Public Comps Weekly Update - 2022.06.21

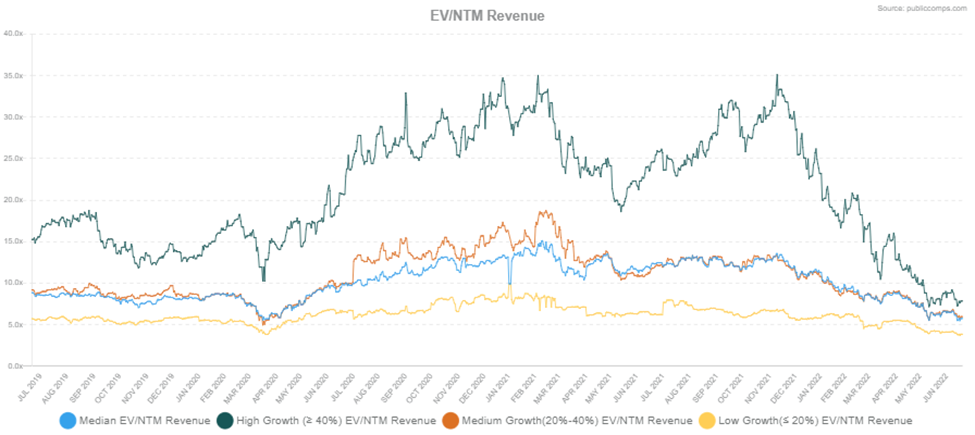

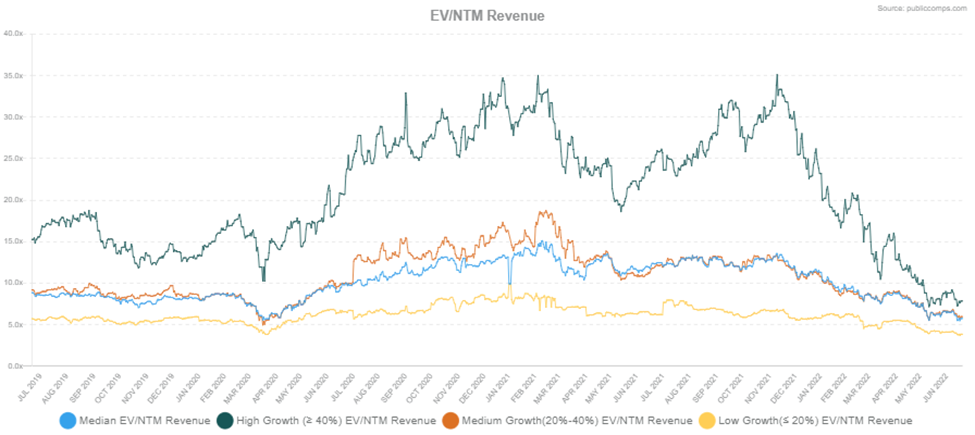

The recent drawdown has effectively taken the Median multiple back to Mar’20 / COVID trough, significantly lower than pre-COVID Dec’19 levels

Happy belated Father’s Day and Juneteenth!

Below is a quick recap of public SaaS EV/NTM multiples for the last 3 years. The recent drawdown has effectively taken the Median multiple📉📉📉 back to Mar’20 / COVID trough, significantly lower than pre-COVID Dec’19 levels. The High Growth cohort (>40% growth) has been hit disproportionally harder than Medium and Low Growth cohorts as the market shift its focus to cash flow/burn vs. growth at all cost.

As of prices as of 6/17/2022

|

|

12/31/2019 |

3/16/2020 |

6/17/2022 |

|

High Growth (>40%) |

13.2x |

10.2x |

7.8x |

|

Medium Growth (20-40%) |

8.6x |

4.9x |

6.0x |

|

Low Growth (<20%) |

6.0x |

3.9x |

3.9x |

|

Median |

8.1x |

5.5x |

5.7x |

When shown this data, it is easy to get blinded by narrative bias: THE MARKET OVERCORRECTED AND MULTIPLES SHOULD REVERT BACK TO PRE-COVID DEC’19 LEVELS. However, the macro environment and business backdrop have totally changed. Interest rates are heading significantly higher. Spending is coming down. Growth is slowing. And COVID pulled forward years of adoption and demand. A discount to pre-Dec'19 levels MAY be warranted.

