Zoom IPO & S-1 Teardown

Here are 5 reasons why Zoom.us is one of the top SaaS companies .

Here are 5 reasons why Zoom.us is one of the top SaaS companies 🏆

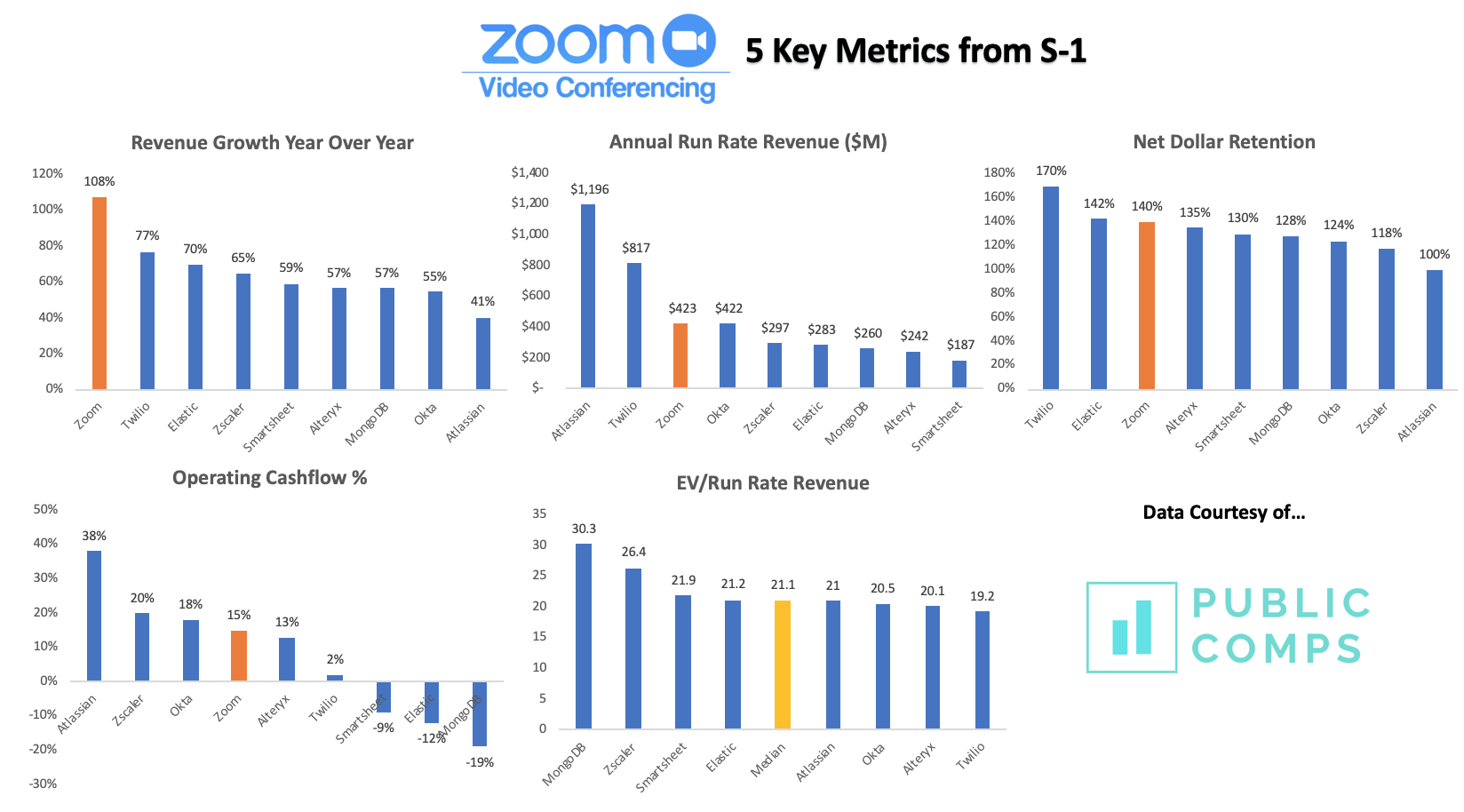

1/ 🔥 Zoom is #1 Fastest Growing Public SaaS Company at 108% YoY revenue growth. Benchmarking against Twilio, Alteryx, Zscaler, Okta, Smartsheet, Atlassian which are all top quartile growth and high-quality SaaS cos.

2/ 🚀 Growing fast at the #3 largest revenue scale ($423m ARR) of our top SaaS companies. There's room to grow too: WebEx was $700m of revenue when Eric left Cisco in 2011 and the enterprise video conferencing market is large ($20b in 2018 growing 20% YoY)

3/ 🙌 Best in class net dollar retention at 140% which is #3 among our top SaaS companies. The beauty of a product that customers love (70 NPS) where non-paying attendees -> attend Zoom meeting 😍 -> become paid host 💳> more attendees -> paid host 🌀

4/ 💵While generating 15% operating cash flow % ($51m operating cash flow '19) which is #4 highest operating cash flow %. Due to efficient S&M (10 month payback period) + self-service bottoms up model + 74% ARR in '19 is upfront annual/multiyear contracts

5/ 💰The Median EV/Run Rate Revenue is ~21.1x and at $423m ARR would imply ~$9B market cap. 9x for Sequoia since the Series D (2 years ago) which is ~200% IRR and ~$800m+ cap gains.💰