Block $SQ Outlook

A quick note on Block's valuation and future outlook heading into earnings next week!

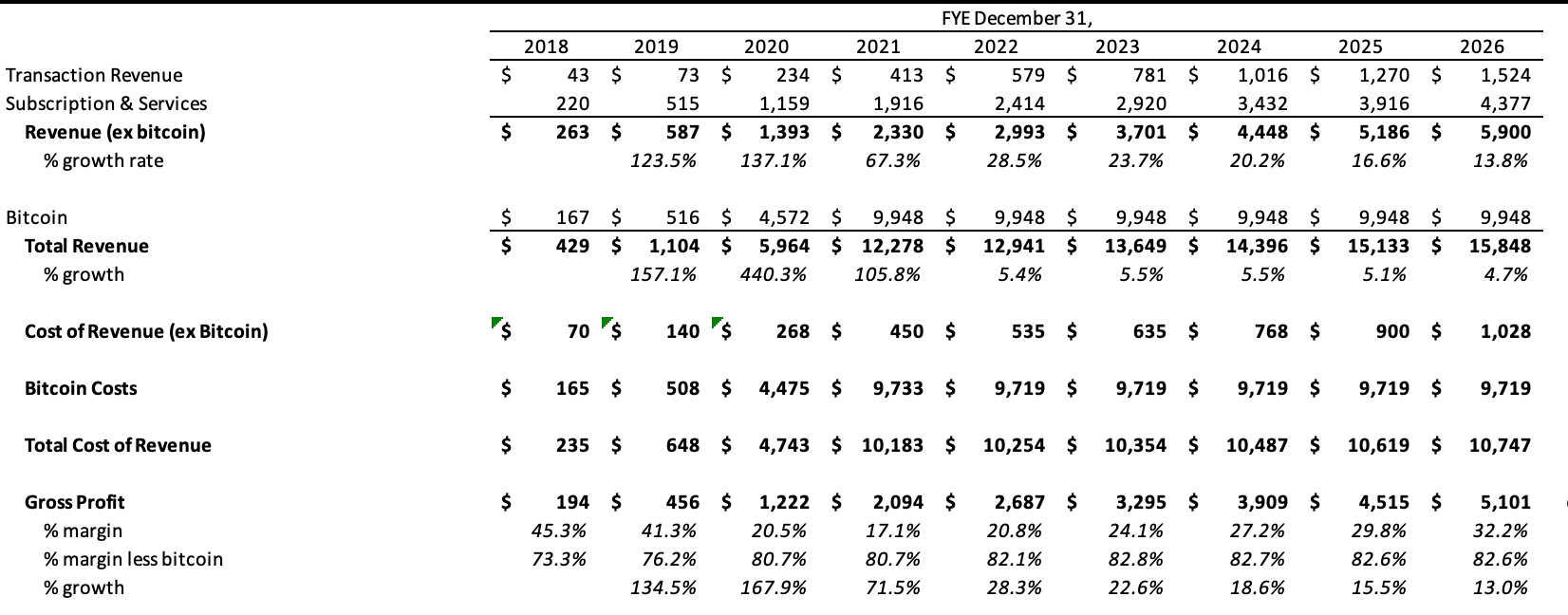

Hey Public Compers, this week we are outlining a brief thesis for Block before Q4 '21 earnings next week! If you guys are interested in seeing a detailed model/valuation work breaking out transaction revenue, subscription, and services revenue for both Seller and CashApp segments, please email me at aneesh@publiccomps.com or DM me on Twitter. Also, I'll be updating this post if something materially changes post-earnings.

Summary

Block is a best-in-class business currently trading at a meaningful discount to its fundamental value (8.5x forward gross profit), presenting an extremely attractive risk-reward profile. At its current price, the value of the core Seller and CashApp ecosystems alone provide very strong valuation support, while Afterpay integration/synergies, Bitcoin real option, and other vectors for growth create a compelling case for the stock to 3x from here in the next several years. If you already know the business well, feel free to skip to the valuation section.