In 2011, Bill Gurley wrote: “investors commonly use a handful of other shortcuts to determine valuations. ‘Price earnings ratio’ and ‘enterprise value to EBITDA’ are common shortcuts, with their own benefits and limitations…. the price/revenue multiple is the crudest valuation tool of them all.”

So maybe...the better question is whether revenue multiple is still the right metric to value SaaS businesses? But sometimes revenue is the only metric that we can slap a multiple on…😅 (no EBITDA, Net Income or FCF)

Revenue multiple will be missed. pic.twitter.com/ZFmFM0V5mV

— Value Investor (@ValueIn72055855) June 8, 2022

In all seriousness, investors are (were) willing to ascribe software businesses with a revenue multiple because:

1. Software businesses have very high margins (e.g., 70-90% gross and 30-50% EBITDA), and

2. In a downturn when growth slows, SaaS companies SHOULD be able to maintain topline (sticky contracts and mission critical with high NDR) and cut S&M to generate a steady stream FCF (i.e., a high-quality stream of annuity / perpetuity). Assuming no topline growth and 40% margin, 8x ARR will translate to 5% FCF yield

Today, software is at an exciting intersection in which the SaaS investment thesis is about to get tested in the public markets. Layoffs and hiring freezes are happening across the board. Software companies are doing zero based budgeting across the board – everything is getting scrutinized. Anecdotally, we have had a few large SaaS customers revisit and renewed their 5-figure Public Comps contract.

In the same vein that all revenue is not created equal – SaaS is not created equal. Those with high gross margin, ability to flip profitability quickly, and demonstrate growth (strong value proposition / mission-critical to their customers) should continue to warrant a healthy revenue multiple. Fundamentals matter. Value propositions matter. End markets matter. Happy hunting👋🙏!

PS: keep in mind that, eventually even the best companies (e.g., Google, Amazon and Microsoft) trade at 20x EBITDA/Net Income/ FCF (not REVENUE) at maturation.

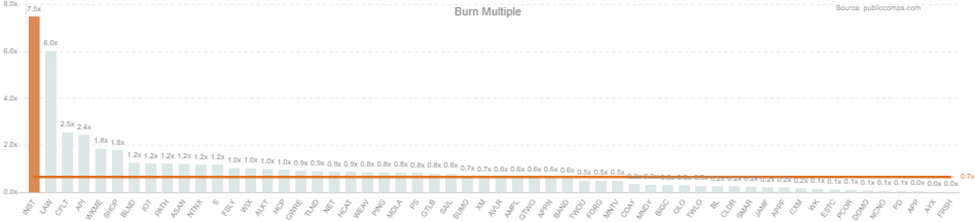

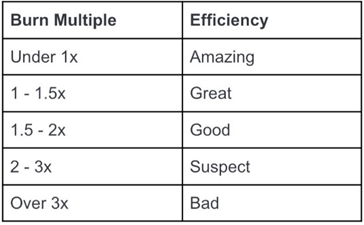

New Metrics Alert: we added Burn Multiple and LTM Burn Multiple to the Dashboard. Credit to David Sacks and Craft Ventures for this metric, and thank you subscribing to Public Comps and using us in their latest presentations

New blog post: The Burn Multiple

— David Sacks (@DavidSacks) April 23, 2020

How Startups Should Think About Capital Efficiencyhttps://t.co/JdMlHRdNyP

Burn Multiple = Net Burn / Net New ARR

- Net Burn = FCF (Cash Flow from Operations lessCapex)

- Net New ARR = Current Quarter ARR less Prior Quarter ARR

Below is David Sacks’ rule of thumb for venture-stage startups:

Public Comps in action with Craft Ventures

Tidbits that we picked up the last couple of weeks:

