Public Comps Weekly Dashboard 9/11/2020: BIGC Earnings & Asana teardown

We break down BIGC's Q2FY21 Earnings

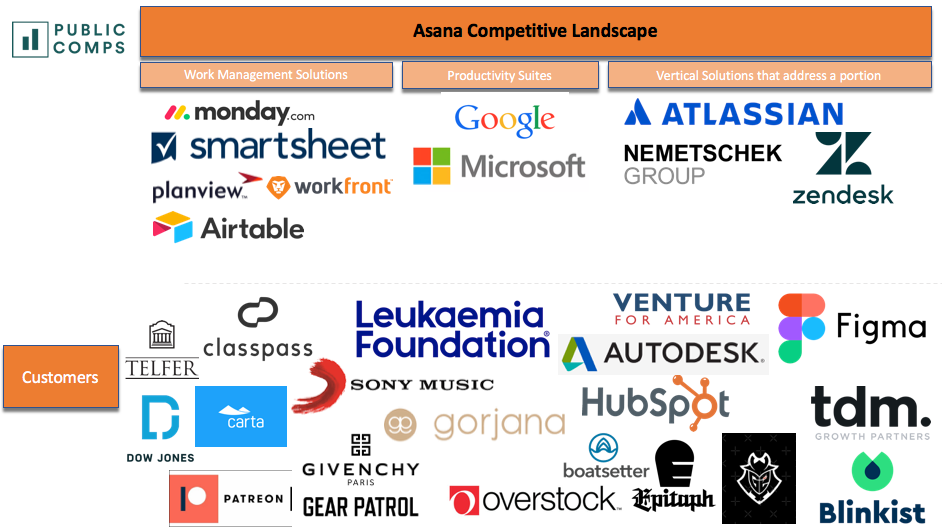

👋 Public Comps Customers 👋

tl;dr This week's newsletter covers BigCommerce's first public earnings quarter, in which I breakdown the earnings call & lay out a high-level investment thesis on the company and showcase a few insights from Asana's S-1 teardown!