Company Overview

Block operates at the intersection of software, payments, and banking creating a financial ecosystem that incorporates both sellers and consumers. Historically, the company has had two predominant revenue streams: Seller and Cash App.

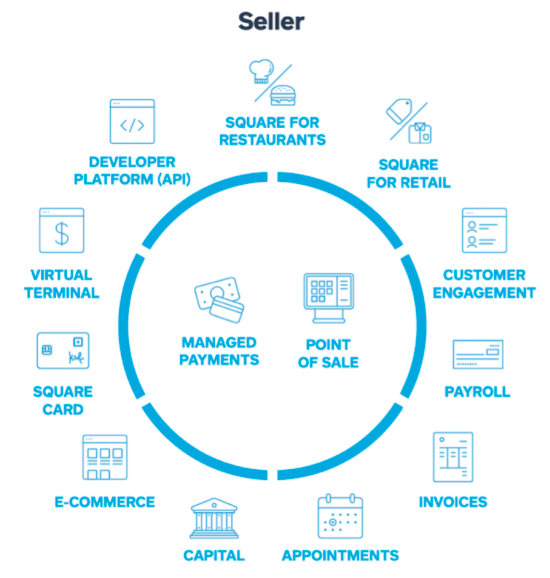

Seller (~72% of adjusted revenue FY'20): Block’s seller ecosystem comprises a suite of B2C-focused hardware, software, and financial products. Total Seller GPV (Gross Processing Volume) I estimate to come in at around $152B for FY'21.

- Hardware: Square credit/debit card readers, tablet-based payment terminals, and POS systems provide sellers with a sleek and easy-to-use interface to accept non-cash payment, all at very attractive price points.

- Software: Square capitalizes on the sellers brought into the ecosystem via hardware by offering a comprehensive suite of SaaS solutions to help sellers manage their business - from customer-facing appointment booking software to payment APIs that enable e-commerce.

- Financial Services: Among other financial service offerings, Square offers a prepaid debit card tied to the seller’s business account (Square Card) and disburses easily-accessible loans to sellers by using their business revenue to automatically pay-back the loan (Square Capital).

Seller Ecosystem Overview & Pricing: Block monetizes Sellers by taking a take rate on their GPV as well as providing value add subscription and services offerings like Instant Deposit, Square Card, Square Capital, Square Online Store, and Software (Weebly Platform).

