Public Comps Weekly Dashboard 8/7/2020: Fastly Q2 Earnings and how Datadog disrupted observabiility

We break down FSLY's Q2 Earnings

👋 Public Comps Customers 👋

Hey everyone, we're moving the email newsletter back to the Public Comps blog!

In this newsletter, I benchmark SaaS against public indices, take a quick look at median B2B SaaS valuations, teardown Fastly's Q2 '20 earnings, and dive into how Datadog disrupted the observability space!

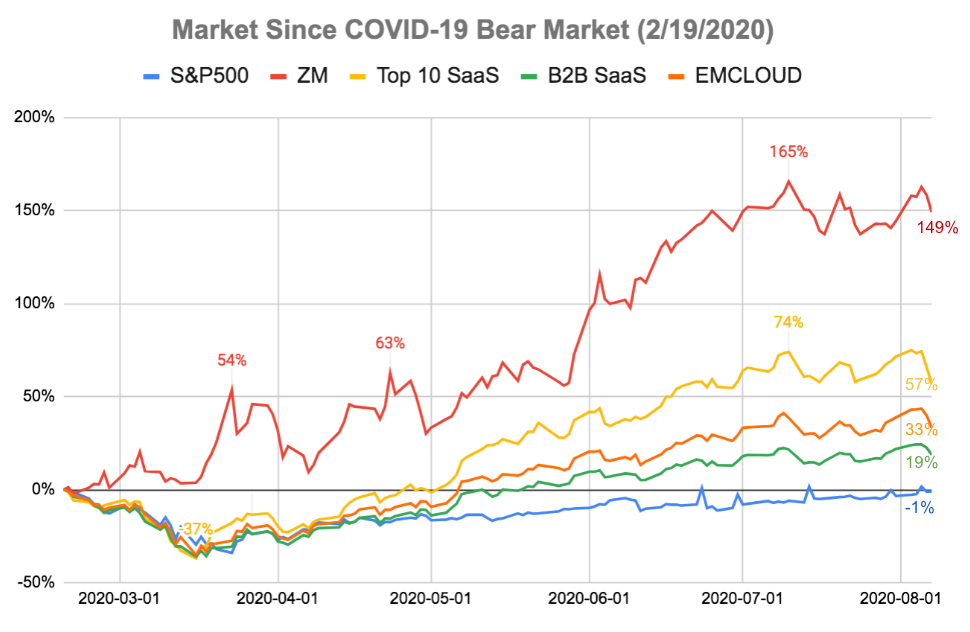

1️⃣ SaaS Stock Prices vs. Benchmarks 📊

Friday marked 169 days since the start of the bear market on February 19th. The S&P 500 index is only down -1% after a good week of recovery.

Change since bear market start (2/19/2020):

- S&P 500: -1.0%

- B2B SaaS: +18.7%

- Top 10 SaaS: +56.7%

- Bessemer Cloud Index (EMCLOUD): +33.2%

- ZM: +148.9%

Change in the past week:

- S&P 500: +2.4%

- B2B SaaS: -14.7%

- Top 10 SaaS: -3.1%

- Bessemer Cloud Index (EMCLOUD): -5.6%

- ZM: +4.6%

This week brought a lot of high valuation B2B SaaS back to reality. Going into earnings season, expectations were incredibly high, as B2B SaaS valuations; specifically high growth, had appreciated over 30% since their last earnings. We saw the disparity between buy-side and sell-side consensus revenue estimates as most cloud names substantially beat sell-side targets, but still saw their valuations decline. Notably, Shopify's 97% yoy revenue growth in Q2 beat sell-side estimates by 38%, yet their stock price remained fairly flat. These high, priced-to-perfection expectations leave little room for error as we saw in post-earnings reaction. Despite corrections among high growth cloud names, the broader market saw strong improvement this week, as Friday's surprise job report of 10.2% unemployment (estimated 11.1%) and strong signal of manufacturing improvement, boosted the industrials sector.