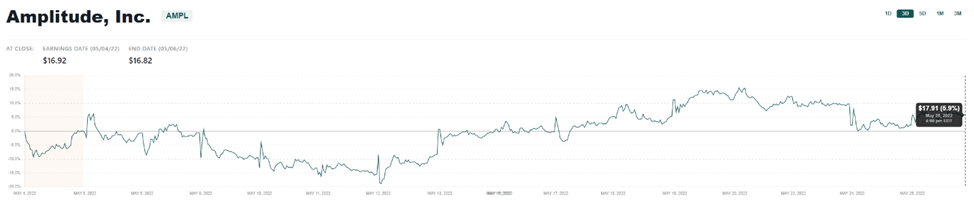

Although virtually every SaaS company we track has been substantially corrected, we share some tidbits we picked up that put color behind price action of the names we follow. We dive into the magnitude and drivers behind selloffs post-Q1 earnings for Amplitude, Unity, and Zoom.

Amplitude

Financial Overview:

- Revenue: $53.1 million (+60.4% YoY)

- Q2’22 Guidance: ~$55.0M (+39.9% YoY)

- 2022 Guidance: $232M (+38.7% YoY)

- cRPO: $149.6M (+62% YoY)

- RPO: $194.4M (+84% YoY)

- Non-GAAP Operating Loss: -$7.7 (-14.5% margin)

- Customers: 1,701 (+49% YoY)

- DBNER: 126% (Up from 118% one year ago)

By far, Amplitude’s bread and butter is still in Analytics for enterprise customers to make data-driven product decisions. It’s still the majority of revenue, despite incremental features that have been added to Experiment and Recommend. Although Amplitude’s guidance showed signs of revenue deceleration for 2022 after reporting Q1 results last month, we did not see a substantial market selloff as a result of relatively weaker guidance. It’s clear that the business is growing at a healthy rate, with total RPO growing +84% YoY and considerably strong volume-based expansion of Analytics. Management has indicated that adjacent products like Experiment and Recommend, which are frequently upsells from the core Analytics solution, are winning customers like Dropbox and IBM. They likely don’t have a meaningful contribution to revenue, but this does indicate use case for additional services in the out-of-the-box product solutions stack.

It's also interesting to note that Amplitude brought on Lambert Walsh to lead customer success at the C-suite level as software businesses can no longer rely on product-led growth as a self-sustaining channel of revenue. While the volume of inbound sales leads falter, software companies must re-allocate resources into sales motions that are sustainable without the unrelenting tailwind of pandemic-induced digital transformation. On the same note, Amplitude landed a partnership to with the AWS marketplace of software products, which will be an advantageous channel partner to have as Amplitude achieves scale and must fuel their growth beyond simple direct sales motions.

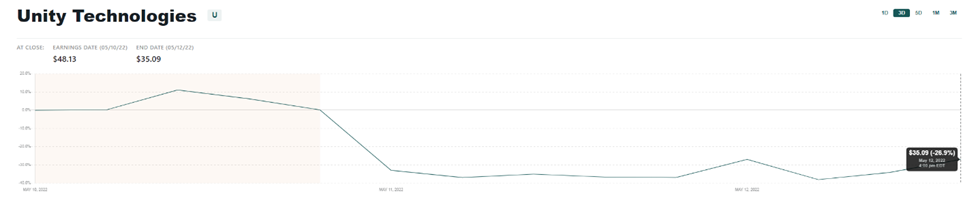

Unity

Financial Overview:

- Revenue: $320.1M (+36% YoY)

- Create Solutions revenue: $116.4M (+65% YoY)

- Operate Solutions revenue: $184.0M (+26% YoY)

- Strategic Partnerships revenue: $19.7M (+11% YoY)

- Non-GAAP operating income: -$23.0M (-7% margin)

- Free cash flow: $86.4M (27.0% margin)

- DBNER: 135% (down from 140% one year ago)

- Cash and cash equivalents: $1.2B (up from $1.1B one year ago)

Down 65% over the past year, Unity experienced a significant selloff after Q1’22 performance and macroeconomic headwinds. Operate Solutions (>50% of the Company by revenue), drastically fell short of expectations, growing +26% YoY compared to +45% YoY in the first quarter of 2021.

