Upstart (UPST) Business & Q3'21 Earnings Teardown

A deep dive on Upstart and why investors have wrangled the business.

Real inefficiencies create real opportunity for disruption, and it’s no question there’s massive opportunity that FinTechs are capturing on a global level.

Up 152% since its listing in 2020 and down 72% from all-time highs, Upstart (UPST) has had a turbulent run in the public markets. In this piece we break down:

- A brief overview of lending & why there's opportunity for FinTechs

- What Upstart does, for consumers & partner banks, on a user level

- Why public markets have wrangled over Upstart's value

- Q3 financials and takeaways

A Background on Lending, and Upstart (UPST)

Within US lending alone, I’m a believer that many consumers are still massively underbanked — not just in the literal sense, but more than half of America is either “credit invisible” or do not have access to prime credit. As the financial sector has rapidly consolidated over the past decades, certain financial products within lending have only become less inclusive as incumbents continue to rely on legacy methods of assessing credit like the FICO score. Today, it has resulted in a plethora of underbanked communities, including immigrants, college students, and disadvantaged individuals who struggle with how the current financial system dictates access to credit.

"Unfortunately, because legacy credit systems fail to properly identify and quantify risk, millions of creditworthy individuals are left out of the system, and millions more pay too much to borrow money.” — Upstart, 2020 10-K

Founded in 2012, Upstart started as an innovative FinTech business: they wanted to disrupt the spaces that were historically underbanked, and began with student loans. However, instead of debt that we’re familiar with today, they’d offer a product for students to effectively sell X% of their future earnings for Y amount of years in exchange for a lump sum of money. For instance, if you wanted to take out a $50,000 loan to pay for your tuition as an independent college student, you’d be obligated to pay 10% of your annual future earnings for 10 years back to Upstart.

The product ultimately struggled to find adoption — it was a wildly new concept that many students were, frankly, afraid of. However, the premise of using statistical models to underwrite loans to borrowers with thin credit files was built. Eventually, the team took these learnings and expanded into personal loans in 2015, which immediately gained traction because it was a product that was 1) far less daunting to consumers and 2) popularized because of the initial excitement around peer-to-peer (P2P) lending platforms like LendingClub.

We dive into Upstart, a highly debated business among investors at the forefront of targeting consumers with non-prime credit.

Product Overview

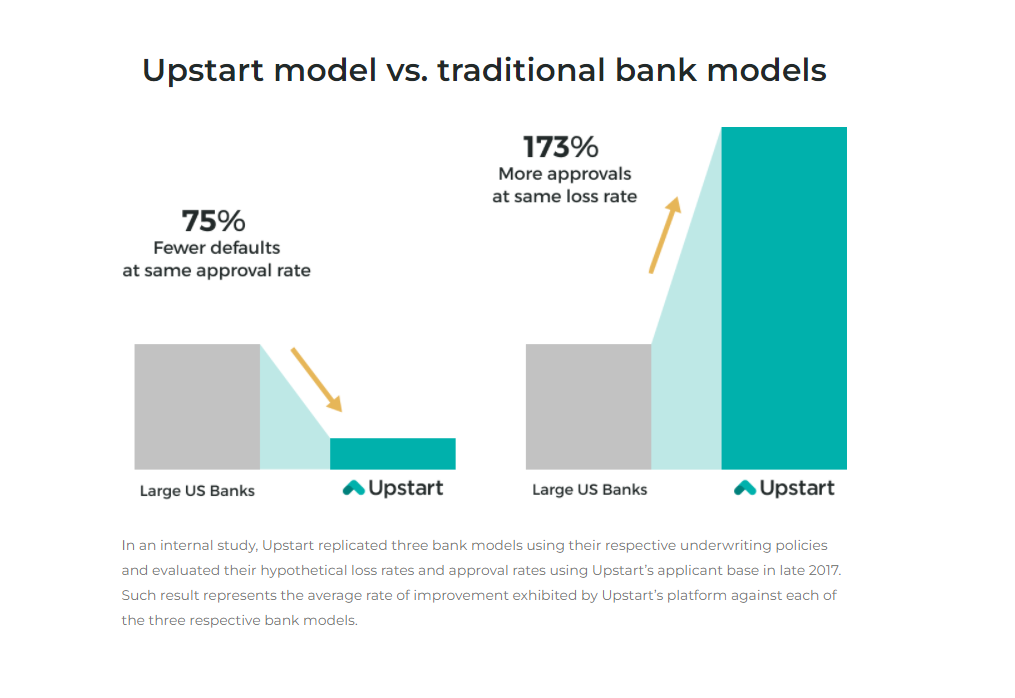

At its core, Upstart is a cloud-based lending technology platform for banks to originate loans to consumers. However, rather than relying on criteria like FICO scores that were introduced in the 1980s, Upstart’s origination process factors in employment history, alma maters, cost of living, and even simple interactions that individuals have had with loan applications in the past. Incredibly, internal studies suggest they approve >173% more loans at <75% default rates compared to legacy underwriting models.

