Why Product Led Growth Companies Win

What is and isn't Product Led Growth? Do PLG companies win? What tools to use if I want to be more PLG?

Product Led Growth (PLG) is all the rage today. In this post, we try to understand what is and isn't product-led growth even though it seems like every company positions themselves as "product-focused" and "customer-obsessed". We also quantify how much better off PLG companies are versus companies that aren't.

First things first, what is Product-Led Growth?

What is Product-Led Growth

Here's how Openview's Blake Bartlett defines Product-Led Growth:

Product led growth (PLG) is an end user-focused growth model that relies on the product itself as the primary driver of customer acquisition, conversion and expansion.

Product-Led Growth is basically a Go-To-Market strategy that focuses on delivering value to the end user in an era where end users are swiping credit cards to buy software products to solve annoying pain points. Given the bottoms-up product adoption motion, PLG emphasizes delivering value before a paywall, minimizing the amount of friction for a user to get value from a product, and focus on solving a user's pain point as opposed to figuring out what is the right ROI to convince a buyer with a budget to buy your product. PLG is not just a bottoms-up sales motion: it involves prioritizing product usage as a north star metric as the key primary strategic driver.

Aside: I find Openview a credible thought leader in the PLG space given that they're investors in Calendly, Datadog, Expensify, among others that are products that are loved by end users.

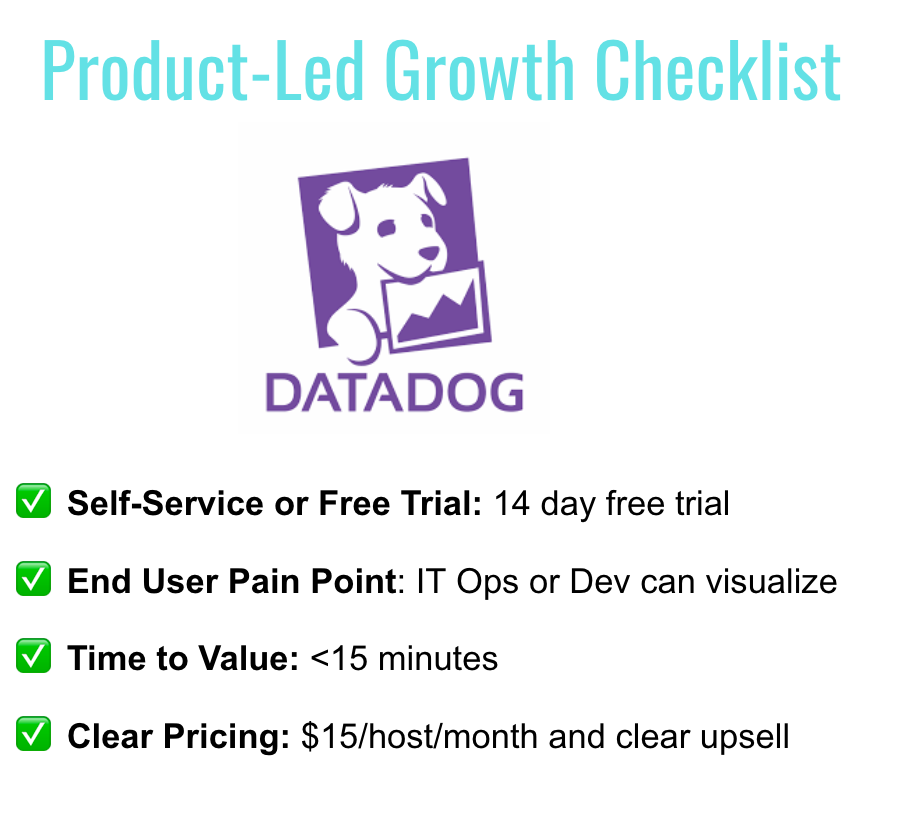

Product-Led Growth Checklist

Here's our mini-checklist of what it take to be PLG.

- ✅ Self-Service or Free Trial: Can I buy the product with a credit card or use the product without talking to a sales rep?

- ✅ End User Buyer: Is the buyer the end user of the product and solving the buyer’s pain point?

- ✅ Time to Value: Can I get value out of the product without having to talk to a person

- ✅ Clear Pricing: Is there a clear pricing page? Is the paywall after I get value from the product? Is it clear how I’d pay more for additional products & services?

- 😂 Emojis: does the company use excessive emojis in explaining how to use the product 🔥. Just kidding.

What is Product Led Growth and What Isn't?

