Weekly Dashboard 11/6/2020: AYX Q3 2020 Earnings Teardown

👋 Public Comps Customers 👋

What a week – crazy election volatility and the start of B2B SaaS earnings (which saw some great ones). This week, we break down AYX's Q3 2020 earnings.

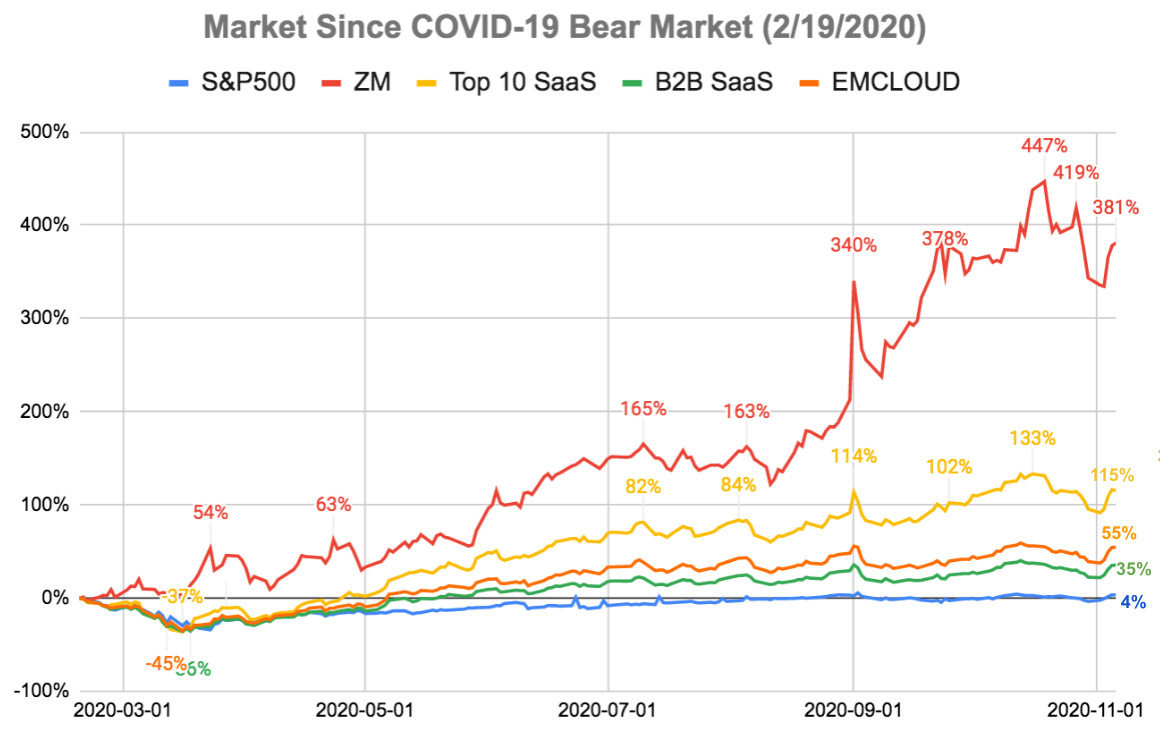

1️⃣ SaaS Stock Prices vs. Benchmarks 📊

Change since bear market start (2/19/2020):

- ZM: +381%

- Top 10 SaaS: +115%

- Bessemer Cloud Index (EMCLOUD): +55%

- B2B SaaS: +35%

- S&P 500: +4%

Change in the past week:

- ZM: +8.5%

- Top 10 SaaS: +10.1%

- Bessemer Cloud Index (EMCLOUD): +11.0%

- B2B SaaS: 10.5%

- S&P 500: +7.3%

Market update 📈: Despite the lack of a clear winner following election night on Tuesday, SaaS stocks, largely driven by Wednesday's sharp rise posted their largest weekly rally since April. With Biden appearing to have the clearest path to victory and Republicans seeming likely to retain control of the Senate, investors began to anticipate a scenario of additional fiscal stimulus but more limited tax increases than under a “blue wave” Democratic sweep. Higher beta stocks outperformed, as the market saw substantial rise following post-election day.

Interestingly, value stocks outperformed high-valuation growth companies early in the week, but the momentum that has driven many growth stocks higher all year took control following the election. In SaaS markets, many stocks that have reported earnings saw healthy and/or accelerated top-line growth (BIGC, TWLO, NET all saw moderate revenue acceleration) as digitalization trends that were heavily anticipated in the early onset of the COVID-19 pandemic started taking effect.