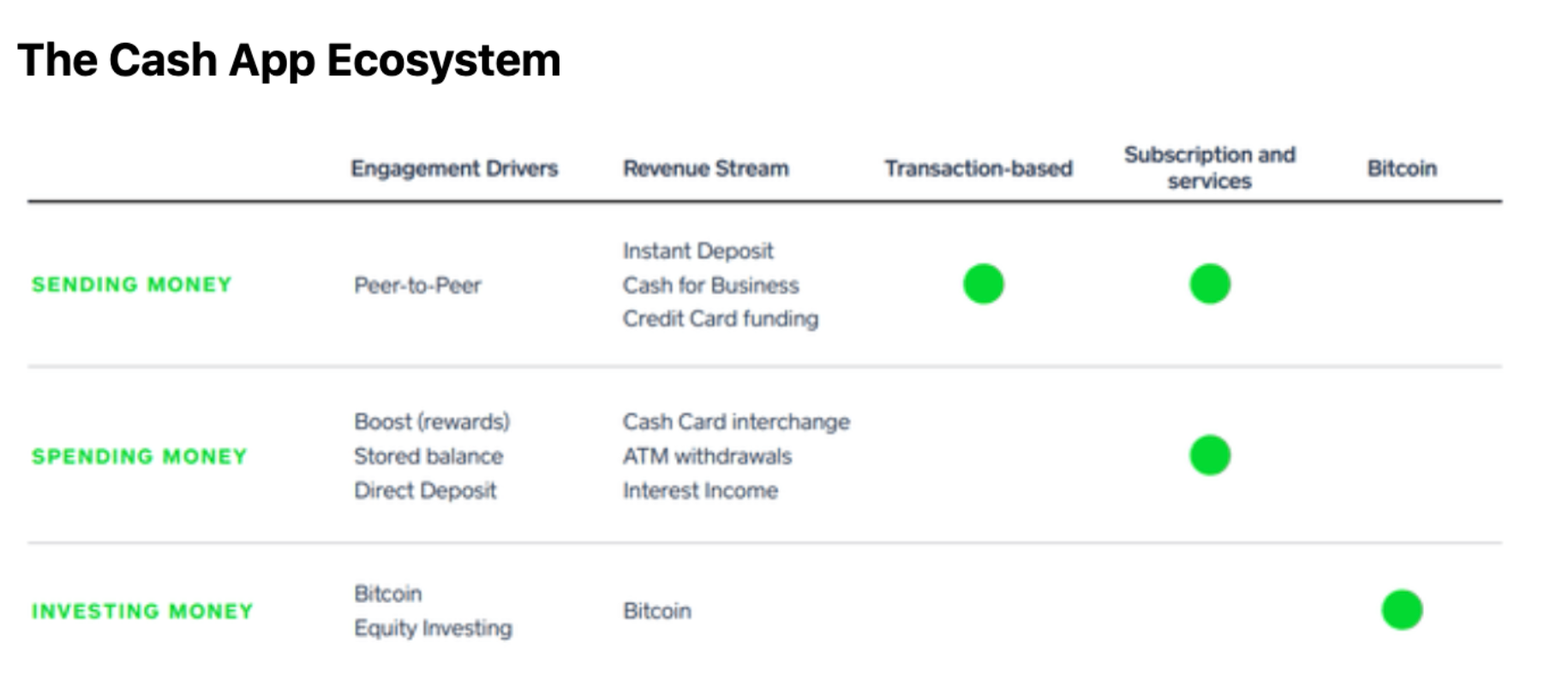

Cash App (~28% of adjusted revenue FY'20): An ecosystem that provides financial tools for individuals to store, send, receive, spend, and invest money. Management has noted the importance of keeping as much money in the Cash App ecosystem as possible and has methodically released features that keep users consistently engaged.

- Though Cash App began primarily as a Peer-to-Peer (P2P) payment service, the addition of several product offerings has created a neobanking-like ecosystem. These product offerings include the ability to receive direct deposits, stock trading, bitcoin trading and transacting, cross-border payments, and debit cards.

- Fees are generated from Consumer-to-Business (C2B) payments using CashApp or the Cash Card (2.6% +10¢ per transaction), expedited bank account transfers (1.5% instant deposit transaction fee), credit card fees, and BTC transactions (up to ~1.75%)

- Depending on the level of cryptocurrency volatility, BTC contributes anywhere from 50-80% of all Cash App revenue.

- Cash App has ~40 million Monthly Active users (MAU), with an Average Revenue per User (ARPU) of ~$50. Out of these ~40M MAU's around 27% of them are Cash Card users and 5% are direct deposit users.

Afterpay: Block completed the acquisition of Afterpay on January 31, 2022, adding a best-in-class buy-now-pay-later (BNPL) offering and demand aggregator to its ecosystem which will effectively facilitate cross-selling while further promoting a closed-loop payment ecosystem. I briefly talked about this acquisition last August, you can find my original take here.

- APT chargers merchants 3-6% of the purchase price which is higher than typical 3-4% credit card fees. However, management indicates that merchants through partnering with Afterpay see an average order value (AOV) increase of >25% with >20% jump in conversion and frequency. The real value proposition of Afterpay is its marketplace that aggregates demand for merchants rather than its BNPL product that is becoming increasingly commoditized.

- Afterpay is the BNPL leader in the US and Australia with a strong presence as Clearpay in the UK as well. Given that Cash App is only available in the US and the UK, Afterpay being the dominant BNPL player will lead to some powerful synergies.

Industry Overview

Seller:

- SMBs contribute >50% of transaction revenue for payment processors since they pay 20-30x higher fees than large businesses. This is particularly relevant given Square’s focus on SMBs, as sustained market dominance among SMBs will create much more value than attempting to target sellers with greater Gross Payment Volume (GPV).