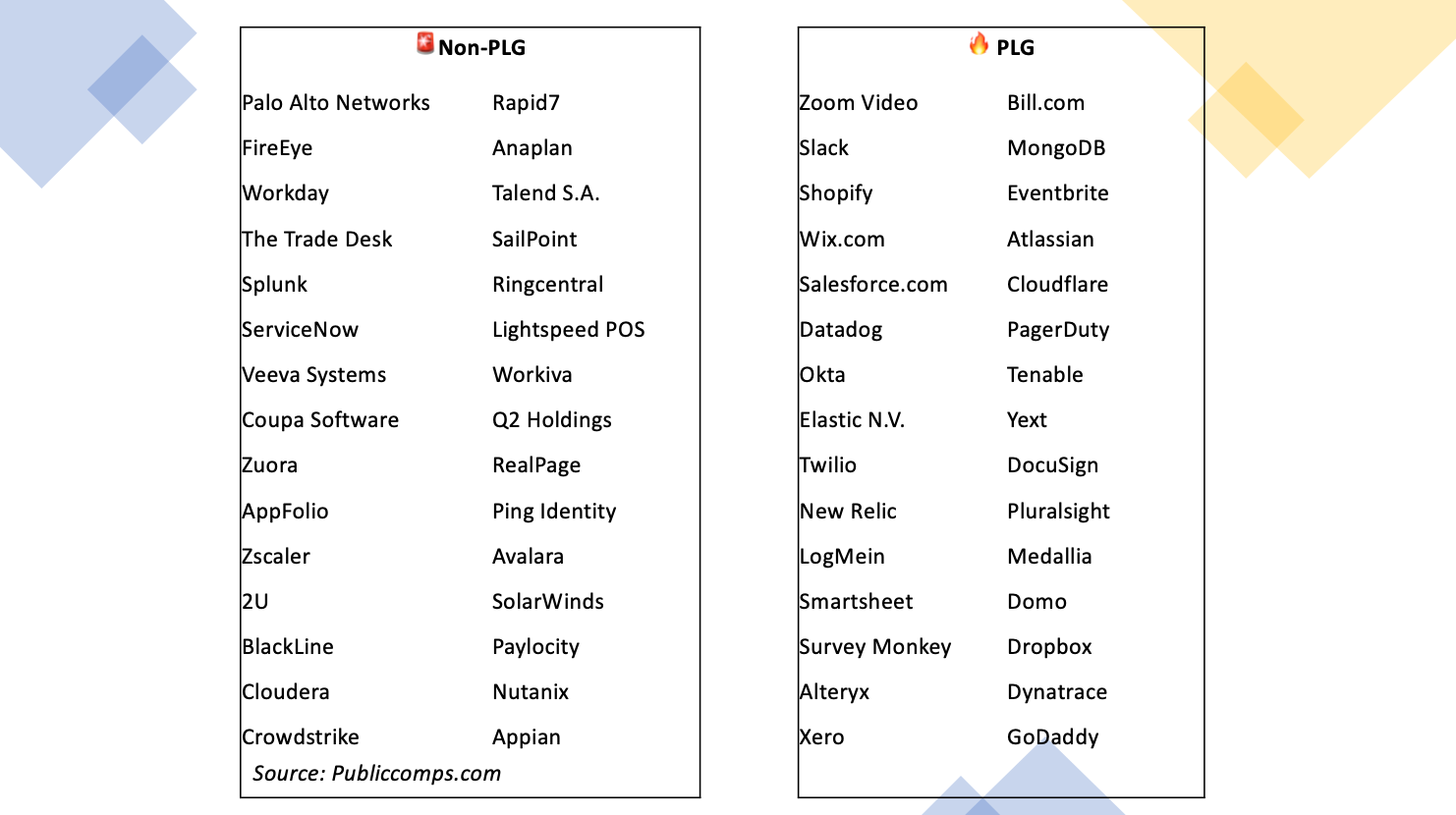

To understand what is Product-Led Growth and what isn't, I went down the list of Publiccomps.com's list of high growth SaaS Companies and tried to figure out which companies checked all or most of the boxes above and which ones didn't. Here's my finding below. I also argue why Datadog is clearly a Product-Led Growth company and why Crowdstrike isn't.

Datadog is product-led growth

Datadog provides cloud-based monitoring and analytics for developers, IT operations and business teams to monitor the health of their cloud infrastructure and applications.