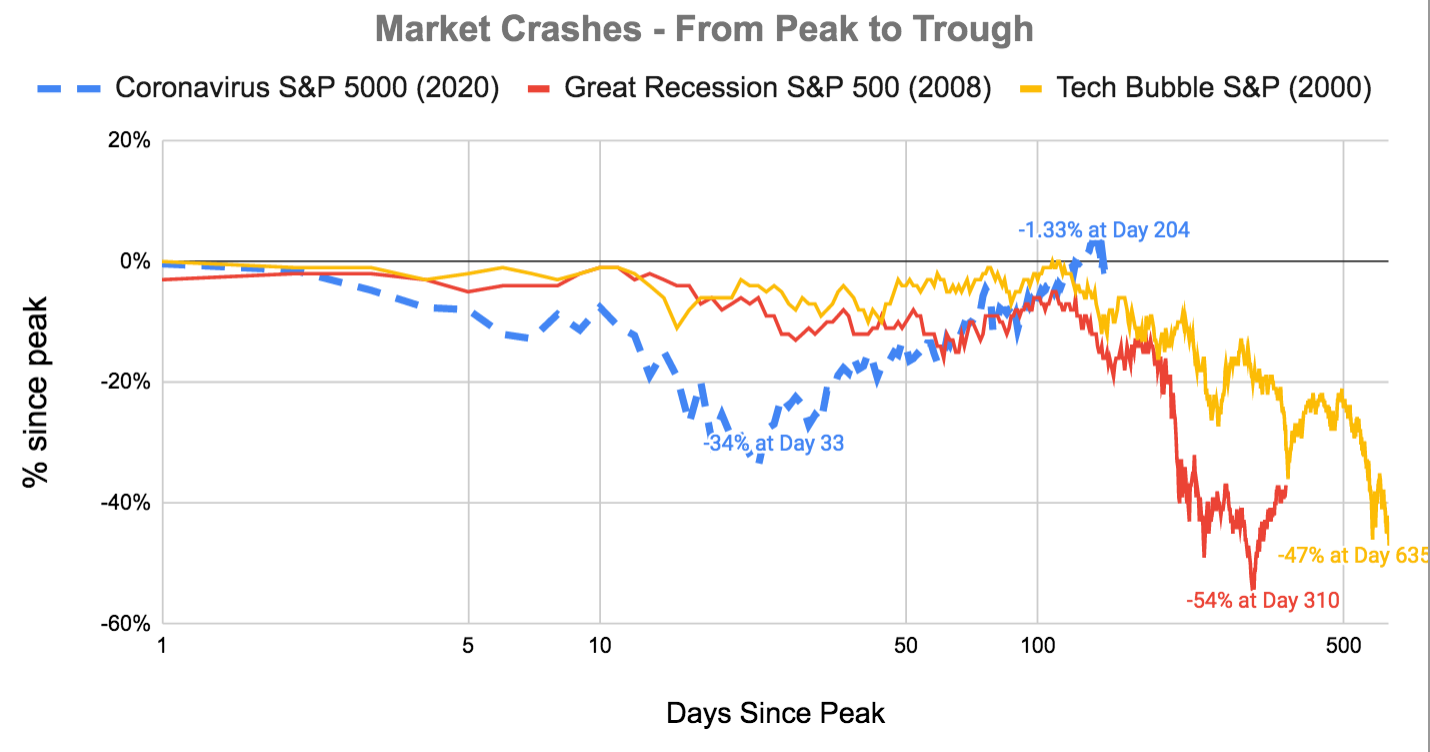

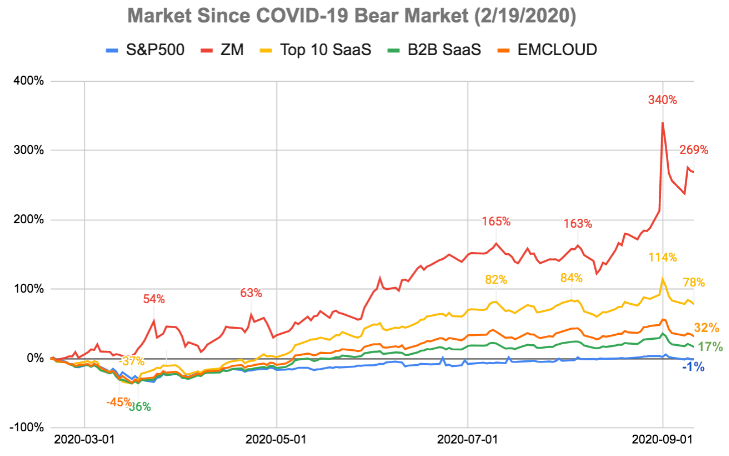

1️⃣ SaaS Stock Prices vs. Benchmarks 📊

Change since bear market start (2/19/2020):

- ZM: +269%

- Top 10 SaaS: +78.0%

- Bessemer Cloud Index (EMCLOUD): +31.9%

- B2B SaaS: +16.6%

- S&P 500: -1.2%

Change in the past week:

- ZM: +2.4%

- Top 10 SaaS: -2.9%

- Bessemer Cloud Index (EMCLOUD): -3.3%

- B2B SaaS: -3%

- S&P 500: -2.5%

Market update📉: Stocks pulled back further from early-week highs in a shortened but highly volatile trading week. Tech stocks fared worst and ended the week in correction territory, or down more than 10% from the all-time high it reached on Sept 2nd. Tech was also among the weakest within the S&P 500 Index, while energy stocks suffered as US oil prices fell below $40/barrel for the first time since July, as Saudi Arabia cut oil prices. The small materials sector outperformed, and industrials shares also proved resilient. The continuing lack of progress in Congress on a new stimulus package also seemed to contribute to the broader market decline this week, as investors worried about the building financial pressures on local governments.

