see a potential buyer for solely the software side of the business, so if there is a divestment, it most likely will be a buyout from a private equity fund, similar to Zendesk’s buyout in June 2022 after pressure from activist investor Jana Partners. In any case, we’ll be looking to see how the new CEO, Shipchandler, leads the company in response to activist pressure.

Cheers,

Noah Kim

Like these teardowns? These are for Publiccomps.com customers only but you can have your friends subscribe to the newsletter here where we send out investment memos, market maps, and analyses on the broader tech market.

Views expressed in these emails are ours and ours alone and don’t represent that of our previous or current employers. Public Comps provides financial and industry information regarding public software companies as part of our weekly dashboard, our blog, and emails. Such information is for general informational purposes only and should not be construed as investment advice or other professional advice.