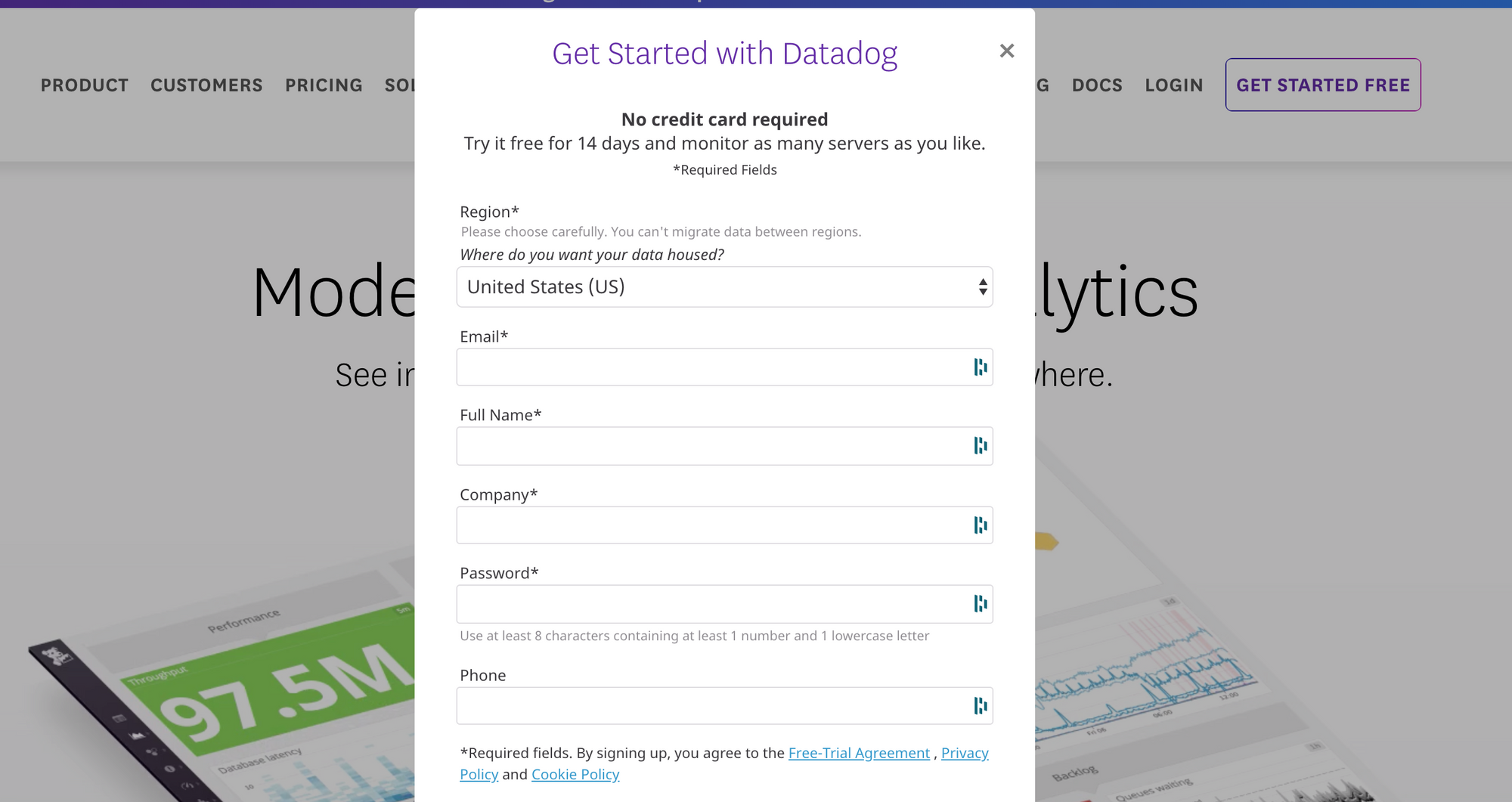

Signing up for Datadog is very simple: you click "Get Started Free" on their site and fill in some basic information and then you're off to the races:

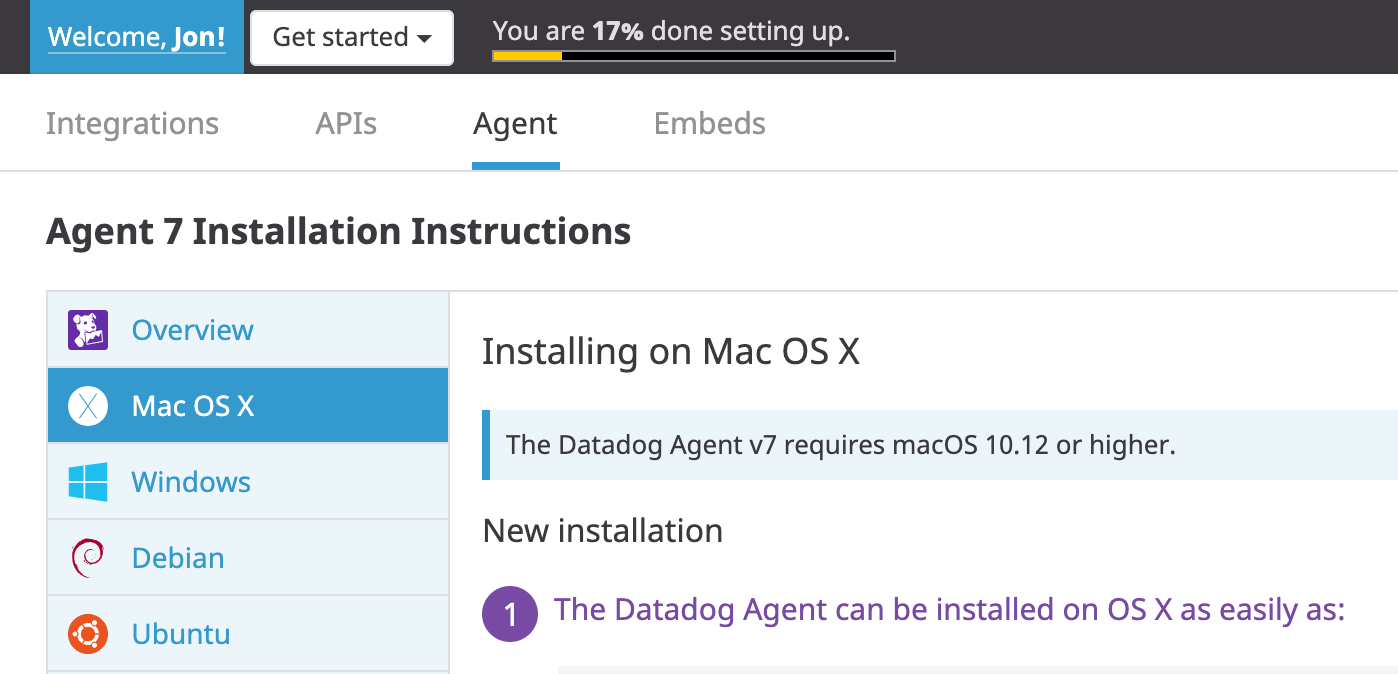

Datadog provides a 14-day trial and once you're signed in, they provide a very easy way to install an agent via an easy installation guide.