Inherently, Upstart drives a substantial data moat — the company tracks 1,000 co-dependent variables and is trained on an ever-growing 17M+ repayments events from the bank partners that are on their platform.

Although Upstart started in student loan, expanded into personal loan, and recently originated their first auto loan just over a year ago, the company’s main source of business is for its AI-driven platform that helps banks originate personal loans to non-prime consumers.

The way in which Upstart is able to thrive with its technology layer is really through a simple three-part system: consumers, bank partners, and institutional investors.

1. Consumers: Individuals are made aware of Upstart loans either via Upstart.com or through loan offers that actual bank partners place on their platforms. Any consumer, even individuals like college students with historically thin files, can apply for credit in a very simple process. I timed a quick run-through of my experience applying for a loan to pay off credit cards, which took me less than two minutes to get to a rate check (!). That’s incredible given that 23% of rate requests converted into loan originations last quarter.

That level of speed and automation is the same case for approvals: ~70% of Upstart-powered loans in 2020 were instantly approved with no document upload or phone call (per 2020 10-K), compared to traditional banking services where documents like tax returns, pay stubs, renting history, are much more likely to be required. Albeit the year of the pandemic, it’s also worth highlighting that ~50%+ of people who applied for Upstart loans in 2020 was done entirely through a smartphone.

“I really needed a personal loan following my divorce to split the shared community debt between me and X... within the hour, I had an approved debt consolidation loan.” — Customer testimonial, Upstart

2. Bank partners: Banks are equipped with a user-friendly cloud application, meaning that highly complex AI models are abstracted from loan officers. Additionally, the platform is highly configurable, meaning that partners can easily customize their lending program to what they deem as “creditworthy”.

For example, if a bank partner only wanted to lend to individuals within certain parameters such as a <36% debt-to-income (DTI) ratio or if they only wanted to originate loans with a 3+ year period, Upstart’s platform allows them to.

“Upstart’s model was able to deliver better returns, lower default rates, and reduced risk of fraud. We’ve grown the program from a small pilot to a full-scale lending program that’s continued to meet and exceed our expectations.” — Vice Chairman and COO, Customers Bank

3. Institutional investors: A big reason that bank partners are evidently so active in origination with Upstart loans is in part due to the strong network of institutional investors that fund Upstart debt in secondary markets, where investors/buyers participate through loan purchases, purchases of pass-through securities, and direct investments in asset-backed securitizations. In 2020, only 21% of originated loans were retained by the bank partners’ balance sheets, and a total 77% of them were sold to investors.

Additionally, these loans are generally well-covered by credit rating agencies and credit underwriters given their low loss rates, which helps banks and investors in the secondary market gain confidence for Upstart-powered debt. Given that the majority of loans are sold off after initial origination — 77% in 2020 — Upstart’s network of institutional investors plays a huge role in providing liquidity for lenders.

Business Model

Upstart’s business model consists almost entirely of fees (98%) in exchange for providing the cloud-based technology infrastructure that their bank partners use for Upstart-based loans. The three primary fees that drive the top-line are:

- Referral fees from bank partners for loan traffic originated through Upstart.com

- Platform fees from banks for each loan originated regardless of where it is originated (be it Upstart.com or the bank partner’s site)

- Loan servicing fees from consumers as they repay their loans

One advantage worth pointing out is Upstart’s operating leverage, which further improves unit economics, because of how automated the platform is. They’re able to capture fees from every part of the ecosystem they operate in a way that requires almost zero SG&A expense.

Upstart’s business makes for a great example of why FinTechs that have lodged themselves right within financial services are so cash-generative: they’re capital light, TAMs are large (~$81B alone in personal loan originations), revenue is recurring (albeit a derivative), and moats are often driven by data.

The State of Upstart in 2022

Up 152% since its listing and down 72% from its all-time highs, Upstart has had a turbulent run in the public markets as investors wrangle over varying views. Across my own analysis of sell-side reports and retail/institutional sentiment, I outline what I believe to be primary points of contention among investors and my thoughts on them:

- Customer + counterparty concentration: There’s an argument to be made regarding Upstart’s current reliance on certain businesses from both a revenue stream and an operating business model standpoint. It’s been noted many times that Cross River Bank, one of the largest capital providers for a huge number of FinTechs, accounted for 63% of Upstart’s total revenue and originated 67% of the loans facilitated on Upstart’s platform in 2020.