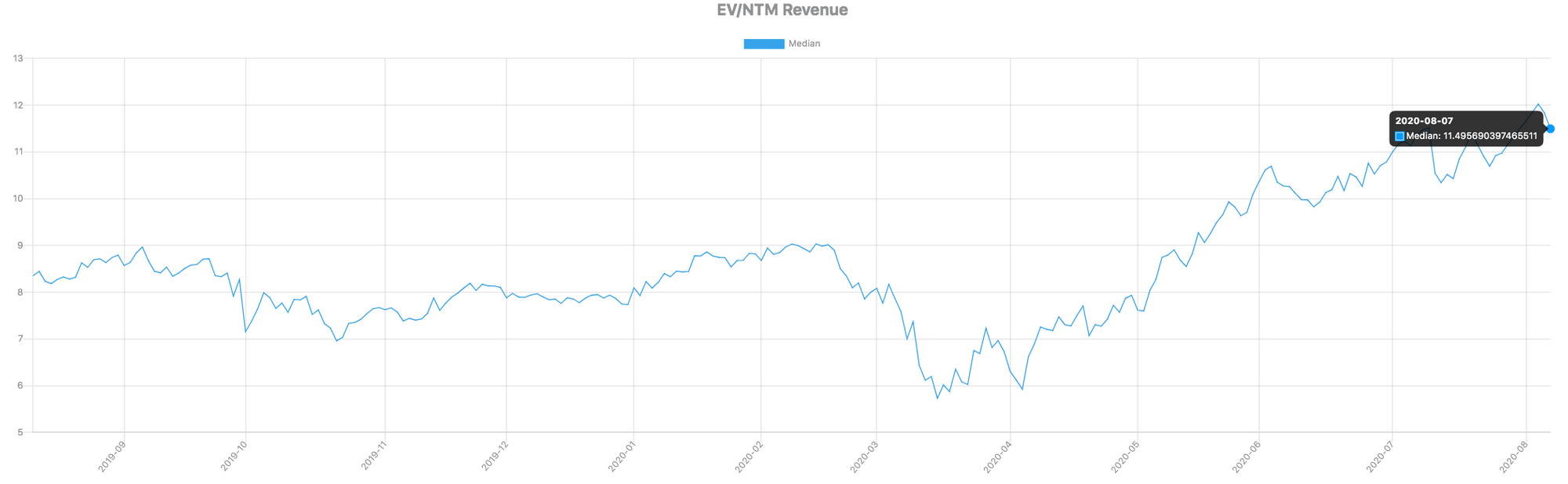

2️⃣ Median B2B SaaS Valuation Multiples: 11.5x 🔥

Median B2B SaaS valuations fell -4.2% this week (from 12x to 11.5x), but high growth names were hit the hardest – as median high growth SaaS multiples fell -14% (from 18.8x to 16.2x).