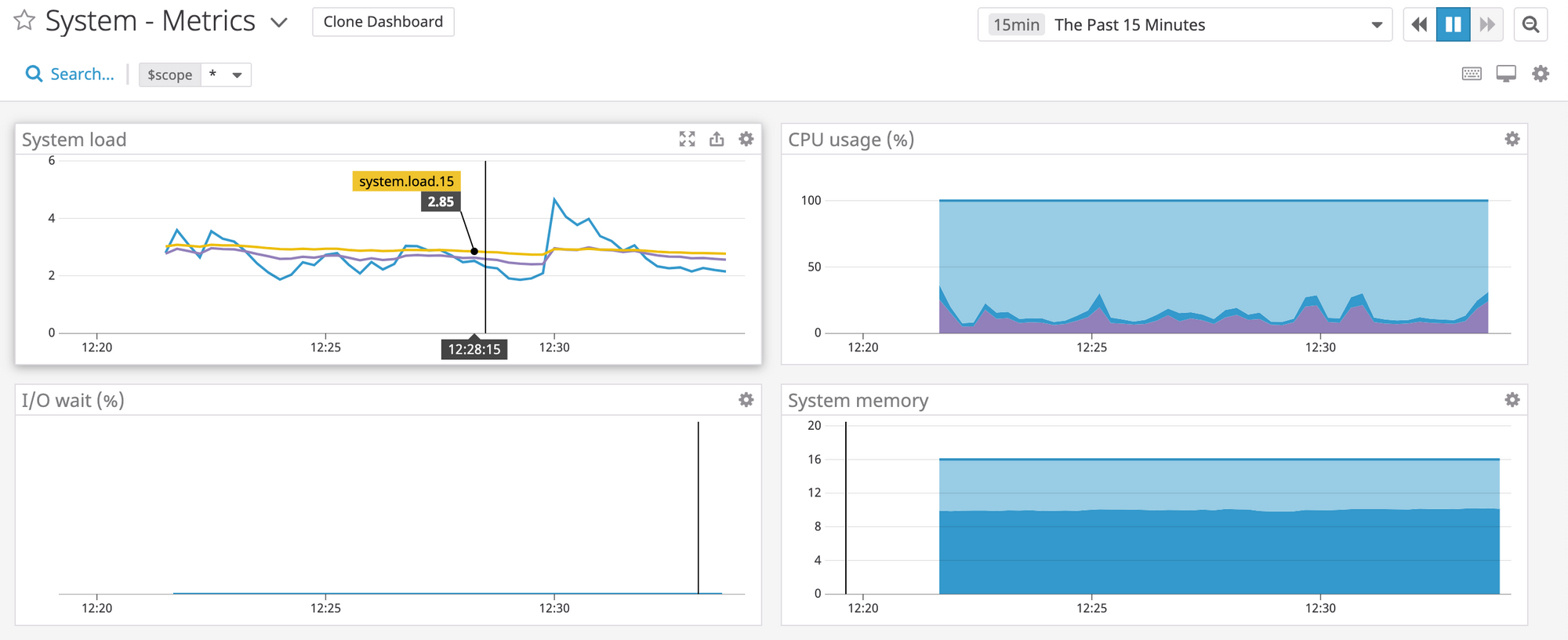

Once the agent is installed, I can start getting the value of Datadog by visualizing the system metrics on my Mac.

The entire process from sign up, to installing the Datadog agent on my laptop, to getting value from visualizing the system metrics took <15 minutes.