- Although not a mitigant so much as the industry norm, the reliance of a single institution for the origination of loans is not something that’s incredibly alarming. The alternative — which is quite common — is to simply have a backup bank. For example, if you look at LendingClub, the original P2P lending marketplace, it relied on WebBank as its primary bank for nearly 10 years and never originated a single loan through their backup bank (which was coincidentally Cross River!). Industry experts claim that it’s mainly for compliance reasons as well as a preference from the actual banks to be a sole B2B lender.

- Competitive pressure in the non-prime space: What I’m personally much more concerned about is the competitive pressures that may arise as other FinTechs look to capture the hundreds of millions of Americans with non-prime credit. It’s evidently a huge market, and competitors I can think of like Mission Lane are targeting very similar consumer challenges as Upstart. For instance, they offer a credit card for non-prime members based on data that isn’t solely reliant on a credit score.

- The way I see it: Upstart's competitive positioning is really a function of its first-mover advantage, which yields two moats: trust and data. The reason that traffic through Upstart's website for consumers is a key driver of loan origination is because the business has established a credible consumer brand, which isn't a light task especially as an emerging fintech. On the banking side, Upstart-powered loans are trusted by banks and the institutional investors that fund them because of Upstart's track record of low loss rates that it originates with its models. At 17M+ data points today, the training data that informs Upstart's models only grows faster, which drives the data moat that makes it difficult for competitors to replicate.

- Broader macroeconomic implications: Although applicable to nearly all verticals within financial services, lending is particularly tied with broader macroeconomic factors. Upstart, Cross River, and the lending arms of traditional institutions are great when rates are low and originations are abundant, but it’s the complete opposite case in higher-rate environments with much lower levels of liquidity. The pandemic made for a great example: after stimulus checks, near-zero rates, and trillions of dollars spent on quantitative easing, there’s no doubt that loan volumes were monstrous as a direct consequence.

- However, the bull case is based on the premise that consumer borrowing trends will be in favor of Upstart’s personal lending products.

In terms of macro outlook, we are seeing the early signs of a return to the pre-COVID consumer profile with personal savings rates in the economy having fallen back to pre-COVID levels, and credit card balances steadily edging upwards to within 90% of pre-COVID levels... We also expect these macro dynamics to ultimately lead to an increase in borrower loan demand. — Sanjay Datta, Upstart CFO, Q3’21 earnings call

- Given that origination volumes during the pandemic were insanely high due to the wonderful combination of stimulus, low rates, and liquidity in virtually all markets from both fiscal/monetary policy, it’s difficult to justify that thesis emerging from the current macro environment. However, I believe it’s possible the Upstart thesis may mitigate the revenue deceleration they will likely experience as rate hike continue and origination volume slows.