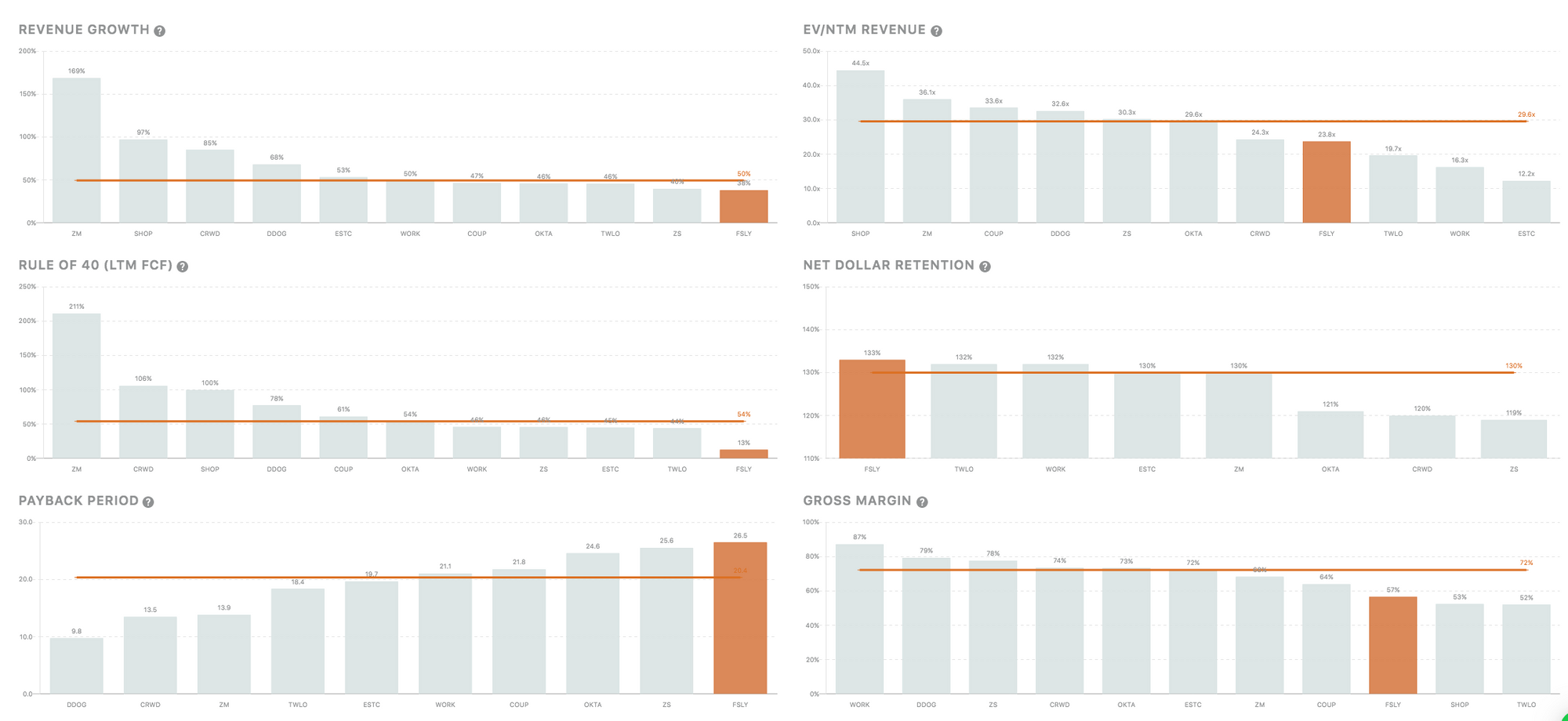

3️⃣ SaaS Earnings - Fastly (FSLY) 💸

Fastly Q2 Earnings | Earnings Call Transcript | Shareholder Letter

Highlights:

- Summary: Fastly is a leading edge cloud platform, providing a content delivery network (CDN), Internet security services, load balancing, and video and streaming services. With highly customizable CDN solutions, Fastly enables developers to take full control of edge logic, computations, and advanced routing. As the Internet of Things (IoT) continues to expand at astonishing levels, the current centralized computing Internet infrastructure will inevitably be plagued with traffic and latency issues, driving the adoption of the edge cloud. Fastly’s beta version of a promising serverless edge computing will give rise to an increasingly dynamic and more-personalized Internet experience. With a mission-critical service seeing heightened demand, as well as innovative product launches, Fastly's maintained low churn and continued accelerated growth which have propelled it to succeed in this market.

- Why Fastly is accelerating: Fastly has a usage-based pricing model where revenue grows as customers increase their usage of the product. They charge $0.12 per GB (bandwidth) and $0.0075 per 10,000 requests with automated tiered discounts with increased usage. This showcases their "land and expand" strategy, which is reflected in their strong dollar-based net expansion rate. As COVID-19 helped remove many barriers to cloud adoption and increased internet traffic, Fastly has been a strong beneficiary and customers have seen a strong uptick in their CDN usage.

Fastly $FSLY Q2 earnings🔥

— Public Comps (@publiccomps) August 5, 2020

Revenue ACCELERATED to 62% yoy growth.

Dollar based net expansion increased to 137% (133% in Q1)

ACV of $716k, up from $642k in Q1

non-GAAP gross margin increased to 61.7%, up from 55.6% a year ago.

First Q of positive EBITDA

Raised FY20 guidance!

Key insights from the earnings call:

- Customer growth was strong: Management noted a solid increase in total customers (1837 to 1951), the largest quarterly increase since going public but only added 7 enterprise customers (297 to 304).

- TikTok accounted for 12% of revenue: Fastly noted that "any ban of the TikTok app by the U.S. would create uncertainty around our ability to support [them]".

- Upsell is going well: average enterprise customer spend increased to 716k, from 642k in Q1, and net retention rate increased to 138% from 130% in Q1.

- Q2 to Q1 is usually flat, and we should be optimistic about Q3: management noted that seasonally, Q1 to Q2 comparisons are usually flat (which makes the revenue acceleration from 38% to 62% all the more impressive), and a big ramp up usually comes from Q2 to Q3.

- Remote learning, especially as the fall semester begins is an exciting sector of focus: "Universities face digital — the need to accelerate digital transformation by years like everyone else does in order to survive."

High-level thesis on Fastly:

- Edge networks like CDNs are on the early half of the S-curve and demand is accelerating. Fastly has a huge market opportunity in a large and growing TAM with high barriers to entry. Increasing number IoT devices, web-based video content, 5G networks, and autonomous vehicles are all early-adoption tailwinds that Fastly can immensely benefit from.