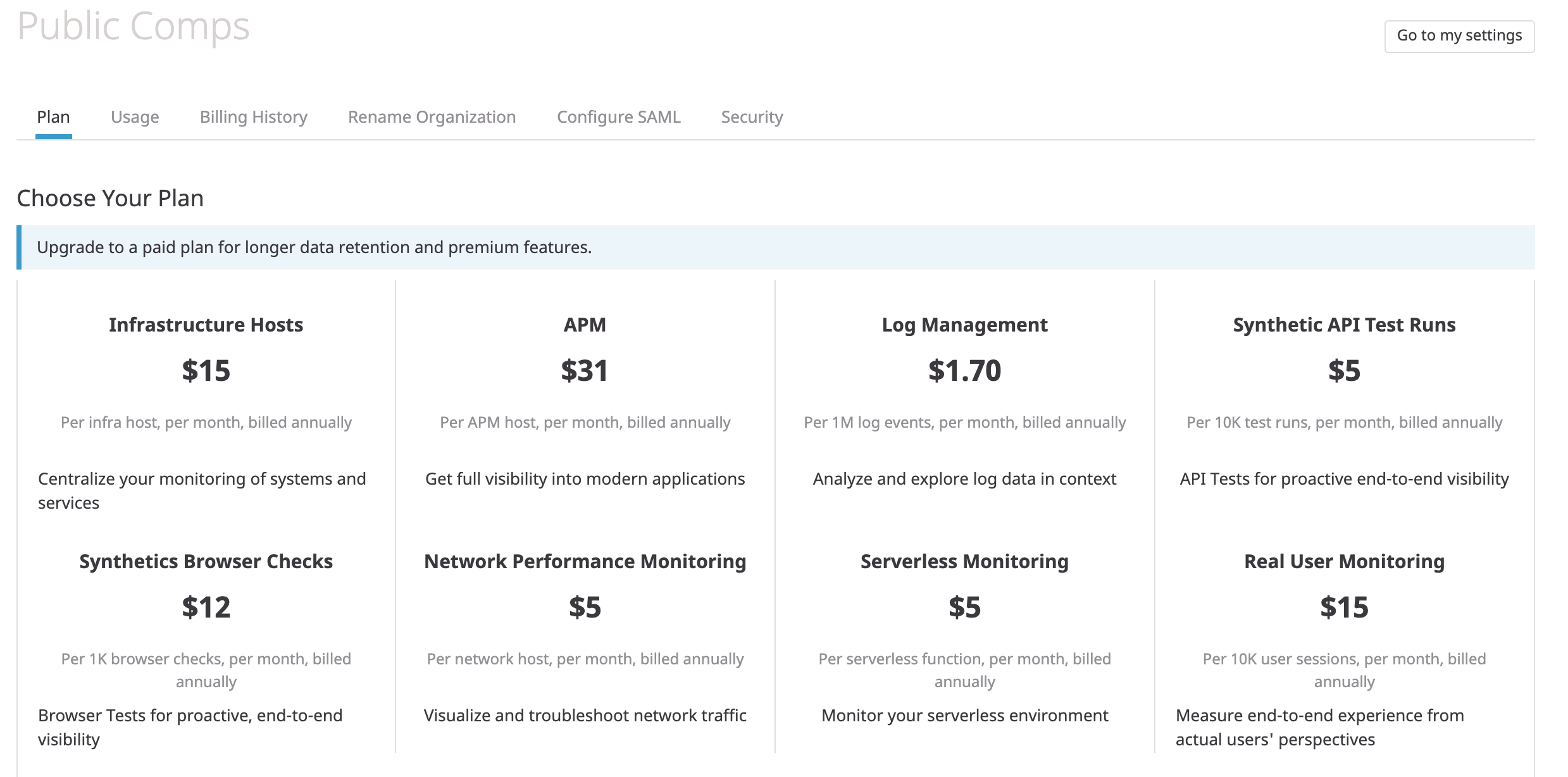

Lastly, it's very clear from their pricing menu how much I'll have to pay after the 14 day free trial and if I'm happy with the system metrics, I can easily pay more per month to get the APM, logging, etc products.

Datadog checks the boxes of "Product-Led Growth" and they point out the importance of time to value in their S-1

"We employ a land-and-expand business model centered around offering products that are easy to adopt and have a very short time to value. Our customers can expand their footprint with us on a self-service basis. Our customers often significantly increase their usage of the products they initially buy from us and expand their usage to other products we offer on our platform. - Datadog S-1"

Here are some observations

👉Developer and IT Ops tools can be PLG: one traditionally thinks of Slack, Dropbox, Zoom as product-led growth companies but its fascinating to see a company like Datadog that sells monitoring and analytics to developers and IT operations teams can also create a low friction and fast time to value proposition in a traditionally long sales cycle industry.

👉PLG enables low CAC so more investment in R&D: the point of having low time to value is so that teams like Datadog require fewer customer support or sales reps and so the business can invest more in product. Here's a blurb from their S-1 echoing this point: "Our efficient go-to-market model enables us to prioritize significant investment in innovation. We have proven initial success of our platform approach, through expansion beyond our initial infrastructure monitoring solution, to include APM in 2017, logs in 2018, and both user experience and network performance monitoring in 2019"

Crowdstrike is not "product-led growth".

Crowdstrike is a cloud-delivered endpoint detection software business that allows security teams to protect companies from breaches. Crowdstrike is effectively a cloud-based and next-generation AV company (e.g think of the old guard of AV like Symantec).

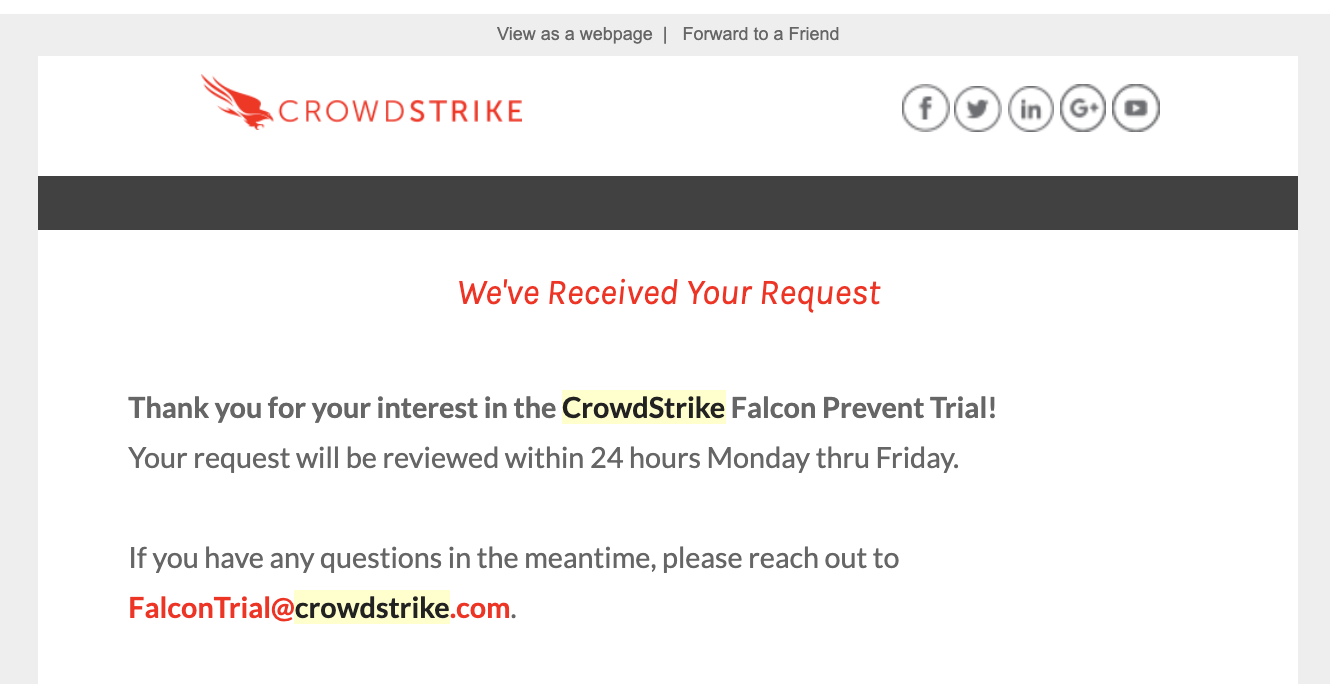

I went on Crowdstrike's website and could "Start a Free Trial" but after filling out my information, I received an email that my request would be reviewed.