Q3 2021 Financial Highlights

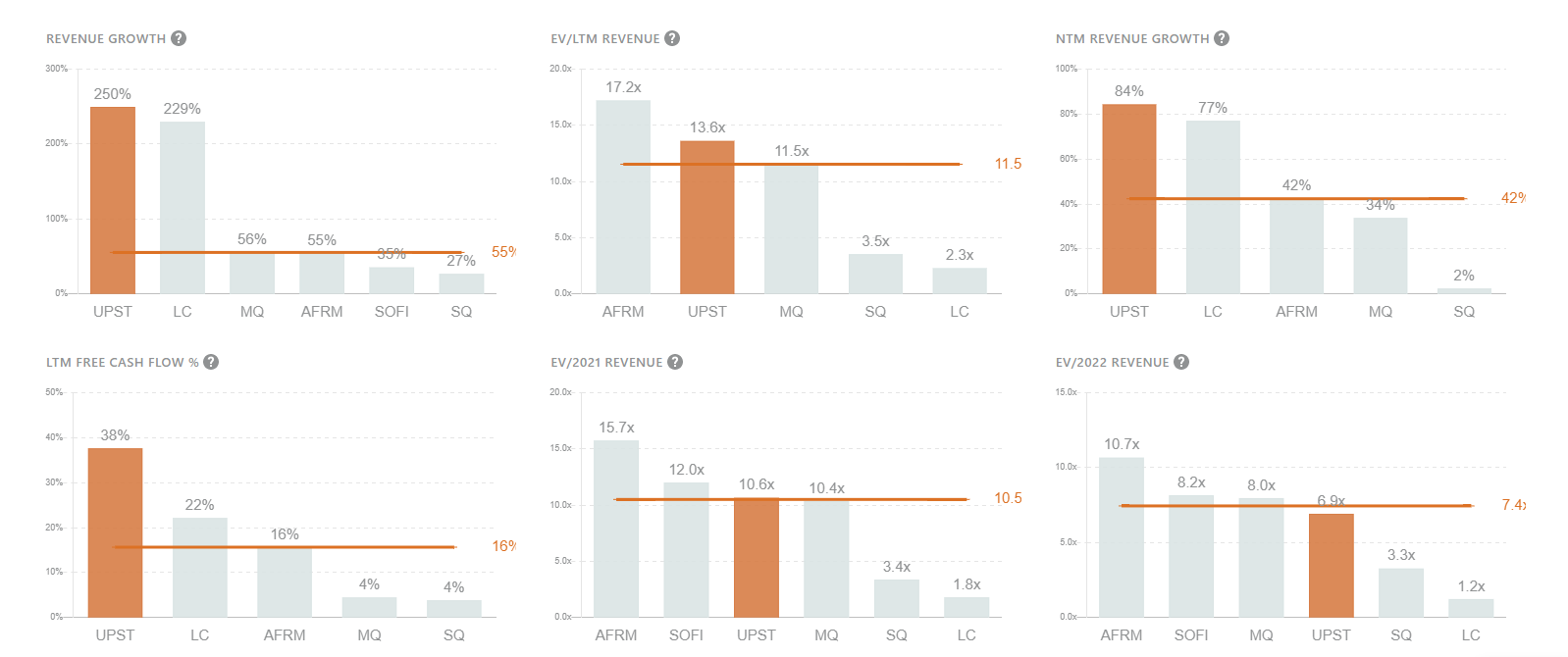

- $228M revenue (+250% YoY)

- $28.6M operating income (12.5% margin)

- $95.9M contribution profit (46% margin)

- 362,780 loans originated for $3.13B in volume (+244% YoY)

- 23% conversion on rate requests (up from 15% last year)

- $255M to $266M revenue projected by management in Q4 2021

Key Takeaways from Q3'21

1. Upstart plans to roll out similar products targeting consumers that are left out of the current financial system, namely, with a small dollar loan product. Long-term, management has disclosed plans to tackle auto retail and mortgage.

On small dollar loans:

So, loans for a few $100 for a few months are just -- it's just an area ripe with exploitation. We can do it right... And we can do it under the envelope that banks operate, meaning under the 36% rate limit and with much more affordable products that don't create debt cycles better harmful to consumers — Dave Girouard, Upstart CEO, Q3 earnings call

On long-term mortgage products:

This is what we call the missing million, and from where we stand it's crystal clear that a huge fraction of these million would-be homeowners are more than credit-worthy and deserve access to an affordable mortgage. This is an opportunity that we're excited about and we'll begin to invest in significantly throughout 2022. — Dave Girouard, Upstart CEO, Q3 earnings call

2. Relationships with bank partners are not only growing, but the partnership cycle is also shortening as onboarding processes become more efficient over time.

A year-ago, we had 10 bank and credit union partners on our platform. Today we have 31 partners and we're adding them faster than ever. We're also making progress in how rapidly we can onboard these partners. In fact, our most recent bank partner went live on the platform in less than 50 days. — Dave Girouard, Upstart CEO, Q3 earnings call

Given the consensus’s concerns around customer/counterparty concentration, it’s important to note the expansion of Upstart’s network of bank partners. The implications of this are two-fold: 1) a reduced reliance on singular banks like Cross River for revenues/origination; 2) more channels for Upstart loans to be made, and subsequently, fees to be collected.

3. A concern in the past with Upstart’s business was around organic growth i.e. consumers with thin credit files moving upstream to traditional banks as they gain economic wealth. Upstart is addressing this through additive incentives, informed by Upstart’s core AI models + training data.

Only by serving consumers across the entire credit spectrum, can we reach our full potential. Even if your credit score begins with a seven or an 8, you are more than your credit score. By working with our bank partners, we're beginning to deliver instant loan offers with no origination fees and with rates that are as attractive as any on the market. — Dave Girouard, Upstart CEO, Q3 earnings call

Although Upstart’s value proposition has always been focused on the non-prime consumer, their AI platform can also inform them of high LTV consumers (i.e. consumers with healthier “true credit”). It’s evident they’re willing to go the extra mile by incentivizing those consumers with benefits like zero origination fees to acquire them.

Conclusion

The lending non-prime market is huge, and Upstart has had an incredible run over the past year. In order to remain a leader, they'll need to continually drive a moat against emerging new entrants and execute well even during tightening credit cycles. Exciting to see how they'll transform legacy practices & democratize credit!

That's it for this week. As always, never hesitate to shoot over a message (reply to this email) for any feedback or if you’d just like to chat!

Cheers,

Jimmy Zhou (@jimmynzhou on Twitter)

Like these teardowns? These are for Publiccomps.com customers only but you can have your friends subscribe to the newsletter here where we send out investment memos, market maps and analysis on the broader SaaS market.

Views expressed in these emails are ours and ours alone and don’t represent that of our previous or current employers. Public Comps provides financial and industry information regarding public software companies as part of our weekly dashboard, our blog, and emails. Such information is for general informational purposes only and should not be construed as investment advice or other professional advice.