- Developer-focus and "land and expand" strategies prove successful compared to competition. The flexibility of Fastly's product, as developers increasingly become the decision-makers within companies helps Fastly land new deals, and their sticky existing products continue to drive increased usage as seen with their best-in-class net dollar retention.

- Fastly is a mission-critical product and one of the largest beneficiaries of COVID-19. COVID-19 itself removed many barriers to adoption for edge computing in IT, increased internet consumption, and set the standard of maintaining healthy internet infrastructure. This itself is a de-risking event which propels Fastly to continue to trade at a premium valuation.

- Outlook: Fastly was a breakout stock in 2020 as COVID-19 helped accelerate demand for CDNs. Fastly is seeing increased adoption for their real-time visibility, a characteristic lacking of many legacy CDN vendors, however, their security offerings don't stack up well with competitors like Cloudflare and large cloud infrastructure providers (AWS, Azure, GCP), an area they'll look to boost.

4️⃣ How Datadog disrupted Observability 👀

tl;dr check out Jon Ma's Datadog S-1 teardown!

I analyze how Datadog was able to beat out their competitor, and previous category leader, New Relic, in the observability space.

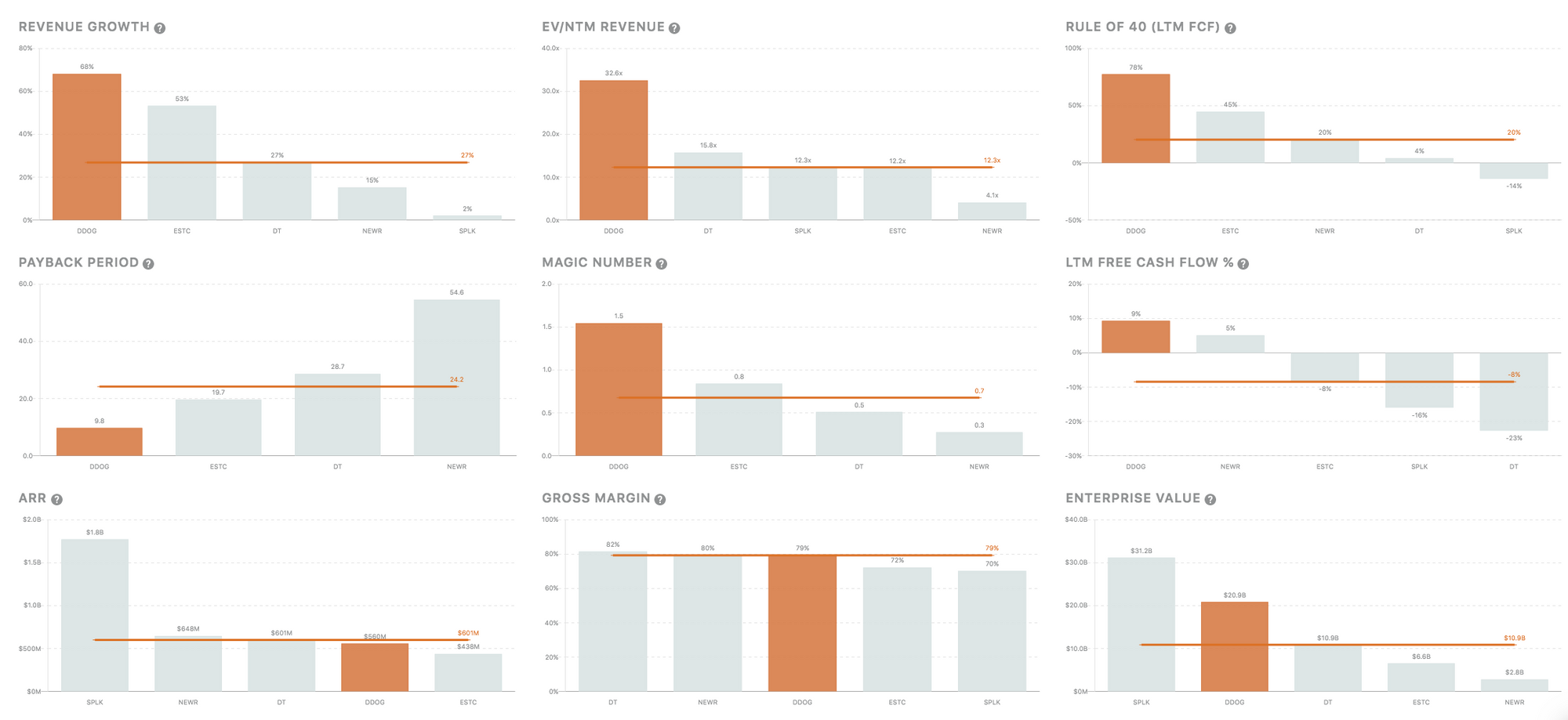

Founded in 2010, Datadog is now a $22.5B company growing 68% yoy and up 105% YTD – one of the hottest cloud names today.