Unlike other personal AV solutions like Malwarebytes where I can easily "download" their product as a consumer (or small business), there's no immediate way to "test out" Crowdstrike and get a quick time to value after signing up.

What's interesting to note is that relative to other on-premise competitors, Crowdstrike prides itself for having a short time to value by allowing security teams to install agents and deploy their platform in <24 hours. See the blurb from Crowdstrike's S-1 below.

I had a difficult time deciding if I should bucket Crowdstrike as PLG or not and ultimately decided

Here are some observations

👉Pure Self-Service isn't suitable for all software products: Certain software companies with sensitive enterprise security products may not be well suited for "self-service" given that their products could be exploited by potential adversaries.

👉A company is PLG relative to its industry: While Crowdstrike doesn't have a frictionless on-boarding process and the time from sign up to value may take longer than say a Dropbox, Slack, etc, Crowdstrike provides value much more quickly by installing in <24 hours versus incumbents which may take weeks. While on face value Crowdstrike isn't "Product-Led Growth", it is definitely more product oriented than the rest of its competitors. Here's a snippet from their Dec '19 earnings transcript on how Crowdstrike has continued to upsell customers with new cloud modules.

In the third quarter, the percentage of customers that have adopted four or more cloud modules, increased beyond the 50% we reported last quarter. Additionally, I'm pleased to report that customers with five or more cloud modules increased to 30%. -George Kurtz CRWD Q3 2020 Transcript

Here's why Product-Led Growth Companies Win

We now get to the fun part of looking at data comparing PLG companies and non-PLG companies. The questions we ask ourselves are "how much better are PLG companies versus non-PLG companies at IPO? Today?".