- Block’s US Seller-ecosystem TAM is ~$85B: $39B transaction profit + $30B Software + $12B Square Capital + $5B Financial Services. TAM grows beyond $100B considering international opportunities and other growth vectors.

- The seller ecosystem is driven by industry tailwinds including the digitization of transactions, cross-selling capabilities for customers with both online and physical distribution channels, and an increasing desire for an all-encompassing commerce ecosystem among merchants.

Cash App:

- P2P payments are growing rapidly, with high-teens user growth across P2P applications and GPV projected to grow at a CAGR of 17-19% until 2030.

- $SQ management estimates Cash App’s user TAM in the US to be roughly 1/3 of the population, comprising ~70-80mm+ underbanked consumers and ~40-50mm+ digitally native consumers (Millennials and Gen Z). This implies ~15% penetration based on Cash App’s 15mm users - not accounting for potential TAM expansion as additional banking services are added.

- The consumer-finance industry is driven by tailwinds toward neobanking, P2P payments, and interconnected services - among other drivers. Similar to the seller-ecosystem, companies that can provide a one-stop shop for payments, banking, credit (e.g., BNPL), and investment will have a material edge.

Outlook

1. Afterpay acquisition, Cash App Pay, and Bitcoin payment strategy offer alternative payment rails to card networks (creating a closed-loop payment system) which will drive gross profit expansion while potentially boosting merchant economics over time.

- Currently, Block receives less than 1% of the GPV from merchants as the majority of fees are redistributed to participants such as the acquiring bank and the card network. With BNPL via Afterpay integration and CashApp Pay in the near-term and Bitcoin payments in the long term, Block’s take rate on GPV will increase as fees will not have to be redistributed to various participants in the payment value chain. Payments will flow through a closed-loop system where Block is able to pocket all merchant fees or even lower merchant fees to incentivize payment through Block-provided alternative payment rails. This demonstrates the real value of owning both the merchant and consumer relationship.

- Currently, 90% of Afterpay loans are paid back via debit cards which further represents an opportunity for gross profit expansion as loans can be paid via Cash App or users connected bank account in Cash App.

2. Block’s Bitcoin strategy/maximalism is misunderstood

- Over the last several years, Block's Bitcoin strategy has been centered around user engagement on Cash App. Users graduate from “spending money” to “saving money” as they invest in stocks or bitcoin and, in Block’s 4Q20 earnings call, Dorsey stated “In 2020, more than 3 million customers bought or sold Bitcoin in Cash App. And in January 2021 alone, more than 1 million customers bought Bitcoin for the first time.”

- Features such as being able to hold Bitcoin assets within Cash App, Bitcoin boosts (an incentive to spend money at select retail locations and receive Bitcoin rewards), Lighting Network (allowing Cash app customers in the U.S. to send bitcoin for free within seconds to anybody in the world), and other initiatives further increase the important TPV KPI within Cash App.

- Over time, Cash App will become users' crypto gateway that connects to other initiatives like the hardware wallet, tbDEX, and other decentralized products. Last June, Dorsey confirmed the development of a hardware wallet focused around Bitcoin, global distribution, multi-signature authentication, and mobile use.

- While Dorsey does seem obsessed with making Bitcoin the internet's "digital currency", Block continues to make useful crypto products that increase Cash App engagement and customer lifetime value.