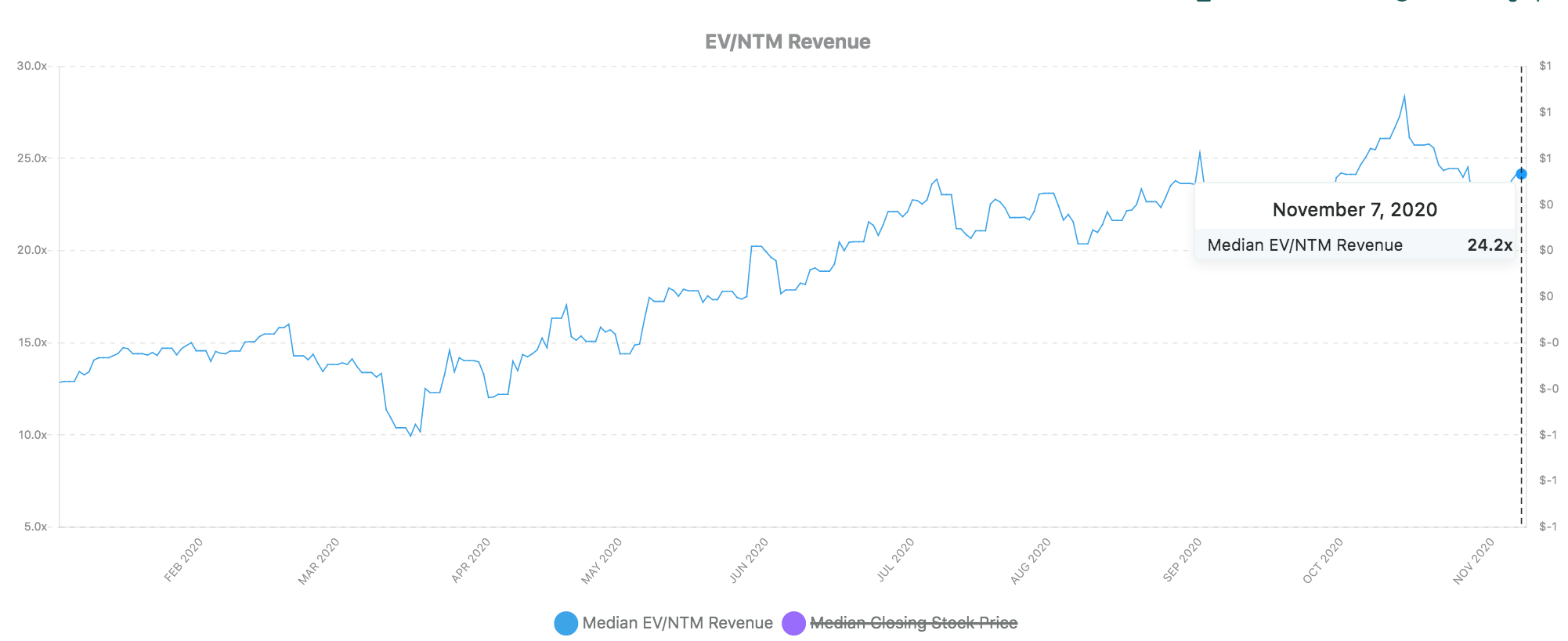

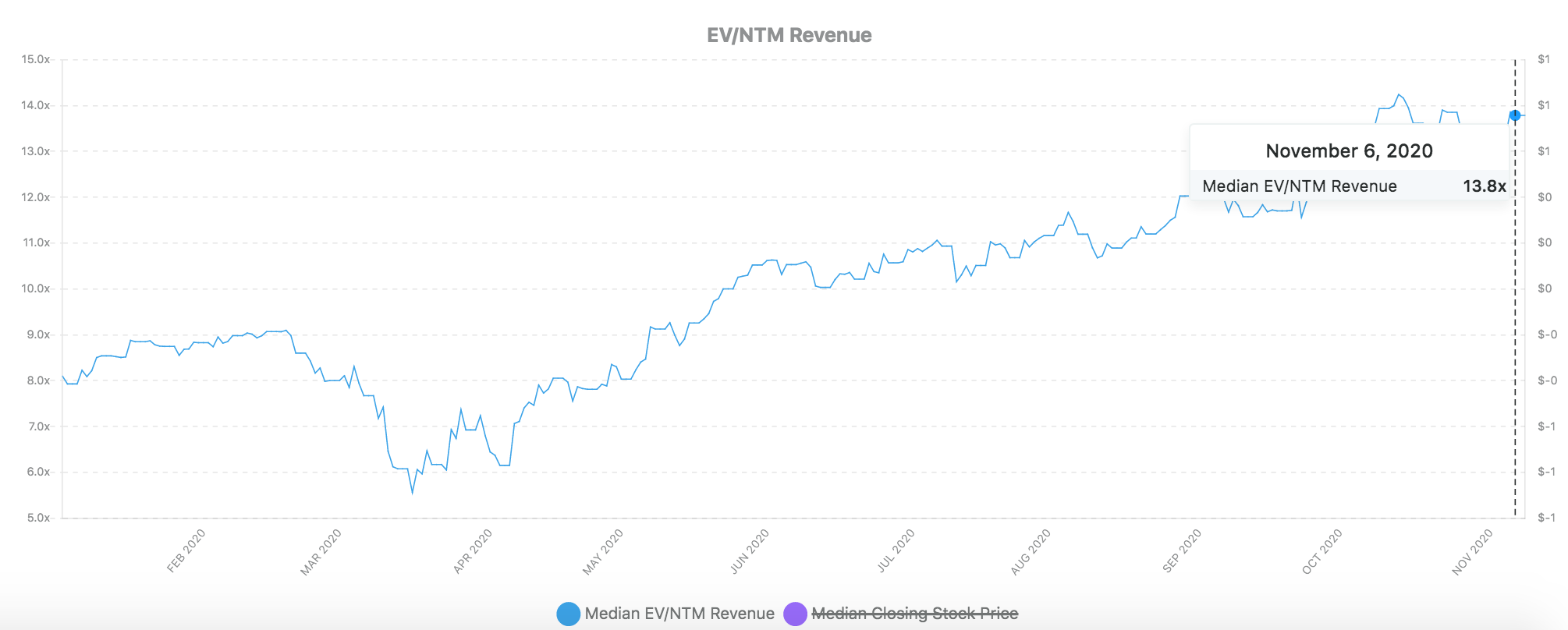

2️⃣ Median B2B SaaS EV/NTM Revenue Valuation Multiples

High growth SaaS: 24.2x

All B2B SaaS: 13.8x

3️⃣ SaaS Earnings - Alteryx (AYX) 💸

Company Overview:

Alteryx (leader in data tooling) is a no-code & self-service analytics tool for data analysts and data scientists to join, clean and prepare data for analysis and visualization. Business teams at some of the largest companies use Alteryx to clean & process large datasets that can't be analyzed in just Excel so the teams can get insights from their data in minutes versus weeks.

Alteryx delivers value to its customers because businesses are not only up-skilling knowledge workers to become citizen data scientists, but they're also increasingly leveraging analytics and automation to run smarter.

In their Q3 2020 Earnings, they allude to customers that specifically call out these three trends: 1) business transformation initiatives are being accelerated due to the COVID pandemic; 2) companies are struggling to leverage the massive influx of data, cascading in and around their businesses every day; and 3) legacy systems and manual processes are slowing down these transformations, often, separating the winners from the losers in this new age. These trends are real and aligned with the value that the Alteryx APA platform delivers.

Industry Overview:

- Market Opportunity: According to the IDC, over a trillion dollars is expected to be invested in data-related transformation initiatives. Alteryx believes they have a significant opportunity ahead, defined by the $49 billion total addressable markets, and believes they are still in the early stages of this explosion.

- Competition: Competitors include older incumbents like IBM, Microsoft, Oracle, SAP, Tableau, SAS, Microstrategy, and TIBCO that offer some data preparation or analytics tools. Upstart data prep competitors include Dataiku, Trifacta, Paxata, Knime (Opensource). Alteryx's main competitors are really business analysts cleaning data themselves manually in Excel.

Earnings Call Highlights:

- Alteryx instated Mark Anderson as CEO on 10/5/2020, and interestingly Dean Stoecker (former CEO) did not make an appearance in the call.