2️⃣ Median B2B SaaS EV/NTM Revenue Valuations

All B2B SaaS: 11.0x

High Growth SaaS: 18.8x

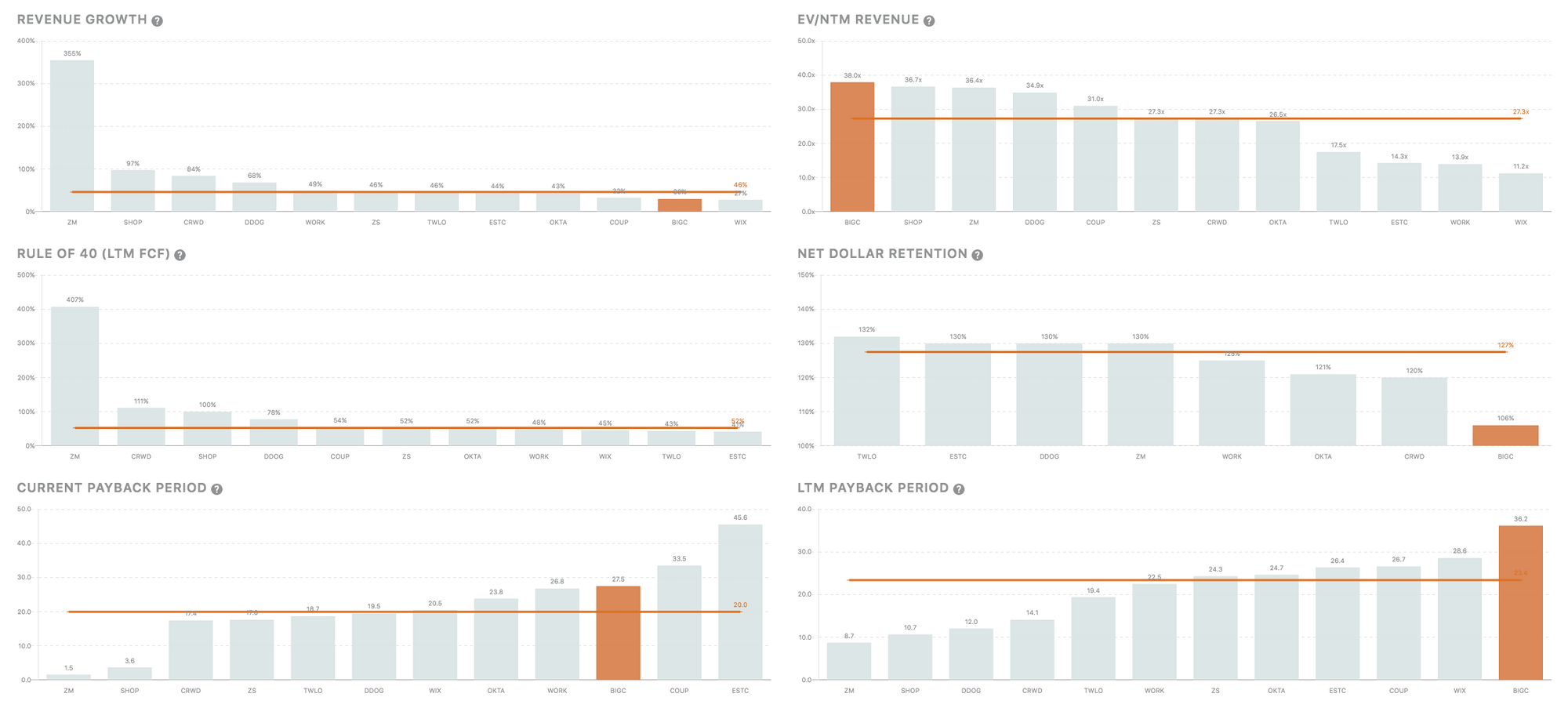

3️⃣ SaaS Earnings - BigCommerce (BIGC) 💸

Press Release | Earnings Call Transcript

Overview

BigCommerce is a $5.5B software-as-a-service (SaaS) platform that powers some of the world’s most interesting and engaging e-commerce stores. BIGC provides everything a business needs to create, manage and grow an online store from the design and hosting of the store through checkout along with the tools that help a business merchandise market, operate and grow. Unlike other e-commerce platforms, BIGC is an open SaaS solution: it offers the benefits of SaaS, but with the APIs and platform openness that allow complex businesses to integrate, modify, and customize their e-commerce stores based on their unique requirements.

Financial Highlights:

Revenue: revenues accelerated to 36.3M in Q2, +33% yoy, compared to +30% in Q1. ARR grew 32% yoy to 151.8M.

Operating Income/net loss/adjusted EBITDA:

- Non-GAAP operating loss improved to -6.2M, up from -9.8M in Q2 2019.

- Non-GAAP net loss was ($7.3) million, compared to ($10.2) million in the second quarter of 2019.

- Adjusted EBITDA was ($5.4) million, compared to ($9.3) million in the second quarter of 2019.