Meanwhile, New Relic, founded two years earlier in 2008, is now just a $3.2B company, growing 15% yoy, and down 22% YTD. The once premium cloud name has fallen out-of-favor amongst most software investors.

Datadog is valued 7x more than New Relic, despite the fact that New Relic actually has a higher ARR!

New Relic went public in late 2014, at the time, it was considered one of the hottest cloud software companies, growing revenues 100+% yoy and having raised funding from Insight Partners, Benchmark, and Dragoneer. New Relic didn't even mention Datadog as a competitor in their S-1. Ultimately, rampant growth deceleration as a result of ineffective sales execution and inability to maintain or grow customer cohorts with decreasing net dollar retention led to New Relic's decline.

Here I highlight two of Datadog's key superpowers that have allowed them to scale so quickly:

- Datadog's focus on having the whole breadth of product offerings to capitalize off "land and expand":

- Datadog recognized that one of the pain-points of customers is having multiple software vendors. Companies wanted to trim down the number of monitoring tools used, which in the case of larger enterprises was often more than 30, while some smaller organizations still had 3-10 different monitoring tools. To solve this, Datadog quickly rolled out additional product features, expanding into the APM and log space.

- In their own view, they believed they had a larger market opportunity than the one that New Relic claimed. In fact, New Relic claimed that their TAM in 2018 would be approximately $19B, whereas in their S-1 in 2019, Datadog claimed a TAM of over $60B.

- Datadog’s goal was for their customers to have many end users of their products and services. In their S-1, they mentioned how a leading communications software technology provider had almost 800 Datadog users, about half of the company’s total employee count and greater than the total number of the company’s engineers. Another company, a Fortune 500 financial services firm, had over 3,000 Datadog users.

- Frictionless, self-serve product adoption and cross-sell enabled Datadog to more effectively penetrate TAM and expand faster than competitors. Relentless focus and great execution on creating products helped create scale. Unlike legacy solutions, which were typically used only by IT professionals, Datadog encompassed the whole breadth of product offerings and thus, could be deployed across a customers’ entire infrastructure environment (including public cloud, private cloud, on-premise, and multi-cloud hybrid).

- Datadog was able to disrupt the industry because its customers are offered a single choke-point of performance in one solution and could now consolidate all their observability needs onto a single platform.

2. Being customer-obsessed: understanding customer pain-points and then building positive feedback loops.

- Datadog was "born from a problem experienced first hand" by the founders, Olivier Pomel and Alexis Le-Quoc. They understood and solved the friction experienced by developers in monitoring cloud applications.

- With Datadog's ability to make the end-user almost anyone in an organization, they can now land almost anywhere and expand from there, this boosts their ability to continuously upsell and cross-sell their customers. Its a win-win because Datadog has products that are easy to adopt and gain value from, which allows customers to then prioritize spend in new product innovation.

- With Datadog's insane flexibility, their go-to-market strategy isn't directly selling to CIOs, they can then segment their S&M team into four key areas for greater efficiency: 1) enterprise sales team focused on large business 2) high-velocity inside-sales team focused on new customers 3) a customer success team focused on customer onboarding and expansions in the current base and 4) a partner team that works with resellers, distributors and managed service providers.

All of this is clear with a quick look at how Datadog stacks up against its competitors in the observability space: sales are more efficient with a better magic number and lower payback period, and its able to efficiently execute.

As always, feel free to shoot me an email if you have any questions, feedback, or concerns.

Stay safe everyone,

Albert Wang, Public Comps Team

albert@publiccomps.com

Like these weekly dashboards? These are for Publiccomps.com customers only but you can have your friends subscribe to the newsletter here where we send out investment memos, market maps and analysis on the broader SaaS market.

Views expressed in theses emails are ours and ours alone and don't represent that of our previous or current employers. Public Comps provides financial and industry information regarding public software companies as part of our weekly dashboard, our blog, and emails. Such information is for general informational purposes only and should not be construed as investment advice or other professional advice.

Full disclosure: I own CRWD, TWLO, SHOP, LVGO, FB, MSFT, DDOG, ESTC, AYX, SMAR, PLAN, and ZM.