Current Valuation

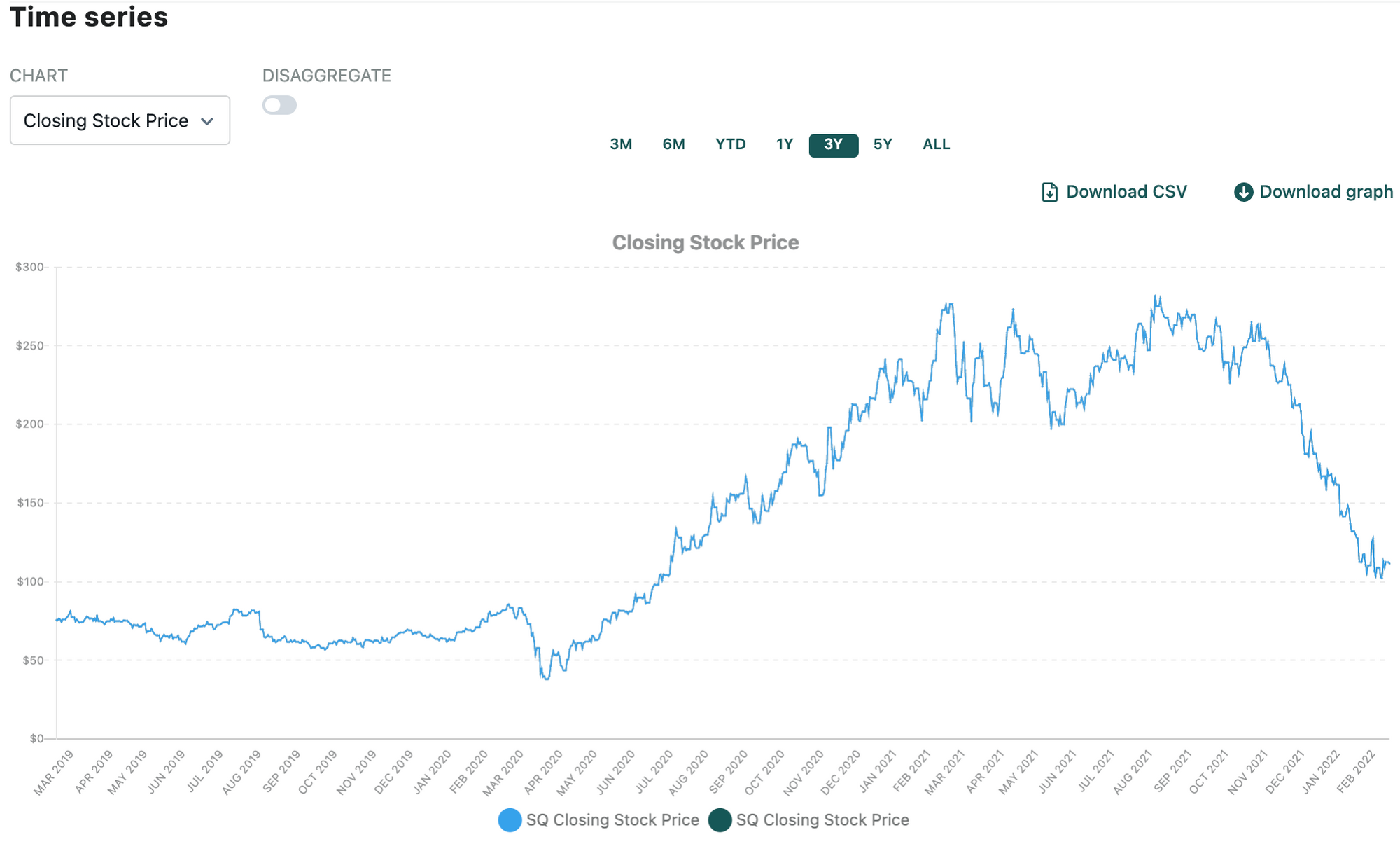

Block has been one of the hardest-hit growth stocks since the broader market selloff beginning in November of last year. At the current closing price, $SQ hasn't traded at this level since July of 2020 as multiples have contracted significantly across the payments and software landscape.