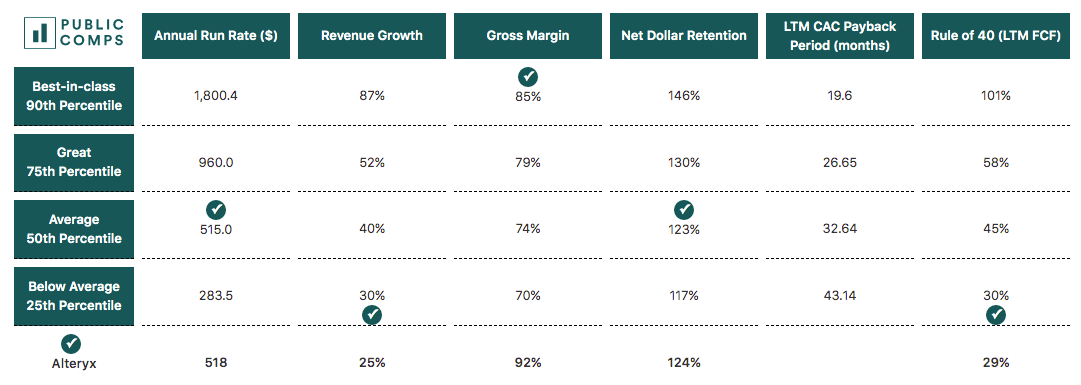

- AYX ended the quarter with ARR of $450M, +38% y/y and 129.7M in revenue (+25% y/y) – the accounting here for revenue recognition is a little weird because of ASC 606.

- AYX ended the quarter with 7,000 customers across 90 countries, including 38% of the Global 2000.

- Net dollar retention was 124%, and 135% among the Global 2000.

- Strong balance sheet with over $1B in cash and cash equivalents.

- AYX analyst day scheduled for Spring 2021.

- In Q3, the FAA expanded its footprint with the Alteryx platform in order to automate and speed up the critical transfer of data between existing systems. Alteryx allowed them to eliminate manual processes and automate their workflows during the pandemic.

- While the overall duration remained at ~2 years in the quarter, AYX did see a slight tick down on a year-over-year basis. Management expects this trend to continue in Q4. However, they noted that the product mix in the quarter was favorable at the higher end of the upfront range.

Takeaways:

- Digital transformation initiatives within the largest companies in the world accelerate, so does Alteryx's relevance. In Q3, a number of Global 2000 companies expanded their use of Alteryx across multiple lines of business. However, net customer adds was the lowest in the last 3 years (last quarter with fewer net customer adds was Q3 2017). As management hinted, it seems like growth is mainly coming from the larger customers expanding use cases, whereas other customers are shortening their subscriptions as evidenced by them disclosing a higher net dollar retention among the Global 2k customers (135% vs. actual 124%). However, even this isn't very impressive. Remaining Performance Obligation (RPO) has been flat the past 4 quarters, and management noted the company was allocating resources specifically to get big customers just to renew with Alteryx.

- Customer spending trends improved modestly relative to Q2. Again, management hinted at uncertainty and skepticism over short-term growth: higher level of scrutiny on spend, which has led to longer sales cycles, smaller deal sizes, and less favorable linearity relative to historical levels. Renewals, particularly in enterprise segment remains strong, as they continue to see elevated churn levels among smaller customers and those with small Alteryx deployments. On the bright side, management noted that churn rates improved slightly from what they saw in the first half of 2020. Approximately 35% to 40% of TCV booked in the quarter will be recognized upfront with the remainder recognized ratably over the time of the contract. Therefore, revenue growth rates will likely slow in 2021 as a result of shortened contract duration and other accounting inputs.

- AYX looks deceptively cheap. Growth is primarily coming from large enterprise customers, and new CEO Mark Anderson's background caters more towards them. With competition among no-code vendors intensifying and AYX is struggling to hold onto its smaller customers, they may well carve out a niche among larger enterprises as their solution delivers strong value to its customers and they've shown the ability to successfully land and expand. While AYX may look cheap on an EV/NTM revenue basis for a profitable company growing ARR at 38%, their margins likely lack sustainability in the short term and their long-term FCF margin target is likely lower than best-in-class B2B SaaS (30-35+%). While the FCF margin improvement over Q2 may seem like a positive, it was the same year-over-year and in this COVID-19 environment, investors are more likely to reward top-line growth than cost-cutting.

Bottom line: AYX continues to be a company I've maintained a small position in, but still a tier 2 B2B SaaS company – and I'm beginning to wonder whether it even belongs among that group.