Key Business Metrics

- Number of accounts greater than $2,000 in annual contract value (ACV) was 9,378, up 7% compared to the second quarter of 2019.

- Average revenue per account (ARPA) of accounts greater than $2,000 in ACV was $12,936, up 29% yoy.

- Accounts greater than $2,000 in ACV as a percent of total ARR was 80%, up from 76% a year ago.

- Enterprise account ARR was $79.8M, +44% yoy. As a percent of total ARR, enterprise account ARR was 53%, up from 48% a year ago.

Takeaways from earnings call:

- E-commerce growth: BigCommerce is participating in one of the largest and fastest transformations in human economic history, the global shift in commerce from offline to online. It took 23 years for e-commerce to go from non-existent to 10% of all global consumer spending in 2017. eMarketer predicts it will take just 6 years for this percentage to more than double to 21% of global retail spending in 2023.

- Market Opportunity: IDC estimates that the global market for digital commerce applications was $4.7 billion in 2019 and is expected to grow at a compound annual growth rate of 11% to reach $7.8 billion in 2024. BIGC's TAM is actually larger than that for e-commerce platform spending alone due to the additional revenue earned in partnership with their technology partner ecosystem.

- Improved architecture: BIGC recently completed the rollout of their new storefront architecture. As measured by Google PageSpeed Insights, the platform benchmark is faster than leading e-commerce sites.

- Big customer adds: Added 9 different Forbes Global 2000 corporations, such as Royal Dutch Shell, Diageo, Sharp Electronics, and two of the world’s largest consumer packaged goods companies. Added 390 net new customers with >$2k in ACV.

- Rolled out new orders API: Order Refunds API, which allows merchants and agencies to integrate third-party order management solutions.

- Technology extension partners: signed two new preferred technology partners. Systum, which provides enterprise-grade insight into a merchant’s inventory, orders, invoices and more. 2) bundled B2B which provides B2B sellers with the seamless ability to review transactions and manage customer accounts.

- Payments integrations: completed a number of integrations to support our global merchants, including Elavon, Adyen and WeChat Pay. BIGC also upgraded integrations with Klarna multicurrency, PayPal Vaulting, and Google Pay on Authorize.net and Barclaycard.

- Cross-channel improvements: Enhanced partnership with Facebook & Instagram. This partnership enables merchants to easily connect their e-commerce storefronts catalogs to Instagram and give customers the ability to buy from their favorite brands directly on Instagram.

- COVID-19 impact: Subscription growth rate was down slightly versus Q1 as a result of an essentials plan promotion that BIGC ran during Q2 as part of thei bricks-to-clicks campaign to help merchants during the initial months of the COVID-19 pandemic.

While valuation does still seem high, I believe that the attractive long-term margin potential for BIGC and market consolidation happening among enterprises' online presences give it plenty of runway ahead. Here, I outline some high-level thoughts on BIGC to make sense of the valuation.

High-level Investment thesis on BIGC:

1. E-commerce is still early on the S-curve and decreased barriers to adoption leads to accelerating growth and consolidation of the market.

- A historically fragmented market with heavy friction in setting up an online business: internet/mobile adoption was early, technology was a barrier, payments was a problem which led to a highly fragmented industry where many enterprises chose to set up their e-commerce segment in-house or just remain brick and mortar.

- Huge market opportunity: E-commerce presence is something that every business will fundamentally need in the future economy. TAM is largely unpenetrated, business IT budgets are expanding, and the market is massive.

- COVID-19 accelerated removal of barriers to adoption: forced adoption of e-commerce led to business' online presence being mission-critical. New entrants came in on the demand side as in-person shopping halted, specifically in emerging markets which saw a massive uptick in first-time online shoppers. On the supply side, brick and mortar business came online for the first time. Market acceleration during COVID-19 creates unit growth and mitigates risk.

- Payments is a strong differentiator of BIGC: e-commerce payments have adoption friction from existing enterprises – BIGC can capture a larger share of these because of their breadth of payments integrations rather than uprooting their existing payments methods. Management also understands these pain points (CEO Brent Bellm came from PayPal). Customers choose BigCommerce because of the robust APIs, which enable PayPal’s custom integrations at low cost and fast time to market.