Although Unity’s suite of 3D content creation tools is their core business, Operate Solutions has grown to be an exceptional business and has well-positioned themselves in the advertising industry. Operate was a huge driver for the business in 2021 given high gaming engagement, and importantly, the implementation of Apple IDFA (requiring users to opt in to off-app data collection for advertisers) created a meaningful advantage because of the in-game data Unity collects. The issue this past quarter is a technical one – management attributes the downward performance due to ingesting “bad data” from a large customer and software issues in its Audience Pinpointer – contextual advertising – tool. It’s likely an issue that will adversely impact Unity for the rest of the year, but management expects no carryover impact in 2023.

Where Unity did perform was in their content engine tools – Create Solutions grew 65% YoY compared to 49% YoY growth last quarter, which we believe is a positive sign for the long-time thesis of the business. Several notable wins that led to the revenue bump include Zenith: The Last City (multiplayer VR role-playing game) across major VR devices, Syberia: The World Before (graphics adventure game), and Angry Birds’ relaunch to mobile stores using Unity’s engine. Additionally, Unity’s digital twin tech – software that helps develop virtual 3D clones of real-life objects – saw 126% YoY growth across non-gaming industries like construction, automobile simulation, and manufacturing, positioning it well for future developments in AR/VR. Finally, although the acquisition of Weta FX for $1.6B last year is still in integration, part of a $200M payment contribution to Unity’s cash flow from the deal is worth noting as Unity builds new artists solutions alongside the new team.

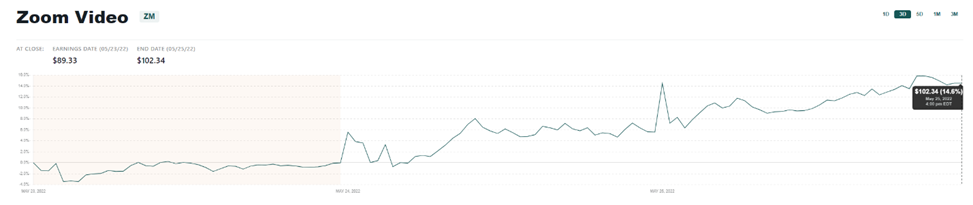

Zoom

Financial Overview:

- Revenue: $1,073.8M (+12% YoY)

- Q2 FY’23 guidance: $1.116B (+9.3% YoY)

- Full Fiscal Year 2023 guidance: $4.534B (+10.6% YoY)

- Non-GAAP operating income: $399.6 (37.2% margin)

- Operating cash flow: $526.2M (49% margin)

- # of Enterprise customers: 198,900 (+24% YoY)

- DBNER for Enterprise: 123% (down from 130% one year ago, which then included non-Enterprise customers)

Across macro headwinds and revenue deceleration in the core videoconferencing offering, Zoom has lost 70% of their price over the past year. Post Q1 FY2023 earnings, price movement has been positive, which may indicate a maturing SaaS business as revenue decelerates and Zoom becomes a cash-generative machine.

R&D and S&M spend as a percentage of revenue has come down over the past several quarters, which indicates a higher priority on profitability. The business is a cash-generative machine: Operating cash flow margin was 49% and adjusted FCF at 46%, which is an incremental $500M+ in the first quarter alone to the $5.7B cash balance they sit on. It won’t be surprising to see further acquisitions that bolster Zoom’s contact center and cloud phone businesses, which supports their play to become the end-to-end enterprise UCaaS platform.

On the enterprise front, the business is growing at a healthy level with 31% growth from Enterprise customers, which now represents >50% of the business (up from 45% in Q1’22). Management does not disclose figures about how much is specifically driven by newer products like Zoom Rooms and Zoom Phone, but we know the combination of Phone, Rooms, Contact Center make up ~10% of the core business. The cash flow generating machine is still largely driven by video, and the long-term thesis is going to depend on Zoom’s ability to expand into adjacent products.

Finally, it’s worth noting the hire of Matthew Saxon from Meta to play the role of a “Chief People Officer” to focus on employee retention. It’s clear that management is aware of the importance of talent retention as the gap between demand of labor and supply of talent widens.