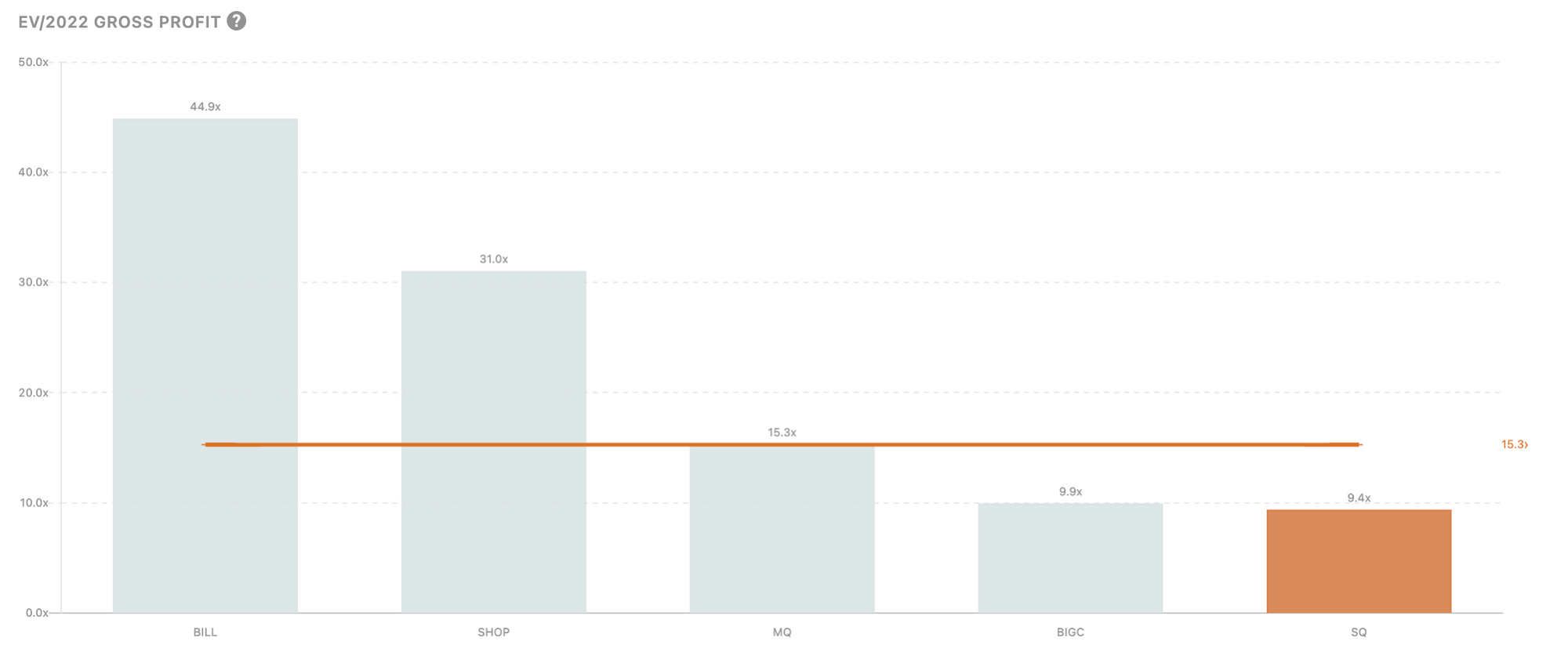

Current price attributes minimal value to Afterpay acquisition as Seller and Cash App ecosystems present a compelling opportunity themselves.

Block's current equity value is ~$66B which suggests that Block's core Seller and Cash App ecosystem without Afterpay synergies and gross profit account for 90%+ of equity value depending on multiples attached to each ecosystem. Even if you attach lower multiples on both Seller and Cash App, Block's equity value attributes minimal value to Afterpay, a business growing at a significantly quicker clip while also reaccelerating aspects of both the Seller and Cash App businesses.

Many investors are waiting on the Cash App print upon earnings as there is widespread fear that Cash App growth will go negative in 2022. Given the price action over the last several months, the expectation of negative growth is partially built-in, especially when considering the massive Cash App demand-pull forward from direct despite stimulus throughout the pandemic. However, I wouldn't rule out a broad sell-off if Cash App MAUs decrease substantially.