The e-commerce platform revolution that COVID-19 accelerated was the catalyst for market consolidation. E-commerce turned mission-critical, software became a source of competitive advantage which favors developer platforms (BIGC's open SaaS platform), and improving technology platforms that deliver strong value proposition and democratization of e-commerce reduces the portion of in-house e-commerce and helps consolidate the market.

2. BigCommerce is an under-monetized platform relative to peers.

- BIGC's subscription take rate is low:

BIGC isn't likely to raise prices on basic, pro, and advanced because of competition with Shopify (both have the same prices for those tiers), but BIGC doesn't take a cut of GMV the way Shopify does. As GMV continues to accelerate as we saw with Shopify's most recent quarter (119% GMV growth), BIGC will have the flexibility to charge more on its subscription solution.

- BIGC has greater pricing power than competitors: pricing levels for BIGC are based on annual sales, this creates key differentiation in their product and is more efficient for customers. The enterprise plan is also variable pricing, so customers are less sensitive to price changes and BIGC aligns themselves to win with their customers.

3. BigCommerce will be a near perfect substitutes but currently trades at a massive discount to Shopify

- BigCommerce didn't begin investing in enterprise customers until 2015: Its still the most underserved market, as incumbent competitors were on-prem and losing market share.

- BigCommerce employs the efficient "land and expand" model more effectively: multi-tenant SaaS architecture is versatile, enterprise customers have high retention rates, and BIGC is incentivized to win with their customers by having them move up subscription tiers.

- Platform integrations & Open SaaS model provides more customization: customers value customization and don't want to pay for app store purchases.

- Compelling unit economics are likely to expand: mission-criticality/variable pricing should improve churn and prolong LTV. Sales cycles should shorten with accelerated demand, growth of ecosystem/partnerships should lead to improved long-term sales efficiency.

- Long-term, BIGC converges on SHOP's subscription offering: BIGC added 715 net adds in 2019, compared to SHOP which added 1800 new plus merchants. Both products will likely look very similar, but BIGC's long-term margins are more compelling as SHOP becomes more of a payments company. BIGC