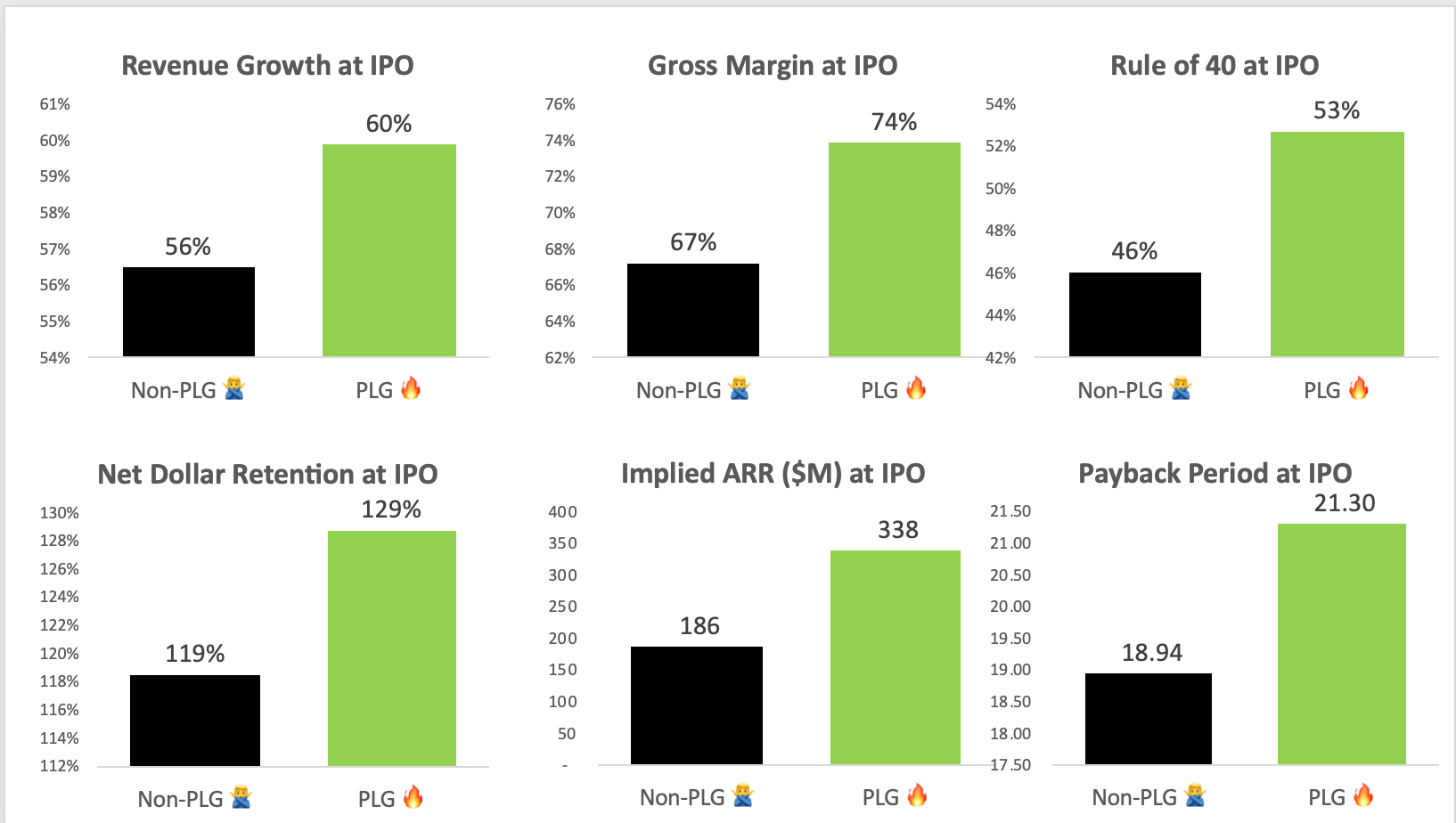

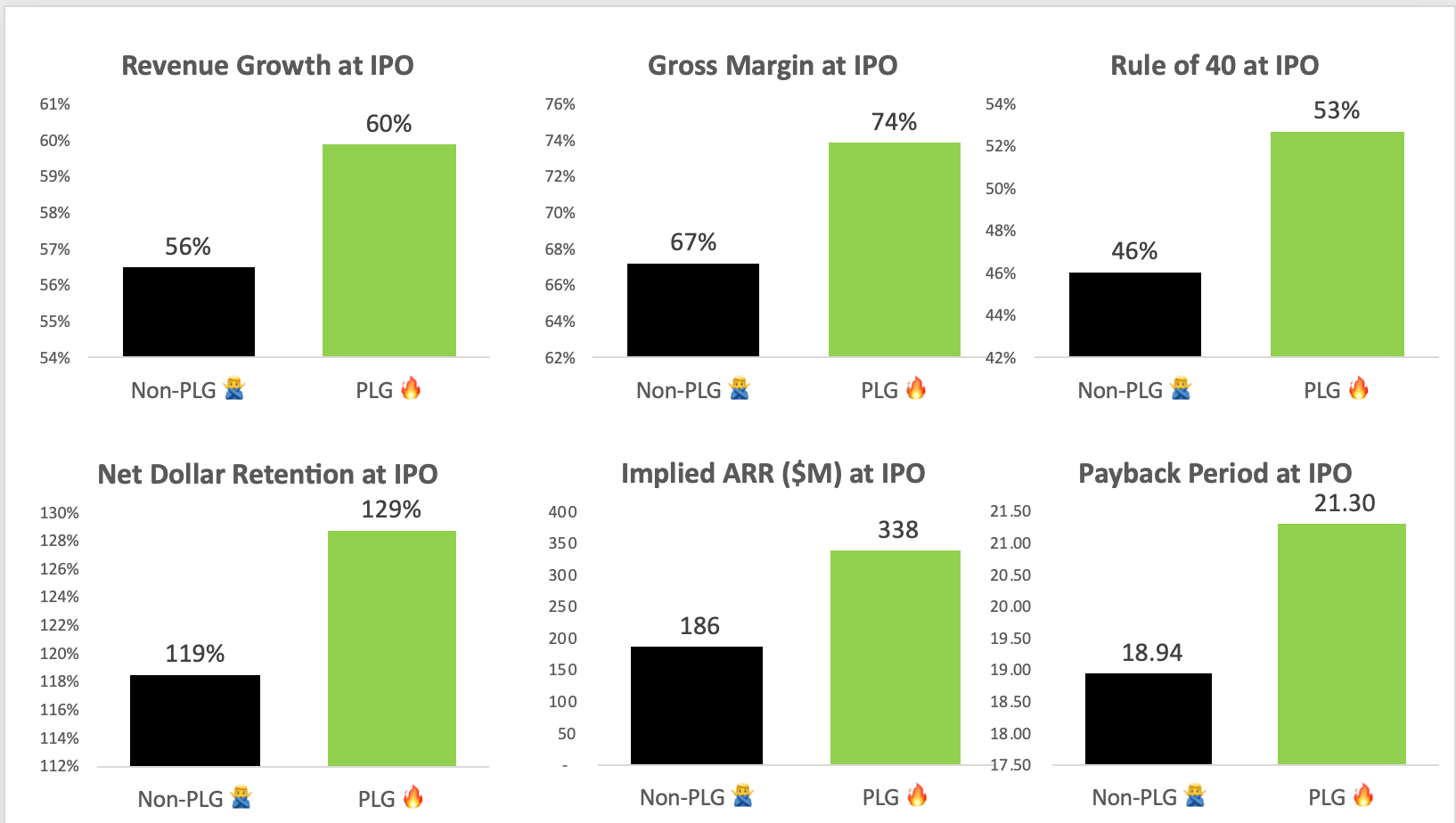

Product-Led Growth companies at IPO on average have:

👉Faster growth rates faster than non-PLG Companies (+4% YoY Revenue Growth): This isn't surprising as bottom-up and self-service companies can grow rapidly and scale faster than a traditional top down enterprise software company.

👉 More revenue at IPO (+$152m ARR): this is likely skewed by IPOs like Dropbox, Slack, Zoom, etc that went public in the last 2-3 years with more and more revenue at IPO. Either way, this shows that PLG companies can grow quickly with more revenue scale.

👉Higher net dollar retention (10%+ Net Dollar Retention): this is perhaps the most important and interesting aspect of PLG vs non-PLG: PLG companies can expand quickly within companies due to the viral aspects of a Zoom, Slack, Dropbox, etc that can drive value the more usage there is within an organization.

👉Higher Gross Margin (7%+ Gross Margin): I suspect PLG companies have higher margins on average because they don't need to employ as many customer support folks or require as much services as a traditional enterprise software company.