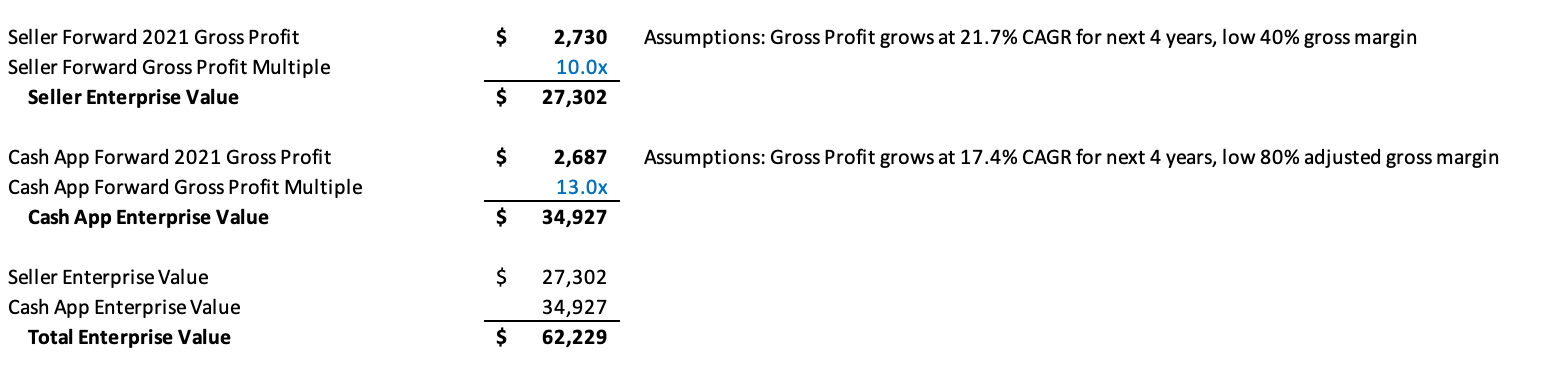

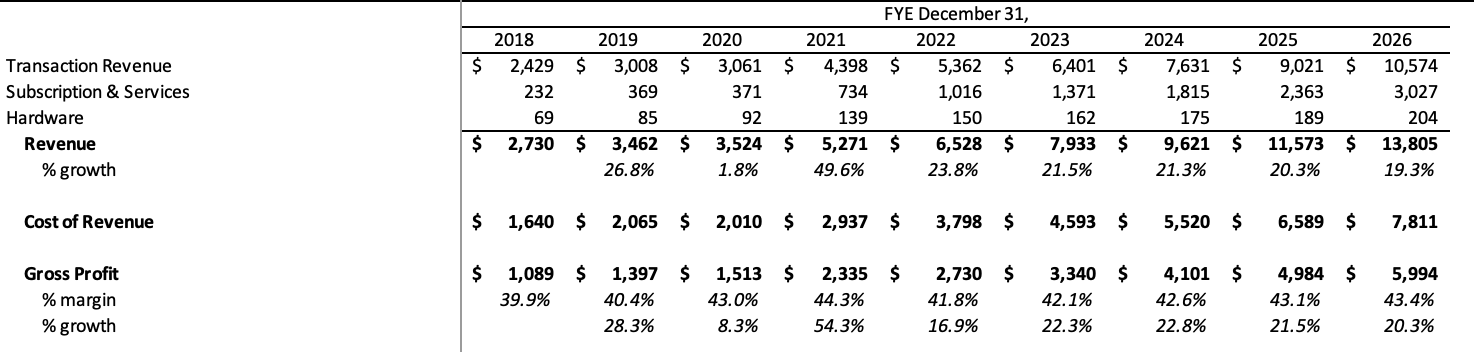

My current 2025 EOY PT is $264 with a 13x gross multiple on a ~$14,000B forward gross profit base. What is particularly compelling is the strong valuation support provided by Seller and Cash App with the bear case providing little downside at the current price. Holistically, I believe Block offers one of the best risk-reward ratios given the quality of the underlying business and the potentially lucrative economics of a closed-loop payment system.

That's it for this week, hope you enjoyed it, and please let me know whether you would invest in Block at this price. As always, don’t hesitate to shoot over a message with any feedback or want to look at my full model. Would love to chat with people with differing opinions on $SQ!

Cheers,

Aneesh Tekulapally (@aneesh_tek on Twitter)