How Alteryx stacks up versus other high growth B2B SaaS:

4️⃣ Product Update - Size Label & Company Highlight 🚨

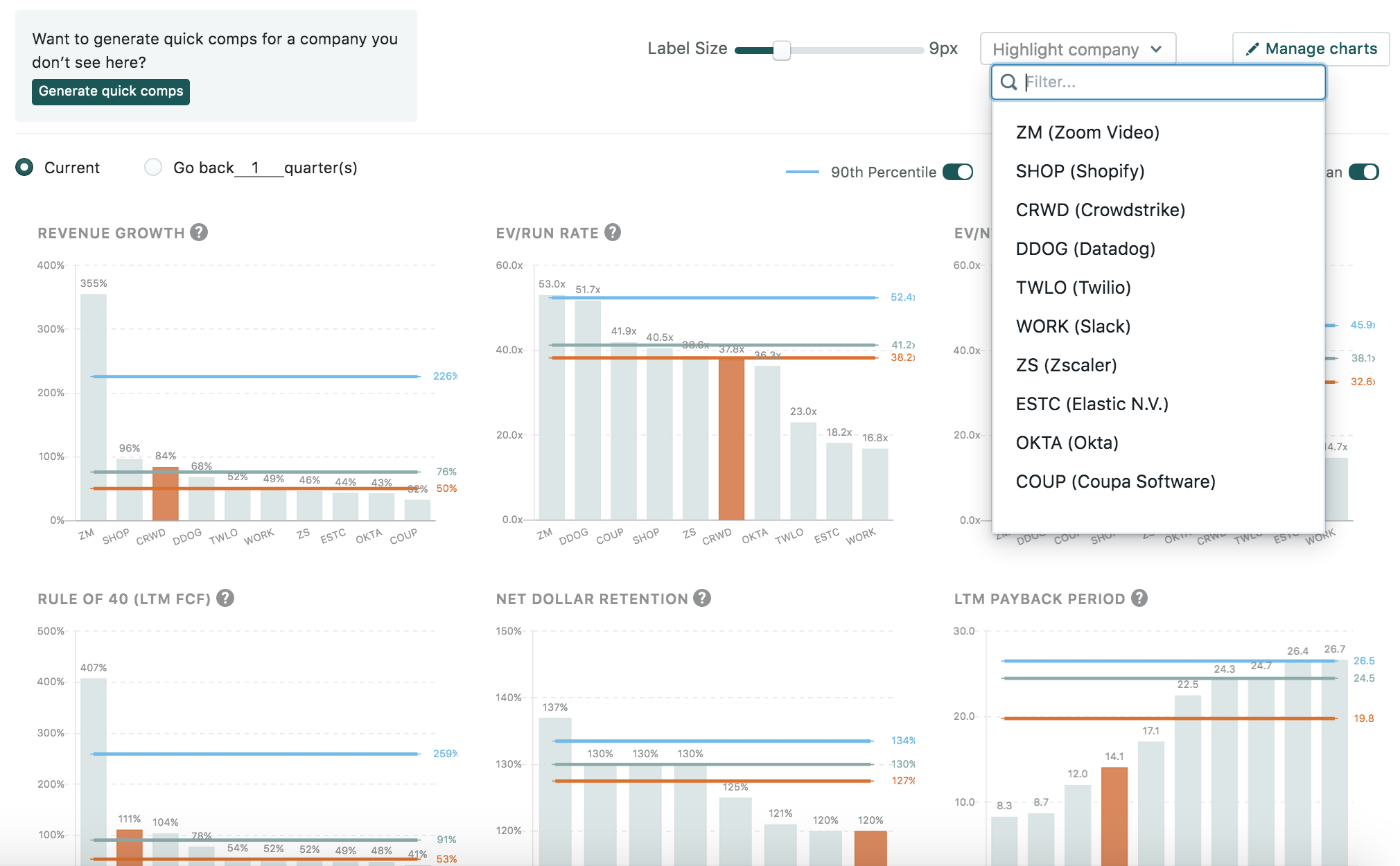

Highlighting two new features on our dashboard: Label Size & Company Highlight!

Label Size: users can now adjust the size of the labels in the graphs.

Company Highlight: users can now select the company they want to highlight through a drop down menu rather than clicking on the respective bar in the graph.

Stay safe everyone,

Albert Wang, Public Comps Team

albert@publiccomps.com

Like these weekly dashboards? These are for Publiccomps.com customers only but you can have your friends subscribe to the newsletter here where we send out investment memos, market maps and analysis on the broader SaaS market.

Views expressed in theses emails are ours and ours alone and don't represent that of our previous or current employers. Public Comps provides financial and industry information regarding public software companies as part of our weekly dashboard, our blog, and emails. Such information is for general informational purposes only and should not be construed as investment advice or other professional advice.

Full disclosure: I own CRWD, TWLO, SHOP, LVGO, FB, MSFT, DDOG, ESTC, AYX, SMAR, PLAN, ZM and BILL.