👉Higher Rule of 40 (LTM FCF % + Revenue Growth %) (+7%): What this is saying is that PLG companies are on average faster growing and more capital efficient than non-PLG companies.

👉Higher Payback Period: this is surprising as one would expect PLG companies at IPO to have a lower payback period given the self-service nature of their products. Keep in mind what is our definition of payback period: Previous Quarter Sales and Marketing/Net New ARR. For some of of our PLG companies, their Net New ARR is flat or declining relative to an increasing spend in S&M which drives up a higher payback period. For example, Domo (83 months), Survey Monkey (46 months), Medallia (36 months) all have really long payback periods despite being "PLG". It's worth noting then that not ALL PLG companies have low payback periods.

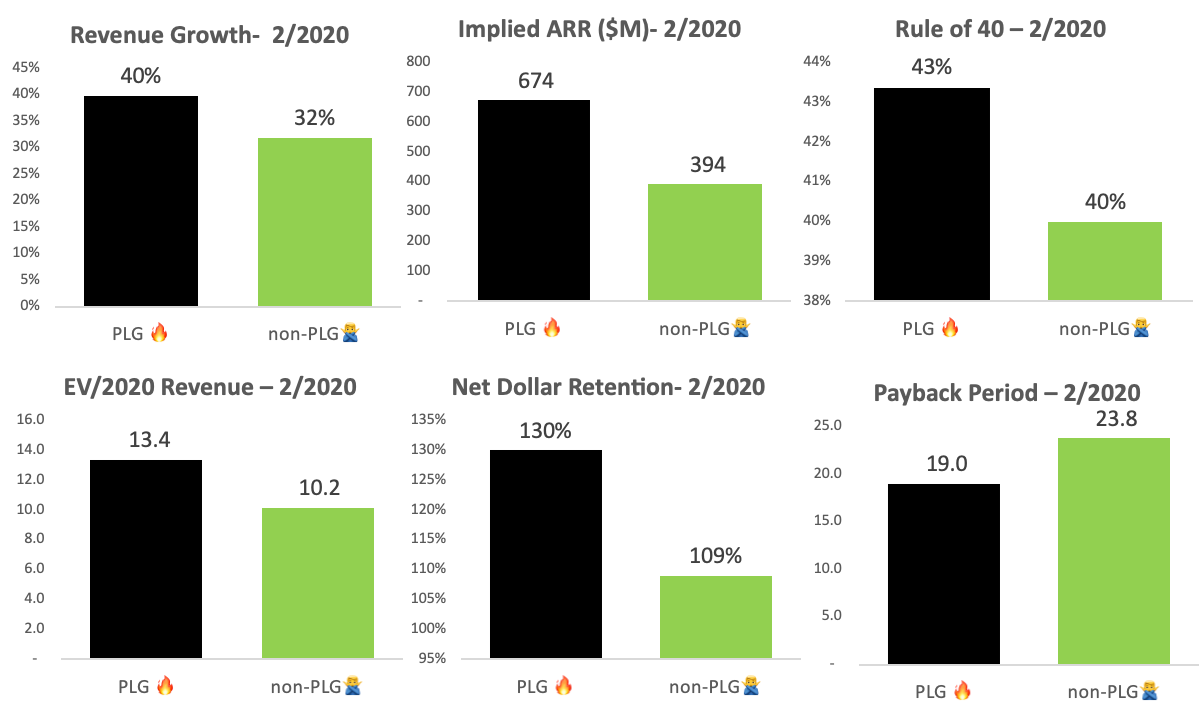

Product-Leg Growth companies today on average have:

👉Faster growth rates faster than non-PLG Companies (+8% YoY Revenue Growth): similar to the finding above but keep in mind this is for companies currently versus the previous graph is looking at these SaaS companies at IPO.

👉 More revenue (+$280m ARR)

👉Higher net dollar retention (21%+ Net Dollar Retention)

👉Higher Rule of 40 ( +3%)

👉Lower Payback Period (-4 months): this fits better with the belief that PLG companies likely spend less to acquire a customer as there's more word-of-mouth or built in distribution in PLG products like Zoom, Slack, etc that have natural vitality built in which lowers your cost of acquiring a customer and hence payback period..

👉Higher Revenue Multiples (+3.2x): this is saying that on average, PLG companies have a higher revenue multiple than a non-PLG company. This is not saying that holding everything constant, PLG companies have higher multiples – it's because of the higher growth rates, more revenue scale, higher retention rates, etc that make investors invest these businesses more.

What can you do to be more product-led?

This is a question Howard and I ask a lot at Publiccomps.com. We share some products that we think can help create processes to help teams be more product-led growth oriented:

- Product Board: Product Board seems like a great product to organize sprints, help prioritize features that have the greatest impact, and gather insights from customer conversations. I'm a big fan of how Loom lays out their product roadmap and allows users to submit ideas via their product board. Product starts at $59/month.

- Appcues: Appcues is the product-led growth platform that allows you to build flows to make the on-boarding process seamless. We started using Appcues to help explain new features to existing users and walk new users through our product. The product has forced us to think about what are the key steps we need to take to "activate" a given new user to be successful. The product starts out at $250/month.

- Logrocket: Logrocket lets teams replay what users are doing on their website and makes it easy to reproduce bugs and fix issues faster. We use Logrocket a ton to track how users are interacting with our product without having to ask them to sit down for a user interview. LR also has some great metrics around who uses our product the most, how much time do they spend using our product, etc. Lastly, bugs can make or break a user's product experience so we love LR because we can fix bugs quickly. Logrocket starts at $99/month.