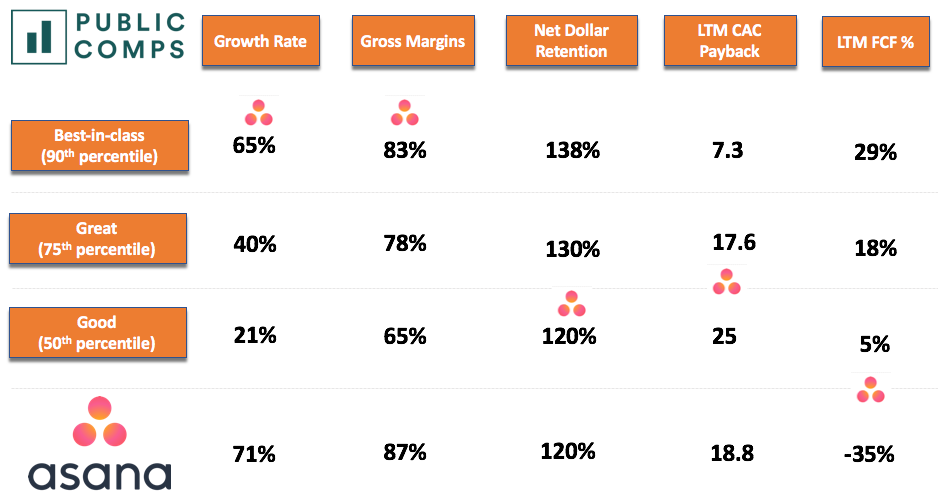

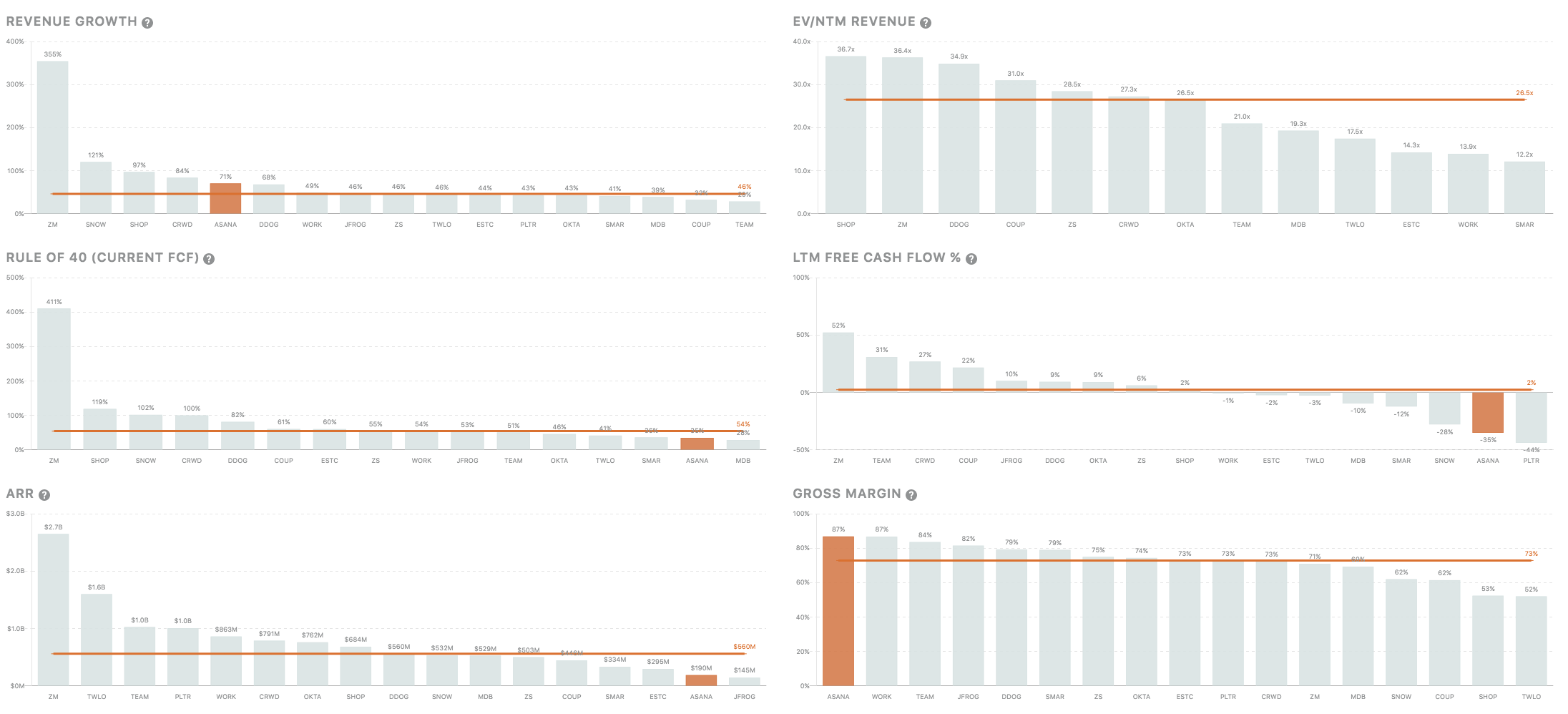

4️⃣ Asana's S-1 Teardown Thoughts

Yesterday, I published an S-1 teardown on Asana.

Here are some interesting insights & charts from it:

How Asana benchmarks with other B2B SaaS:

Market Opportunity:

According to a June 2019 IDC report, the TAM for collaborative applications and project and portfolio management is expected to grow from $23B in 2020 to $32B in 2023 (11.6% CAGR).

In a September 2019 report by Forrester Research, they estimated there to be 1.25B global information workers. Asana believes they are "less than 3% penetrated among addressable employees in our existing customer base, indicating a significant whitespace opportunity".

Asana vs. high growth SaaS:

Stay safe everyone,

Albert Wang, Public Comps Team

albert@publiccomps.com

Like these weekly dashboards? These are for Publiccomps.com customers only but you can have your friends subscribe to the newsletter here where we send out investment memos, market maps and analysis on the broader SaaS market.

Views expressed in theses emails are ours and ours alone and don't represent that of our previous or current employers. Public Comps provides financial and industry information regarding public software companies as part of our weekly dashboard, our blog, and emails. Such information is for general informational purposes only and should not be construed as investment advice or other professional advice.

Full disclosure: I own CRWD, TWLO, SHOP, LVGO, FB, MSFT, DDOG, ESTC, AYX, SMAR, PLAN, ZM and BILL.